Key Takeaways:

- Oracle stock could reasonably reach $312 per share by May 2028, based on our valuation assumptions.

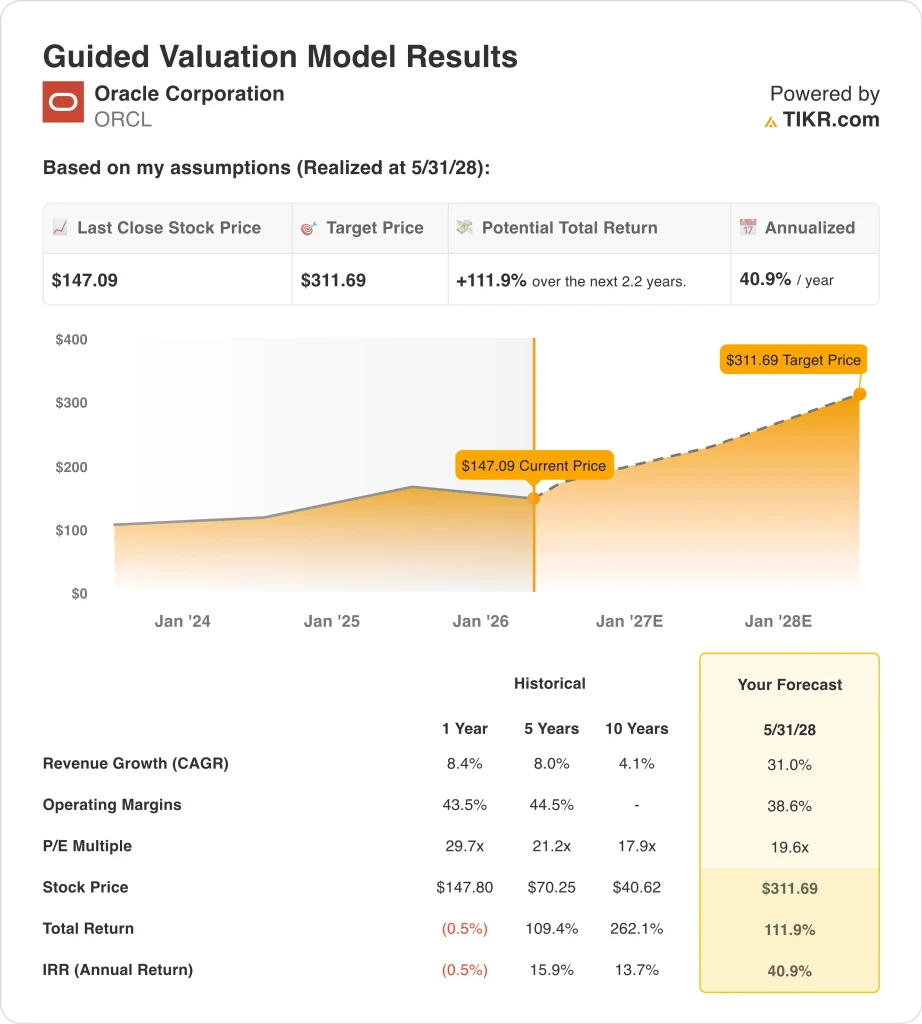

- This implies a total return of 111.9% from today’s $147 price, with an annualized return of 40.9% over the next 2.2 years.

- Oracle’s stock is moving on AI infrastructure demand, cloud backlog growth, and investor concern around capex and debt.

What Happened?

Oracle stock is under pressure in 2026, but the story is not about slowing demand. Instead, the market is debating how much value Oracle can create from its massive AI infrastructure push, and how much capital that growth will require. Shares fell 24.6% over the past roughly 0.23 years, even as Oracle posted accelerating cloud growth and raised its long-term revenue outlook.

That tension was obvious after the fiscal Q3 results on March 10. Reuters reported that Oracle beat quarterly revenue estimates and said the AI data center boom should power revenue above Wall Street estimates through at least 2027. Reuters also said the stock rose 8.3% in extended trading that day, because investors viewed the results as evidence that Oracle’s heavy AI spending was translating into real demand.

Oracle’s own release backed up that view with unusually strong numbers. Q3 revenue rose 22% to $17.2 billion, cloud revenue rose 44% to $8.9 billion, cloud infrastructure revenue rose 84% to $4.9 billion, and remaining performance obligations jumped 325% to $553 billion. Oracle also raised its fiscal 2027 revenue target to $90 billion, which was above the analyst consensus Reuters cited.

But investors are still weighing the cost of getting there. Reuters reported in December that Oracle’s capex outlook for fiscal 2026 had risen to $50 billion, and management kept that figure unchanged in the March earnings release. That helps explain why the stock can rally on AI demand one week and then slip on balance-sheet or infrastructure headlines the next.

What the Model Says for Oracle Stock

We analyzed the upside potential for Oracle stock using valuation assumptions based on its AI cloud backlog, strong infrastructure growth, and improving operating leverage.

Based on estimates of 31.0% annual revenue growth, 38.6% operating margins, and a 19.6x P/E multiple, the model projects Oracle stock could rise from $147 to $312 per share.

That would represent a 111.9% total return over the next 2.2 years. On an annualized basis, that works out to 40.9% per year.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ORCL stock:

1. Revenue Growth: 31%

Oracle’s valuation assumes 31.0% revenue growth, well above its historical levels. The company delivered 8.4% (1-year), 8.0% (5-year), and 4.1% (10-year), so the model depends on AI and cloud acceleration.

Recent results support this shift. Oracle reported 22% total revenue growth, with cloud up 44% and cloud infrastructure up 84% in Q3 2026.

Management also raised forward expectations. The company guided to $67 billion in revenue in FY2026 and $90 billion in FY2027, supported by backlog growth.

Remaining performance obligations reached $553 billion, signaling strong future demand. The key risk is how quickly Oracle can convert this backlog into revenue through capacity expansion.

2. Operating Margins: 38.6%

The model assumes 38.6% operating margins, slightly below historical levels. Oracle delivered 43.5% (1-year) and 44.5% (5-year), so the forecast already reflects some pressure.

Margins are improving despite higher spending. Operating margin increased from 27.4% in 2023 to 32.2% LTM, showing early operating leverage.

Cloud mix is a key driver of margins. Higher-margin database and application services continue to grow alongside infrastructure offerings.

However, near-term pressure remains. Free cash flow fell to (24.7) billion LTM as capex increased significantly for AI infrastructure.

3. Exit P/E Multiple: 19.6x

The model uses a 19.6x P/E, which is below recent averages. Oracle traded at 29.7x (1-year) and 21.2x (5-year), making this assumption conservative.

Current valuation aligns with this level. Oracle trades around 19.6x NTM P/E and 26.4x LTM P/E based on recent data.

Street targets remain higher than the current price. The average target is $246.46 versus $147.09 today, reflecting expected earnings growth.

Valuation will depend on execution. Investors are balancing strong AI demand with rising capex and debt levels tied to infrastructure expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for ORCL stock through 2030 show varied outcomes based on cloud growth, margin expansion, and valuation multiples (these are estimates, not guaranteed returns):

- Low Case: AI demand stays strong, but margin gains are more limited → 31.6% annual returns

- Mid Case: Oracle converts more of its AI backlog into revenue and earnings → 42.2% annual returns

- High Case: Cloud growth stays very strong, and operating leverage improves further → 52.6% annual returns

Even in the low case, Oracle’s model still points to strong returns because revenue growth remains high and earnings expand faster than the valuation multiple changes. The model also shows that Oracle does not need multiple expansions to generate strong outcomes, because all three cases assume a negative P/E change. That makes execution on backlog conversion, cloud infrastructure deployment, and margin expansion more important than sentiment alone.

Oracle’s next catalysts should help shape which path investors focus on. The company is expected to pay its next $0.50 dividend on April 9 and report Q4 2026 results on June 8. Investors will likely watch cloud infrastructure growth, remaining performance obligations, capex, and any updates on AI-related customer demand.

See what analysts think about ORCL stock right now (Free with TIKR) >>>

Should You Invest in Oracle Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ORCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ORCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Oracle Corporation stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!