Key Takeaways:

- Rapid Expansion: Dutch Bros opened 154 new shops in 2025, growing revenues 28% to $1.64 billion.

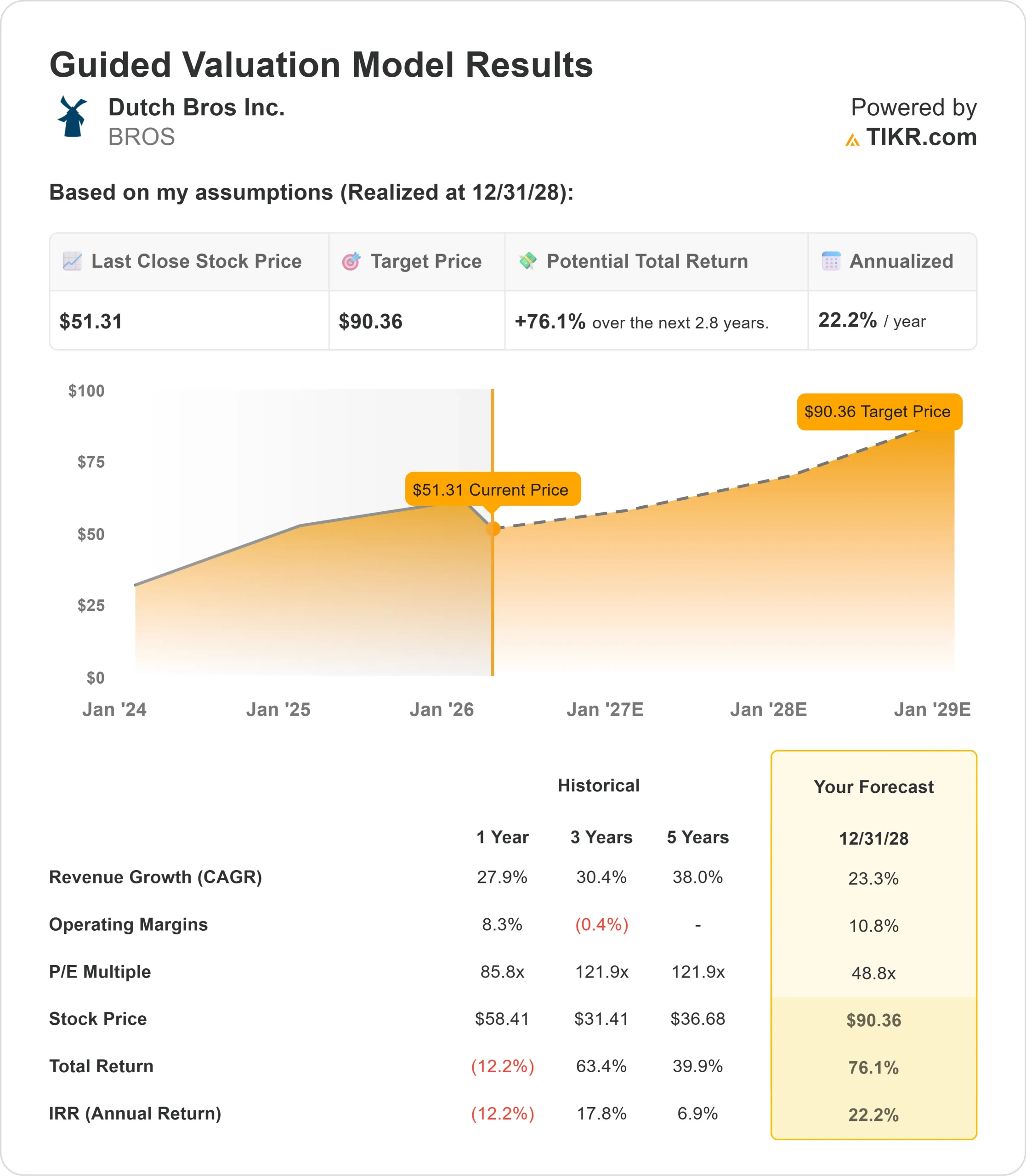

- Price Projection: Based on current execution, BROS stock could reach $90 by December 2028.

- Potential Gains: This target implies a total return of 76% from the current price of $51.

- Annual Return: Investors could see roughly 22% growth over the next 2.8 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Dutch Bros (BROS) delivered exceptional Q4 2025 results with system-wide same-store sales growth of 7.7% and company-operated same-store sales surging 9.7%, both driven primarily by robust transaction growth.

CEO Christine Barone emphasized the company’s momentum toward reaching 2,029 shops by 2029.

- The company’s Order Ahead program reached 14% of transactions in Q4, while the Dutch Rewards loyalty program now boasts over 15 million members representing 72% of system transactions.

- Standout transaction growth of 5.4% in the Q4 demonstrated the strength of Dutch Bros’ customer engagement initiatives.

- The company opened 55 new shops in Q4 alone, bringing the total system to 1,136 locations across 25 states.

- With record average unit volumes of $2.1 million and company-operated contribution margins at 28.9%,

Dutch Bros has built a highly scalable model.

Despite elevated coffee costs creating near-term headwinds, the company maintains strong shop-level economics that support aggressive expansion.

See analysts’ full growth forecasts and estimates for BROS stock (It’s free) >>>

What the Model Says for Dutch Bros Stock

We analyzed Dutch Bros as it transformed into a national drive-thru coffee powerhouse, with significant white space for growth.

The company benefits from multiple structural advantages.

- Its regional operator model creates a deep bench of talent ready to scale operations.

- Dutch Bros ended 2025 with approximately 475 regional operator candidates in the pipeline, nearly double the figure from the end of 2022.

- The new food program provides additional upside.

- After starting with just four shops in Phoenix a year ago, the program expanded to over 300 locations across 11 states.

- Management expects the food rollout to deliver approximately 4% comp lift in shops with the program, driven by both transaction and ticket growth.

Using a forecast of 23.3% annual revenue growth and 10.8% operating margins, our model projects the stock will rise to $90 within 2.8 years. This assumes a 48.8x price-to-earnings multiple.

That represents meaningful compression from Dutch Bros’ historical P/E averages of 85.8x (one year) and 121.9x (three years).

The lower multiple acknowledges near-term margin pressure from elevated coffee costs and the transition to more build-to-suit leases, which increase occupancy expenses but improve capital efficiency.

The real value lies in capturing sustained growth through shop expansion, increased customer frequency via loyalty and Order Ahead, and the maturation of the food platform.

The company’s ability to maintain transaction growth against a much larger base demonstrates the power of its brand and operational execution.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for BROS stock:

1. Revenue Growth: 23.3%

Dutch Bros’ growth centers on aggressive unit expansion and strong same-store sales.

The company opened 154 net new shops in 2025 and expects at least 181 in 2026, including 20 Clutch Coffee Bar conversions in the Carolinas. This represents 16% unit growth.

Management guides to 3-5% system same-store sales growth for 2026.

This reflects tough comparisons against 2025’s accelerating transaction growth, but still demonstrates healthy underlying momentum.

The company’s expansion into seven new contiguous states in 2025 shows its ability to successfully enter and densify markets.

New shop productivity remains elevated above the $1.8 million underwriting target, reflecting improved real estate selection and targeted marketing investments.

The walk-up format test in downtown Los Angeles, which quickly became the top-performing shop, opens potential for urban expansion beyond the traditional drive-thru model.

2. Operating margins: 10.8%

Dutch Bros has expanded adjusted EBITDA margins while scaling rapidly.

Full year 2025 adjusted EBITDA grew 31%, outpacing revenue growth of 28%.

This demonstrates the operating leverage inherent in the model.

For 2026, management expects approximately 60 basis points of EBITDA margin pressure, primarily from elevated coffee costs (about 200 basis points of pressure in Q1, moderating through the year) and increased occupancy from the shift to build-to-suit leases.

However, the company expects to offset some pressure through 70 basis points of SG&A leverage.

As coffee costs normalize and the food program scales, margins should expand toward the company’s long-term contribution margin target of approximately 30%.

3. Exit P/E Multiple: 48.8x

The market values Dutch Bros at premium multiples reflecting its growth profile. We assume compression to 48.8x as the company matures and faces tougher comparisons.

Near-term uncertainty from commodity costs and competitive product launches from larger chains weigh on the multiple.

However, Dutch Bros’ differentiated service model, emotional brand connection, and superior customization capabilities provide significant competitive advantages.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

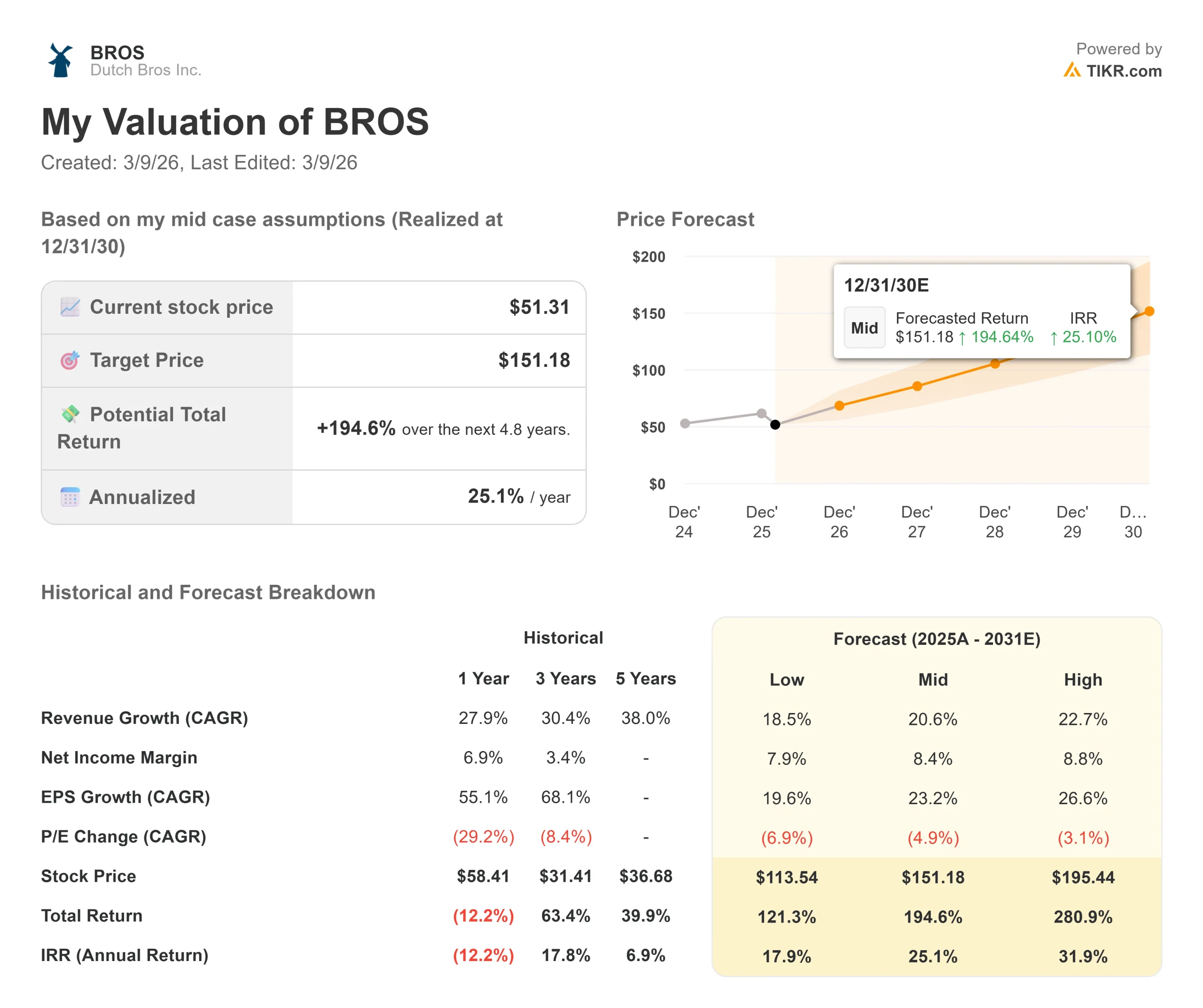

Fast-casual concepts face competition and execution risks. Here’s how Dutch Bros stock might perform under different scenarios through December 2030:

- Low Case: If revenue growth moderates to 18.5% and net income margins stay at 7.9%, investors still see a 121% total return (17.9% annually).

- Mid Case: With 20.6% growth and 8.4% margins, we expect a total return of 195% (25.1% annually).

- High Case: If unit expansion accelerates and Dutch Bros achieves 22.7% revenue growth with 8.8% margins, returns could hit 281% total (31.9% annually).

See what analysts think about BROS stock right now (Free with TIKR) >>>

The range reflects execution on the 2,029-shop goal, successful scaling of the food program, effective competition against new coffee and energy drink launches from major chains, and the company’s ability to navigate commodity cost volatility while maintaining customer frequency and ticket growth.

How Much Upside Does Dutch Bros Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!