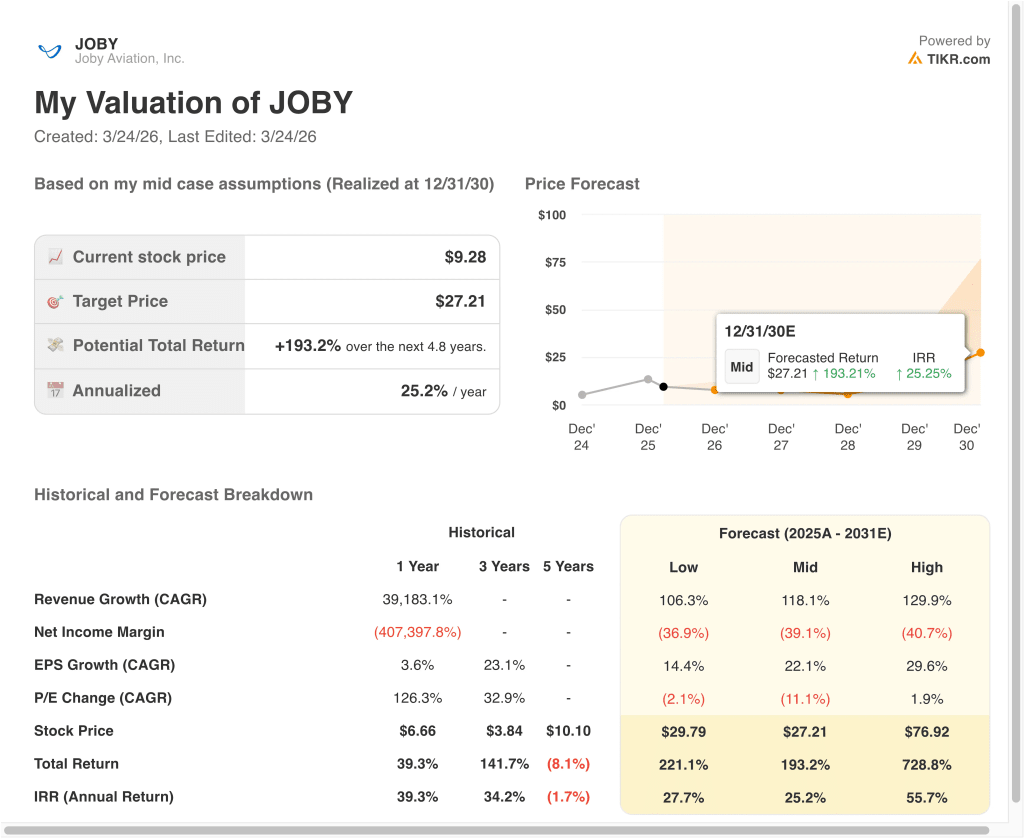

Key Stats for JOBY Stock

- Past week’s performance: -2.7%

- 52-week range: $5 to $21

- Valuation model target price: $27

- Implied upside: 193.2% over 4.8 years

Value your favorite stocks like JOBY with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Joby Aviation (JOBY) stock declined about 2.7% over the past week, even as the company continued to make operational progress toward commercializing its electric air taxi business. The move comes as investors weigh near-term risks against longer-term opportunities in the emerging eVTOL market. With the stock still well below its 52-week high of $21, sentiment remains cautious.

During the week, Joby completed piloted electric air taxi flights across the San Francisco Bay Area and advanced testing of its first FAA-conforming aircraft. These milestones are important because they move the company closer to certification and commercial launch. However, these developments did not translate into immediate stock gains.

At the same time, insider selling activity was disclosed, including share disposals by executives such as the President of Aircraft OEM and other senior leaders. While these transactions are not uncommon, they can weigh on investor sentiment, particularly for early-stage companies. As a result, the stock faced additional pressure during the week.

Investors are also closely watching the upcoming March 30 lock-up expiration, which could increase share supply in the market. This event includes common stock, options, and warrants becoming eligible for sale. The anticipation of this added liquidity may be contributing to the recent weakness in the stock.

See analysts’ growth forecasts and price targets for JOBY (It’s free) >>>

Is JOBY Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 118.1%

- Net Income Margin: -39.1%

- EPS Growth (CAGR): 22.1%

- P/E Change (CAGR): -11.1%

Based on these inputs, the model estimates a target price of $27.21, implying 193.2% total upside from the current share price and a 25.2% annualized return over the next 4.8 years.

The valuation reflects extremely high expected revenue growth as Joby transitions from development to commercialization. However, the model also assumes continued negative margins, highlighting the capital-intensive nature of scaling an air mobility platform. This balance between growth and profitability is central to the investment case.

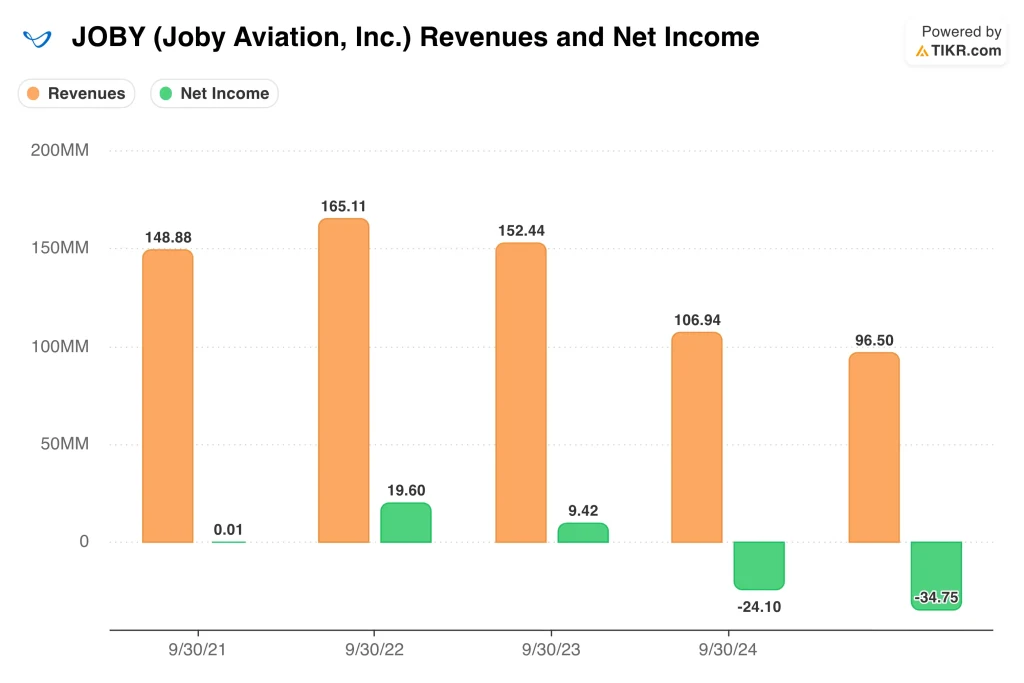

Recent financial results reinforce this dynamic, with FY 2025 revenue declining to about $96 million and net income at -34.8 million. Operating margins remain negative at around -2.9%, reflecting ongoing investment in R&D and manufacturing capabilities. These figures show that the company is still in an early stage of its lifecycle.

The projected returns depend heavily on successful execution, including regulatory approval and scaling operations. While the valuation model suggests significant upside, the market is currently pricing in execution risk. This explains why the stock remains volatile despite positive operational milestones.

What’s Driving the Stock Going Forward?

Joby’s performance will largely depend on its ability to achieve FAA certification and begin commercial operations. The company has already started testing FAA-conforming aircraft, which is a critical step toward regulatory approval. Progress here will likely be one of the biggest drivers of investor sentiment.

Partnerships and government programs are also playing a key role in shaping expectations. Joby was selected for a White House-backed air taxi program, with plans to begin U.S. operations in 2026. This provides a clearer timeline for commercialization, which could influence how investors value the business.

At the same time, capital requirements remain a major factor. The company recently raised funds through equity and convertible note offerings, highlighting the need for ongoing financing. While this supports growth, it can also lead to dilution, which investors must consider.

Finally, competitive dynamics in the eVTOL space continue to evolve, with rivals like Archer Aviation also advancing their programs. This competition adds both validation and risk to the industry. As a result, Joby’s ability to execute ahead of peers will be critical in determining its long-term valuation.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Joby Aviation, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up JOBY, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track JOBY alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Joby Aviation stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!