Key Stats for Amazon Stock

- Past-Week Performance: +1.5%

- 52-Week Range: $161.9 to $258.6

- Current Price: $213.2

What Happened?

AWS, Amazon‘s cloud computing division that generates 35% operating margins and powers the company’s profit engine, accelerated to 24% growth in Q4, its fastest pace in 13 quarters, on a $142 billion annualized revenue base.

On February 5, Amazon reported Q4 net sales of $213.4 billion, up 14%, with AWS adding $2.6 billion in quarter-over-quarter revenue while its custom AI chip business, Trainium and Graviton combined, crossed a $10 billion annualized run rate growing triple digits.

The $244 billion AWS backlog, up 40% year-over-year, makes the demand picture undeniable, while Bedrock, Amazon’s platform letting companies run AI models from Anthropic, OpenAI, and others, saw customer spend grow 60% quarter-over-quarter.

Andy Jassy, CEO, stated on the Q4 2025 earnings call that “as fast as we install this capacity, this AI capacity, we are monetizing it,” directly referencing Amazon’s plan to deploy $200 billion in capital expenditures across 2026, predominantly into AWS.

With Trainium3 supply nearly fully committed by mid-2026, Trainium4 arriving in 2027, Amazon Leo satellite internet launching commercially in 2026, and AWS operating cash flow hitting $139.5 billion in 2025, the compounding infrastructure advantage widens every quarter at $213 per share.

Wall Street’s Take on AMZN Stock

AWS accelerating to 24% growth on a $142 billion base while EBITDA margins expand from 23.7% in 2025 toward a projected 26.1% in 2026 makes the forward earnings inflection feel structural, not cyclical.

Revenue is forecast to grow from $717 billion in 2025 to $807 billion in 2026 and $899 billion in 2027, while normalized EPS climbs from $7.17 to $7.72 and then $9.34 as AWS operating leverage compounds.

Wall Street is overwhelmingly bullish, with 48 buys, 15 outperforms, and just 4 holds among 62 analysts, driving a mean price target of $280.47 that implies 31.5% upside from the current $213.21 close.

The spread between the $175 low target and $360 high target reflects a genuine fork: the low anchors on $200 billion capex destroying near-term free cash flow, while the high prices in full AWS AI monetization and the Trainium chip cycle already underway.

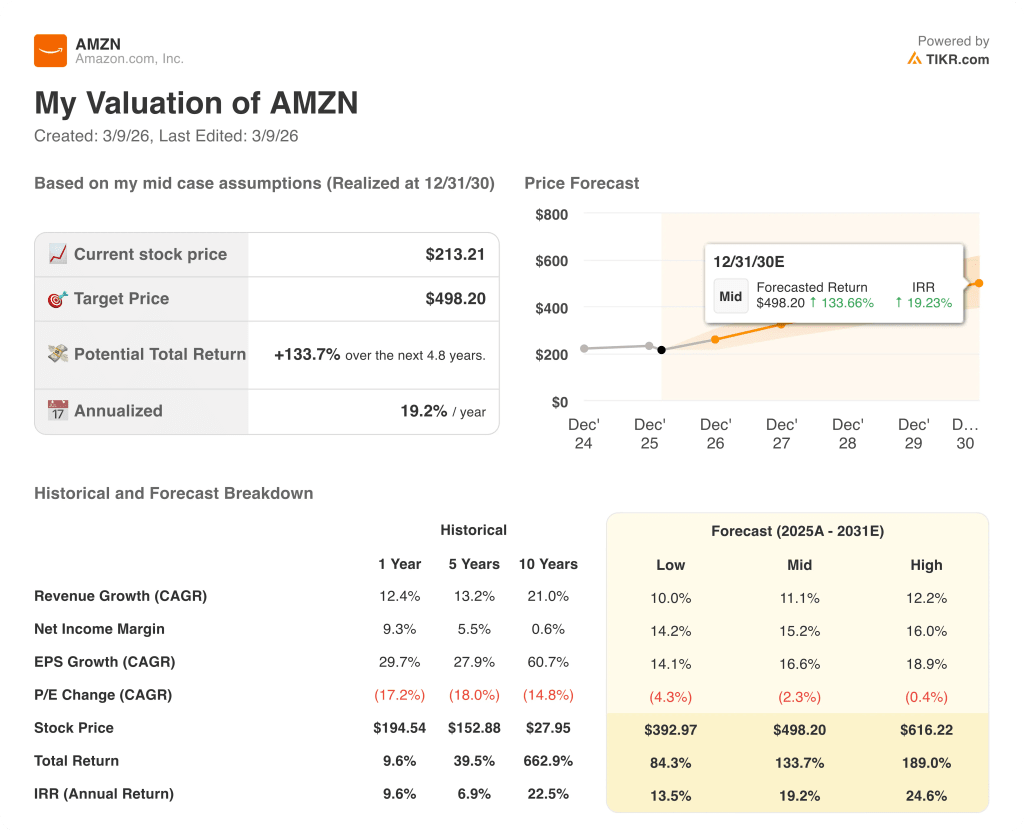

What Does the Valuation Model Say?

TIKR’s mid-case model prices AMZN at $498.20 by December 2030, a 133.7% total return at a 19.2% annualized IRR, anchored to 11.1% revenue CAGR and net income margins expanding from 10.8% today toward 15.2%.

The market is treating Amazon’s $200 billion capex commitment as a liability, yet the $244 billion AWS backlog, up 40% year-over-year, confirms demand already exceeds the capacity being built.

AWS backlog growing 40% and Trainium3 supply nearly fully committed by mid-2026 confirms the TIKR model’s margin expansion assumption as AI inference monetization scales.

Jassy stated on the February 5 earnings call that “as fast as we install this capacity, we are monetizing it,” a signal that the traditional capex-to-revenue lag is compressing for AWS in ways the market has not yet priced.

The primary risk is free cash flow: the $200 billion 2026 capex plan already compressed trailing free cash flow to $11.2 billion from $38.2 billion in 2024, and any demand shortfall breaks the margin expansion timeline entirely.

Q1 2026 operating income guidance of $16.5 billion to $21.5 billion is the first checkpoint; watch whether AWS revenue holds above $37 billion, confirming the 24% growth rate did not peak in Q4.

Should You Invest in Amazon, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMZN stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMZN stock on TIKR for Free →