Key Stats for Marriott Stock

- Past-Week Performance: +1.9%

- 52-Week Range: $205.4 to $370

- Current Price: $326.5

What Happened?

Marriott International‘s loyalty program, Bonvoy, which drives direct bookings and reduces reliance on third-party booking platforms, crossed 271 million members in 2025 while co-branded credit card fees surged to $716 million, turning the program itself into a standalone revenue engine that now anchors management’s 13% to 15% EPS growth target for 2026, with the stock at $326.52.

Last February 10, CFO Kathleen Oberg detailed a 35% projected jump in co-branded credit card royalty fees for 2026, driven by a renegotiated contractual limitation on Marriott’s royalty rate and nearly $100 million in above-property cost savings, with full-year gross fee revenues guided to $5.9 billion to $5.96 billion.

Underpinning that fee acceleration, Marriott closed 2025 with a record pipeline of 610,000 rooms, up 6% year-over-year, and guided net unit growth to 4.5% to 5% for 2026, a pace that trails Hilton’s mid-single-digit target only marginally while Marriott carries a meaningfully larger absolute base of nearly 1.78 million rooms.

CEO Anthony Capuano stated at the J.P. Morgan Gaming, Lodging, Restaurant and Leisure Management Access Forum on March 12 that “internationally, there is an almost insatiable demand for luxury,” tying directly to Marriott’s record 114 luxury deals signed in 2025 and its plan to convert Pelican Hill Resort in Newport Coast into the first St. Regis Estate.

Marriott’s confirmed plan to return over $4.3 billion to shareholders in 2026, the mid-2026 rollout of natural language AI search on marriott.com and the Bonvoy app, and the 35-basis-point World Cup RevPAR tailwind collectively position the company to compound fee revenue well beyond the current $5.4 billion base as its 600,000-room pipeline converts to income-generating properties over the next three to five years.

Wall Street’s Take on MAR Stock

The 35% projected jump in co-branded credit card royalty fees for 2026, structurally locked in through a renegotiated contractual rate on Bonvoy’s loyalty program, converts an already-growing revenue line into a high-margin fee accelerant that flows almost directly to the bottom line, pushing management’s 2026 adjusted diluted EPS guidance to growth of 13% to 15%.

That EPS step-change is grounded in two converging forces: gross fee revenues guided to $5.9 billion to $5.96 billion in 2026, up 8% to 10%, while the TIKR model projects EBITDA margins expanding from 20.6% in 2025 to 21.1% in 2026 and 22.1% by 2028, reflecting the asset-light model’s operating leverage as 610,000 pipeline rooms convert to fee-generating properties.

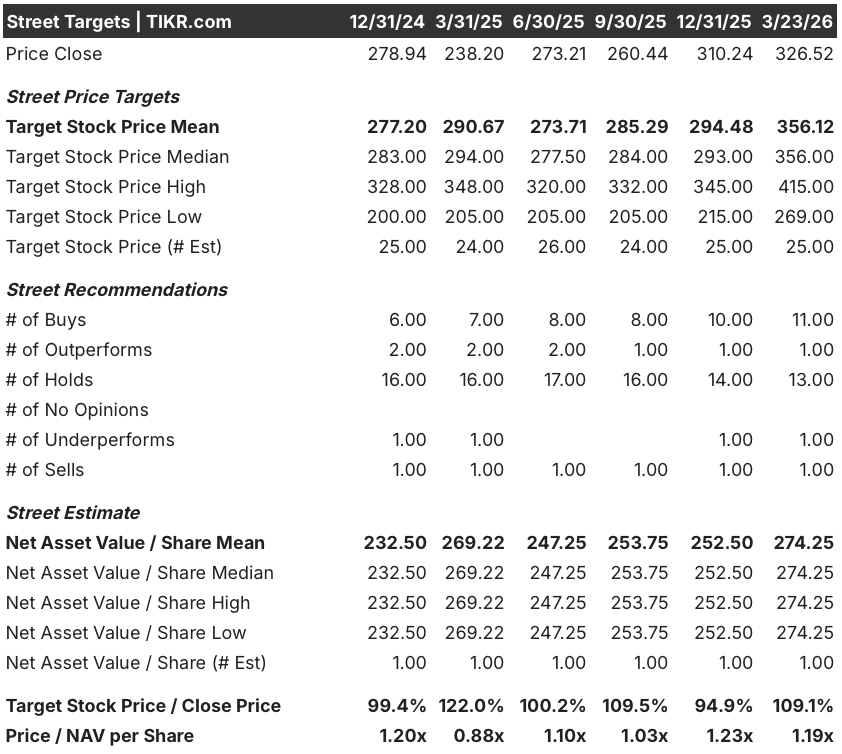

Wall Street’s distribution tells a story of cautious optimism held back by macro hesitation: 11 buys, 1 outperform, 13 holds, 1 underperform, and 1 sell among 25 analysts produce a mean price target of $356.12, implying 9.1% upside from $326.52, with the consensus anchored on steady RevPAR growth of 1.5% to 2.5% and the World Cup adding approximately 35 basis points to global RevPAR in 2026.

The spread between the analyst low of $269 and the high of $415 maps almost precisely to two scenarios already introduced: the low reflects a scenario where the U.S.-Iran conflict expands and suppresses inbound international travel, eroding the World Cup demand thesis, while the high reflects full credit card renegotiation upside with Chase and American Express closing later in 2026 on top of the royalty rate increase.

What Does the Valuation Model Say?

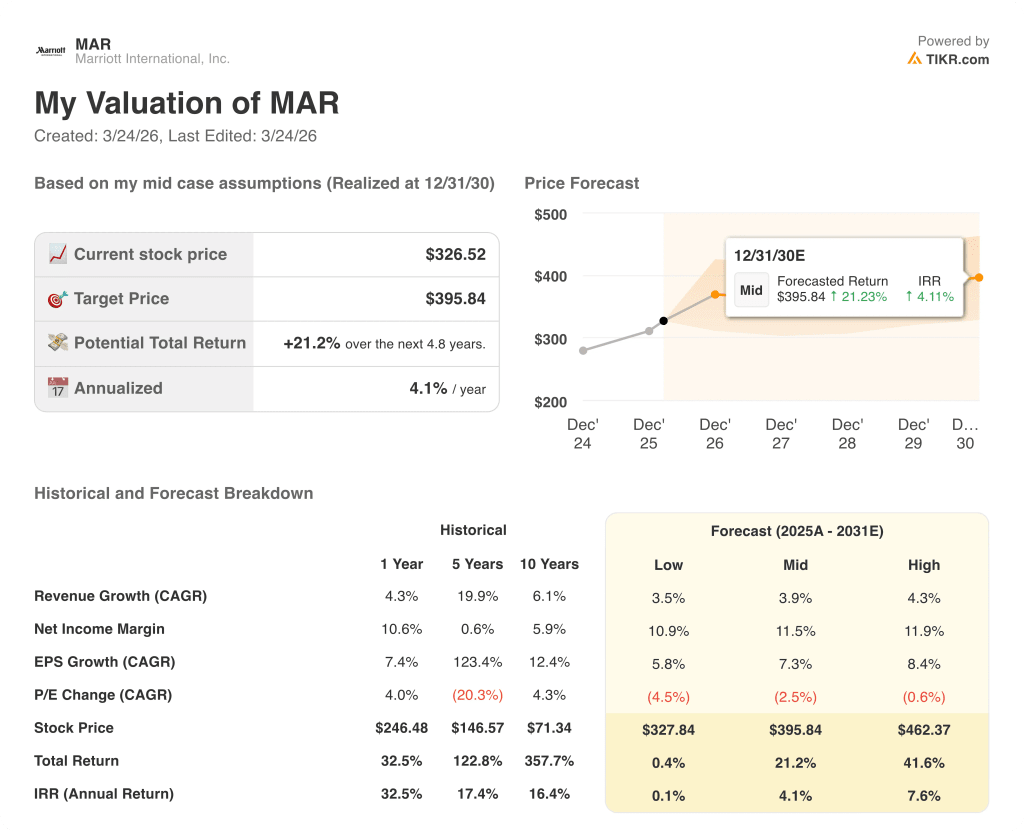

The TIKR mid-case target of $395.84, implying a 21.2% total return over 4.8 years at a 4.1% IRR, is built on a revenue CAGR of 3.9% through 2030 and a net income margin expanding from 10.5% in 2025 to 11.5% in the mid case, driven by the royalty renegotiation and the scale efficiencies Marriott has already demonstrated through nearly $100 million in above-property cost reductions.

The market is pricing MAR as a steady compounder at 9.1% upside to consensus, but the royalty step-change alone drove a 35% fee line increase that is structural, not cyclical, and flows into a business with a 4.5% to 5% net unit growth guide accelerating from 2025.

Marriott’s record 610,000-room pipeline, 75% of conversions opening within 12 months of signing, and $4.3 billion in planned 2026 capital returns directly support the TIKR mid-case target of $395.84 and the EPS trajectory to $16.84 by 2029 in the normalized estimate.

CEO Anthony Capuano’s active collaboration with Google AI Mode Travel and OpenAI’s AdPilot program signals that Marriott is shaping the next distribution paradigm rather than reacting to it, a strategic optionality the model does not price.

The primary risk is a sustained broadening of the Middle East conflict, which currently accounts for 4% of global rooms and 4% of global fees but could compress international RevPAR meaningfully if airline capacity disruptions extend beyond the region, directly undermining the 1.5% to 2.5% global RevPAR growth assumption the TIKR model depends on.

The closing of new U.S. co-brand credit card deals with Chase and American Express, expected later in 2026, is the single event that confirms whether the royalty rate increase is a floor or a launchpad: watch for any guidance revision to the 35% credit card fee growth figure in the Q1 2026 earnings call.

Should You Invest in Marriott International, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MAR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marriott International, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MAR stock on TIKR for Free →