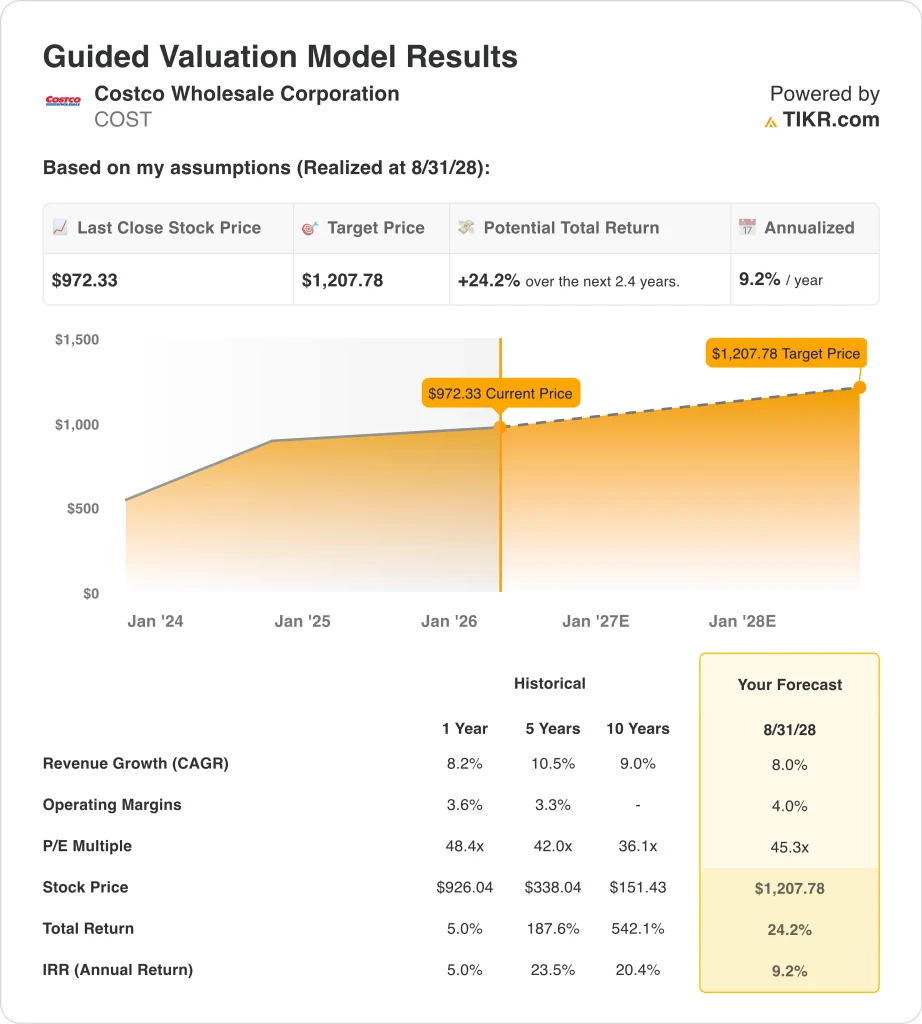

Key Stats for COST Stock

- Past week’s performance: -2.9%

- 52-week range: $844 to $1,067

- Valuation model target price: $1208

- Implied upside: 24.2% over 2.4 years

Value your favorite stocks like COST with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Costco Wholesale Corporation (COST) stock has been relatively stable, but it has pulled back slightly in recent days as investors reassess valuation. Shares were around $965 on March 23, and -2.9% move over the past week. That kind of movement is relatively small, but it comes after a strong multi-year run where the stock approached its 52-week high of $1,067.

The recent price action reflects more of a pause than a shift in the business. Costco continues to benefit from steady demand in consumer staples and strong membership renewal rates. However, the stock’s premium valuation means even small changes in sentiment or expectations can lead to short-term volatility.

There has not been a single major negative headline driving the move lower. Instead, broader retail sentiment and valuation sensitivity appear to be influencing trading. Investors are likely rotating across consumer names while waiting for clearer signals from upcoming earnings and macro trends.

Costco’s defensive positioning also plays a role here. The company tends to perform well in uncertain environments because of its value-focused offering, but that stability can limit near-term upside when investors are looking for faster growth elsewhere. So the recent pullback reflects positioning and expectations rather than a change in fundamentals.

See analysts’ growth forecasts and price targets for COST (It’s free) >>>

Is COST Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 8%

- Operating Margins: 4%

- Exit P/E Multiple: 45.3x

Based on these inputs, the model estimates a target price of $1,207.78, implying a 24.2% total return from the current share price of $972.33 and a 9.2% annualized return over the next 2.4 years.

Costco’s valuation is supported by consistency rather than rapid growth. The company has delivered revenue growth in the high-single-digit range over time, and a forward 2-year revenue CAGR of around 8.0%. That steady growth profile is one of the key reasons investors continue to assign a premium multiple to the stock.

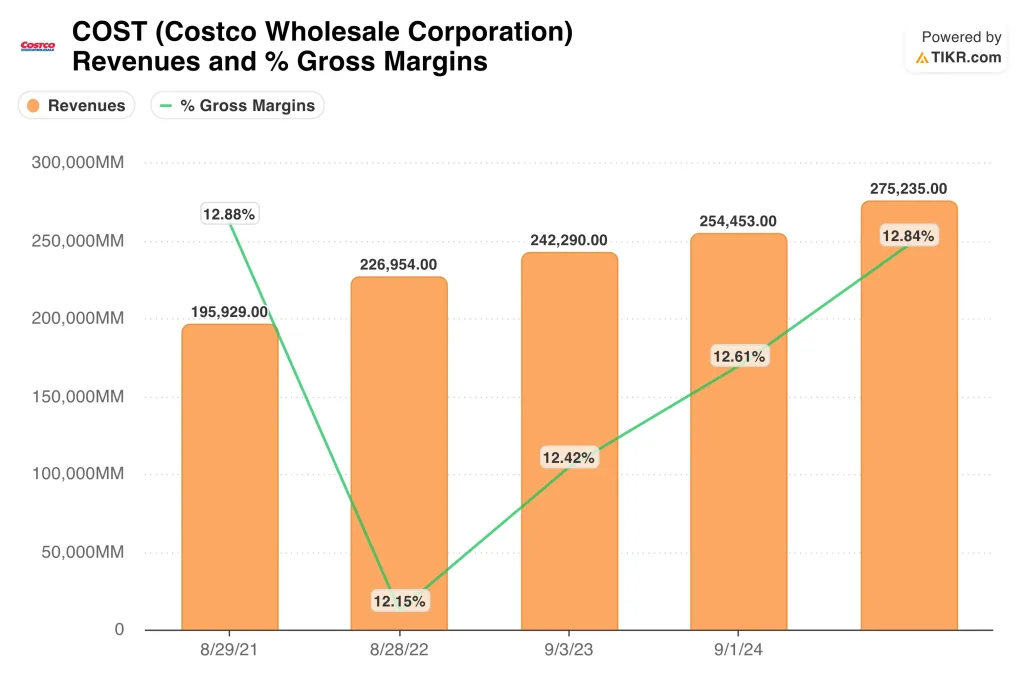

Margins are also relatively stable but structurally lower than those of many other businesses. LTM EBIT margin is 3.8%, and gross margin is 12.9%, reflecting Costco’s strategy of offering low prices and generating profit through high volume and membership fees. This model limits margin expansion but supports durable demand.

Return metrics help explain investor confidence. Costco’s LTM ROE is 29.7%, and ROIC is 27.1%, which are strong for a retail business. These figures show that even with lower margins, the company generates high returns on capital due to efficient operations and strong inventory turnover.

Balance sheet strength is another factor. Costco has a negative net debt of -9,905, which provides flexibility for dividends and reinvestment. That financial position supports the company’s resilience and helps justify its valuation relative to peers.

What’s Driving the Stock Going Forward?

The next move in Costco stock will likely depend on earnings consistency and membership trends. The company’s business model is heavily tied to recurring membership fees, which provide stable, high-margin income. Investors will continue to watch renewal rates and membership growth as key indicators of long-term performance.

Comparable sales growth will also be important. Costco’s ability to drive traffic and maintain pricing discipline in a competitive retail environment supports its revenue growth assumptions. Any signs of slowing traffic or weaker spending could impact sentiment, even if margins remain stable.

Margins will remain a key focus, even though Costco is not designed to maximize them. Investors understand that the company operates with lower margins by design, but they still watch for cost pressures, wage increases, and supply chain dynamics. Maintaining margin stability is critical to sustaining earnings growth.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Costco Wholesale Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track COST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Costco stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!