Key Stats for Sysco Stock

- Past-Week Performance: -4.9%

- 52-Week Range: $67.1 to $91.9

- Current Price: $81.6

What Happened?

Sysco‘s CFO departure to a larger rival coincides with the food distributor’s sharpest local case volume inflection in years, with U.S. local volume up 1.2% in Q2 FY2026 after nine consecutive international quarters of double-digit profit growth and the stock sitting at $81.60, well off its 52-week high of $91.85.

On March 5, CFO Kenny Cheung announced his departure for McKesson, triggering a same-day leadership transition that installed Brandon Sewell as Interim CFO while Sysco simultaneously reaffirmed FY2026 adjusted EPS at the high end of its $4.5 to $4.6 guidance range and expressed confidence in Q3 consensus EPS of $0.94.

Sysco’s local volume improvement, a 140-basis-point sequential acceleration in Q2 driven by the AI 360 CRM selling tool, stabilized sales consultant retention, and the late-December acquisition of Ginsberg’s Foods, a Northeast broadline distributor, outpaced an industry where Black Box restaurant foot traffic fell more than 200 basis points in the same period.

Meanwhile, Cheung has stated on the Q2 FY2026 earnings call last January that “our free cash flow was $413 million, up 25%, highlighting strong quality of earnings,” a figure that underscores the operational discipline carrying into a second half where USFS adjusted operating income is expected to return to positive growth.

Sysco’s long-term algorithm targets 9% to 11% annual total shareholder return, supported by $1 billion in planned dividends, $1 billion in buybacks resuming in Q3, a $377 billion U.S. food-away-from-home TAM where Sysco holds roughly 18% share, and an international segment that management has committed to growing to company-average profitability with no stated ceiling.

Wall Street’s Take on SYY Stock

Cheung’s departure for McKesson removes the CFO who oversaw Sysco’s local volume inflection, yet the company’s same-day guidance reaffirmation signals that operational momentum now runs deeper than any single executive.

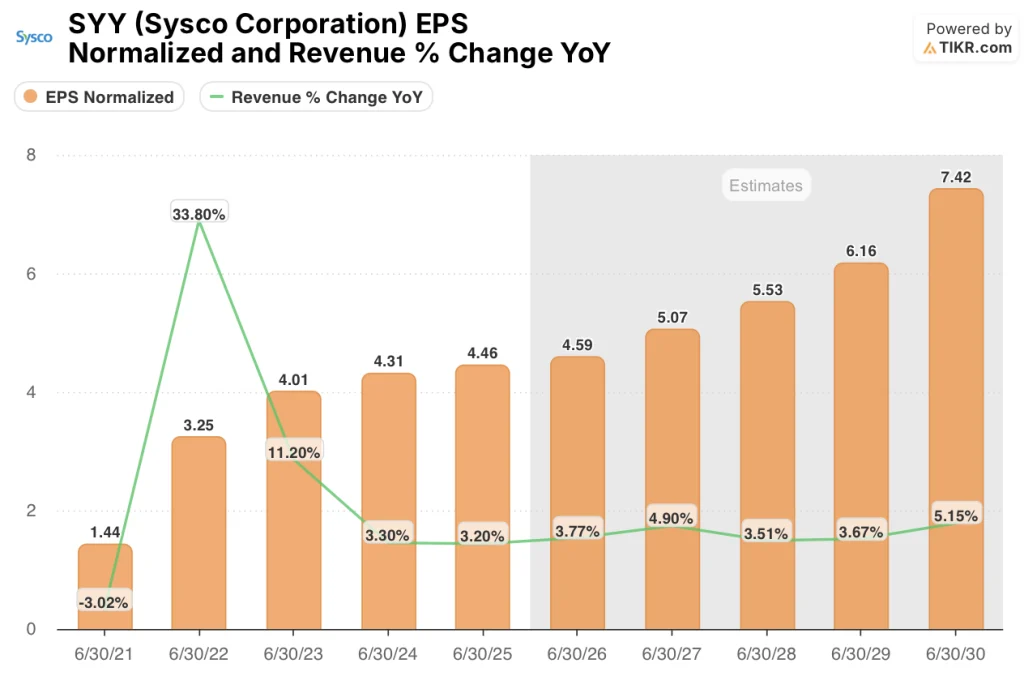

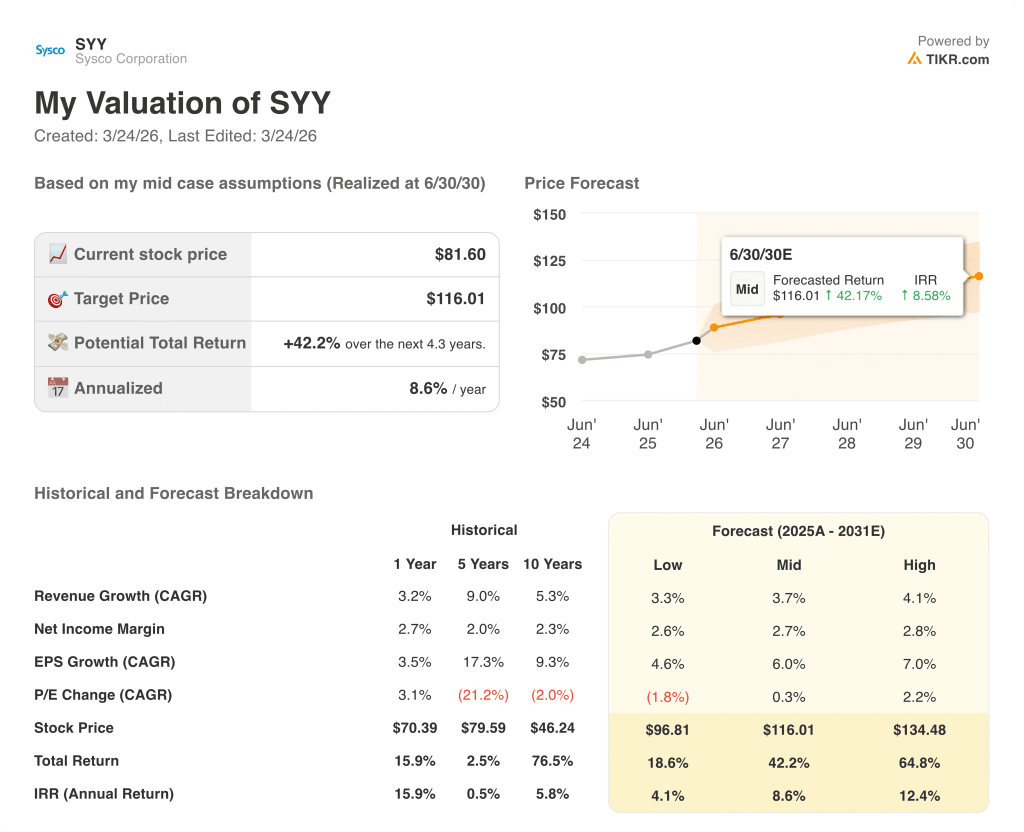

Sysco’s mid-case TIKR estimates prices shares at $116.01 by June 2030, implying a 42.2% total return at an 8.6% annual IRR, driven by a 3.7% revenue CAGR and EPS growing from $4.59 in FY2026 to $7.42 by FY2030 as local volume gains compound across a $377 billion U.S. food-away-from-home market.

The bull case’s most compelling evidence is FCF surging 52.8% from $1.6 billion in FY2025 to an estimated $2.45 billion in FY2026, validating that the AI 360-driven volume recovery and supply chain discipline are converting to real cash, not just reported earnings.

Wall Street sits constructively bullish but not euphoric: 7 buys, 2 outperforms, and 9 holds from 15 analysts produce a mean price target of $90.80, implying 11.3% upside from $81.60, a restrained consensus that likely underweights the FCF acceleration already confirmed in Q2’s year-to-date free cash flow print of $413 million, up 25%.

The spread between the $83.00 street low and the $102.00 street high reflects a genuine fork: the low anchors to execution risk on the CFO transition and a soft restaurant traffic backdrop, while the high price target requires the 2.5%-plus local volume guide to hold and the Ginsberg acquisition to contribute its projected 50 basis points per quarter in H2.

What Does the Valuation Model Say?

The market is pricing Sysco as a low-single-digit grower, but normalized EPS accelerates from 2.9% growth in FY2026 to 10.4% in FY2027 as volume leverage kicks in and the $100 million incentive compensation headwind fully rolls off.

The TIKR model’s $116.01 mid-case target rests on a 3.7% revenue CAGR, directly supported by management’s confirmed H2 FY2026 local case growth guide of at least 2.5% and a national volume recovery to greater than 2%, both of which Sysco reaffirmed on March 5.

Moreover, CEO Kevin Hourican’s statement on the Q2 call that the AI 360 tool shows higher sales among more frequent users, in a quarter where Sysco gained 140 basis points against a market that lost 200 basis points, confirms this is structural share gain, not a macro bounce.

The one development that breaks the TIKR model’s core assumption is a sustained deterioration in USFS local case growth below 2% in H2, which would collapse the volume leverage underpinning the FCF jump from $1.60 billion to $2.45 billion.

Q3 FY2026 earnings, where management has set a specific consensus EPS target of $0.94 and a local volume floor of 2.5%, will confirm whether the AI 360 productivity gains and post-CFO transition stability are tracking on schedule.

Should You Invest in Sysco?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Sysco stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SYY alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze SYY stock on TIKR for Free →