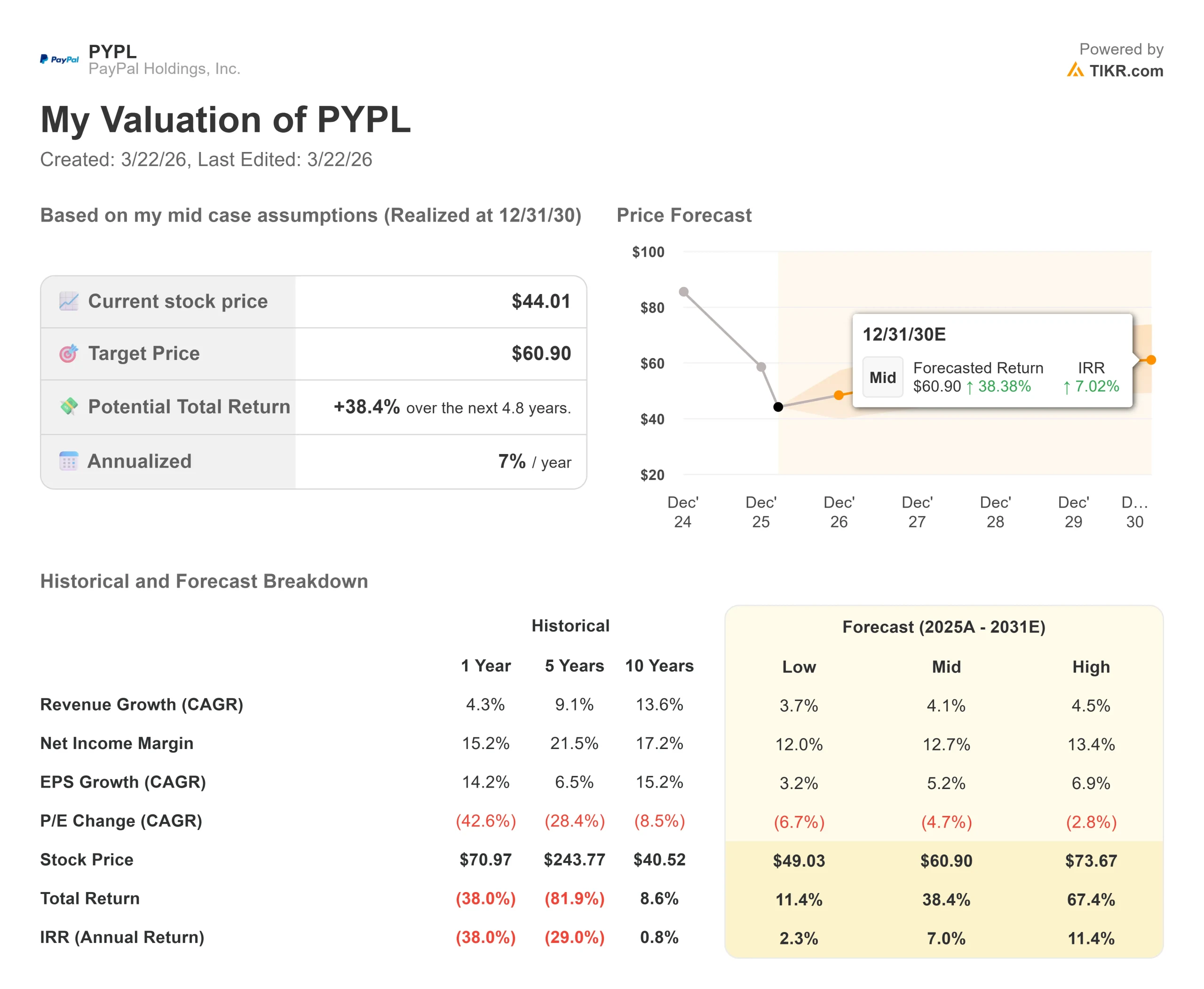

Key Stats for PayPal Stock

- Current Price: $44

- Target Price: $61

- Street Target: $50

- Potential Total Return: +38.4%

- Annualized IRR: 7%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

PayPal Holdings, Inc. (PYPL) has structurally remixed its operational expenses to arrest a deceleration in its legacy checkout business.

Speaking at the Wolfe FinTech Forum on March 10, 2026, CFO Jamie Miller confirmed that more than 60% of the company’s total OpEx is now dedicated directly to product, marketing, and tech.

This capital is funding an ecosystem overhaul required after core branded checkout volume growth slowed to just 1% in the fourth quarter.

Miller explicitly diagnosed this slowdown as the result of a “K-shaped economy,” where PayPal’s core middle-to-lower income consumer base in the U.S. and Germany is disproportionately pulling back on discretionary retail spending, compounded by tougher year-over-year comps in crypto and gaming.

To counter this, PayPal is heavily monetizing its peripheral assets and bridging them into a unified merchant architecture called “PayPal Open.”

Venmo, which now boasts over 100 million annual active accounts, is a primary growth engine.

Co-branded Venmo debit cards, launched through university partnerships, have acquired over 8 million consumers since September 2024.

According to Miller, these debit users create a measurable “halo effect,” meaning that once a consumer gets a Venmo debit card, they subsequently increase their overall online transactions with PayPal by 20% to 30%, proving that the debit card acts as a gateway to broader PayPal ecosystem usage rather than just a standalone product.

Crucially, Miller revealed that these debit transactions are just as profitable, if not more so, than the core branded checkout button, proving PayPal can diversify its revenue without diluting margins.

Simultaneously, the unbranded processing unit, Braintree, PayPal’s behind-the-scenes payment processing service, has transitioned from a loss leader to a profitable margin grower.

By renegotiating legacy contracts with large merchants and scaling its high-margin value-added services (VAS) to exactly 16 distinct offerings, Braintree is effectively competing against pure-play payment service providers (PSPs) on absolute profitability.

Under newly appointed CEO Enrique, PayPal is also leveraging its scale to act as the orchestration layer for “agentic commerce.”

By providing identity authentication and cross-border compliance, PayPal is positioning its network as the bridge between global merchants and large language models (LLMs) operated by Microsoft, Google, Perplexity, and OpenAI.

“When you look at 2026, I’d say the biggest thing is focus and execution,” Miller noted regarding the new CEO’s mandate.

“We have a lot of innovation in flight. What we’ve got to do is really capture that, bring it down, prioritize it and really execute it.”

See historical and forward estimates for PayPal stock (It’s free!) >>>

Is PayPal Undervalued Today?

Trading at $44.01, PayPal’s equity reflects a severe 50.04% max drawdown logged in mid-February 2026.

The market reacted negatively to the company’s fourth-quarter report, issuing a -1.61% earnings reaction on February 3, 2026.

The primary bear case rests on a structural headwind to transaction margins.

After enjoying 6% transaction margin dollar growth in 2025, Miller explicitly guided that 2026 growth will be slightly negative to flat (excluding interest on customer balances).

This compression stems from lower anticipated credit contributions, declining interest rates (stripping 1 to 2 points of growth), and a planned $400 million operational investment.

Management is dedicating two-thirds of this $400 million specifically to defend the branded checkout experience, with the remaining one-third funding agentic commerce and Venmo loyalty programs.

However, institutional holders like The Vanguard Group and BlackRock are anchoring their positions on the company’s capital return floor.

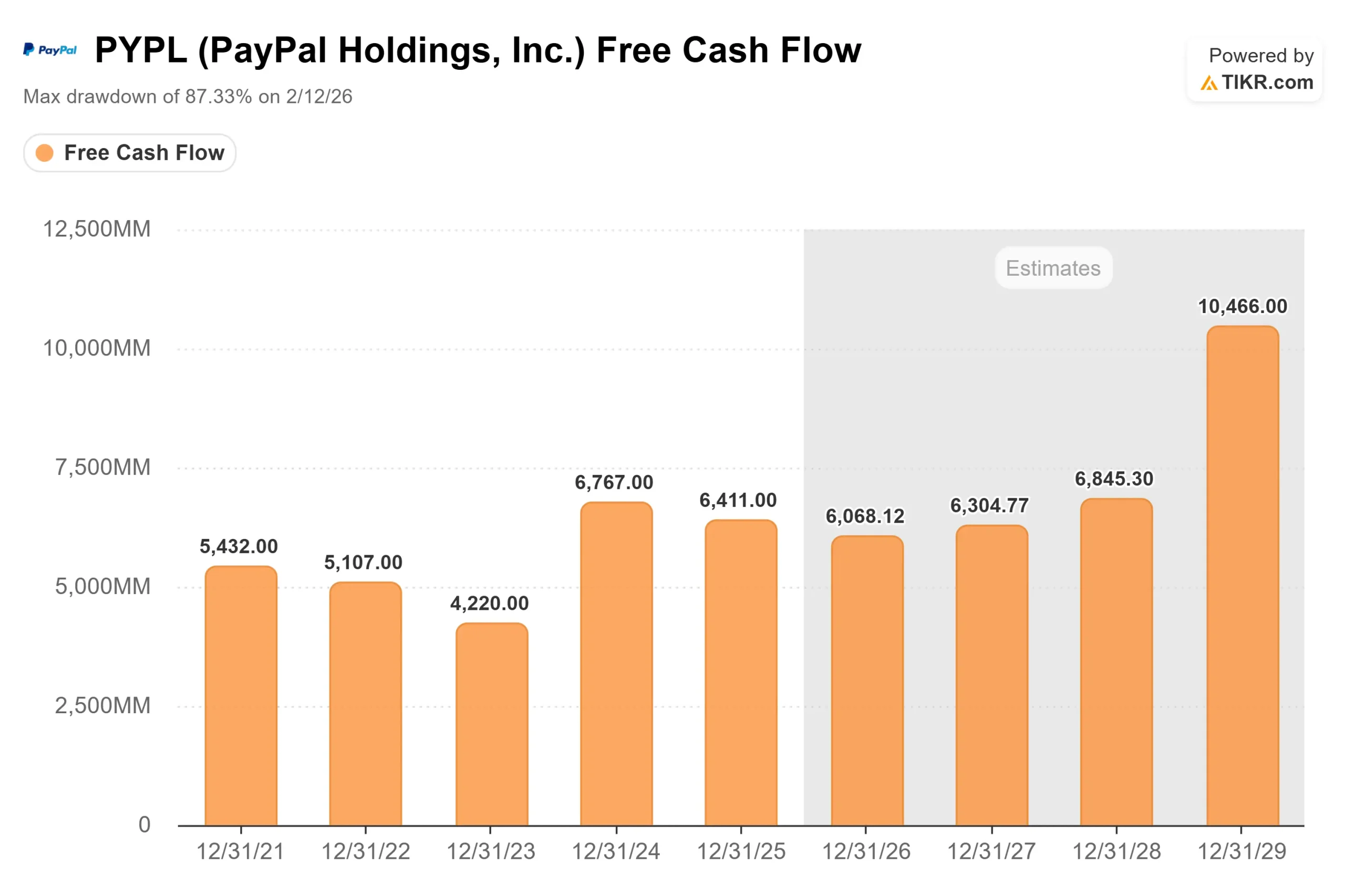

PayPal maintains a $15 billion cash pile and management targets approximately $6 billion in annual free cash flow.

Management is utilizing 100% of this free cash flow to fund a $6 billion share repurchase program in 2026, supplemented by a newly initiated quarterly dividend program targeting a 10% payout ratio of non-GAAP net earnings.

TIKR Advanced Model Analysis

The TIKR Advanced Model calculates the financial output of PayPal absorbing its $400 million margin drag while executing aggressive share repurchases.

- Current Price: $44

- Target Price: $61

- Potential Total Return: +38.4%

- Annualized IRR: 7%

Build a 4-year Valuation Model for PYPL for yourself (It’s free) >>>

Unlike the skeptical Street consensus, the Mid Case model projects a $60.90 target price. This target assumes that the upstream investments in Buy Now, Pay Later (which generated $40 billion in volume last year) and the restructuring of Braintree’s contracts successfully stabilize the core ecosystem.

The mathematical constraint on the valuation is the structural reset of the company’s operating margins. Because Braintree naturally operates at lower absolute margins than the legacy branded checkout button, and the company must continually co-invest with mega-merchants to retain processing share, overall profitability remains constrained relative to historical peaks. However, by factoring in the aggressive $6 billion share reduction against a resilient $6 billion free cash flow baseline, the model yields a 7.0% annualized IRR. This indicates the stock is currently fairly valued, possessing a highly secure fundamental floor.

Conclusion: PayPal is actively sacrificing 2026 margin growth to fund a $400 million revitalization of its branded checkout architecture and AI orchestration layers. While Wall Street’s $50.35 target reflects valid concerns regarding the 1% growth rate in the core business amidst a K-shaped economy, the company’s 100% free cash flow allocation toward buybacks provides a strict valuation floor. Watch the Q2 2026 earnings release for specific data on branded checkout TPV; if the newly launched loyalty programs and 60% OpEx reallocation fail to accelerate volume growth past 2%, it will indicate that the core franchise remains structurally impaired, requiring a downward revision to the $60 target.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in PayPal?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PayPal, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PayPal alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!