Key Stats for Fair Isaac Stock

- Past-Week Performance: -0.32%

- 52-Week Range: $969.32 to $2,217.6

- Current Price: $995

What Happened?

Fair Isaac‘s credit-scoring monopoly — used by 90% of top U.S. lenders to assess consumer creditworthiness — generated $305 million in Scores revenue in Q1 FY2026, up 29% year-over-year, even as the stock trades at $995 after shedding 31% year-to-date.

Wells Fargo trimmed its price target to $2,300 from $2,500 on March 18, citing lower peer multiples, though the firm maintained its bullish stance and flagged minimal incentive for lenders to abandon FICO in favor of VantageScore, a rival credit model competing for mortgage market adoption.

Mortgage originations revenue, which alone accounted for 42% of total Scores revenue in Q1, surged 60% year-over-year, driven by both price increases and volume growth, while non-GAAP operating margin expanded 432 basis points to 54%, a level that peers including S&P Global have not matched in the credit analytics space.

On March 20, FICO closed a $1 billion senior notes offering at 6.25% due 2034, using proceeds to retire $400 million of 5.25% notes due 2026 and repay revolving credit borrowings, reducing near-term refinancing risk as total debt stood at $3.2 billion at quarter end.

CFO Steve Weber stated on the Q1 2026 earnings call that “we’re pretty confident we’re going to be able to beat our guidance,” tying his confidence directly to record software ACV bookings of $38 million in the quarter and accelerating platform ARR growth.

Five resellers representing roughly 70-80% of the reseller market have now signed onto the FICO Mortgage Direct Licensing Program, which streamlines lender access to FICO Scores, with FICO Score 10T — a meaningfully more predictive next-generation model — targeted for Direct Licensing availability in the first half of calendar 2026.

FICO’s forward case rests on three converging drivers: platform ARR of $303 million growing at 33% annually as over 150 customers expand across use cases, a Q2 guidance raise telegraphed by management, and $163 million in Q1 buybacks signaling continued capital return against a stock trading near two-year lows.

Wall Street’s Take on FICO Stock

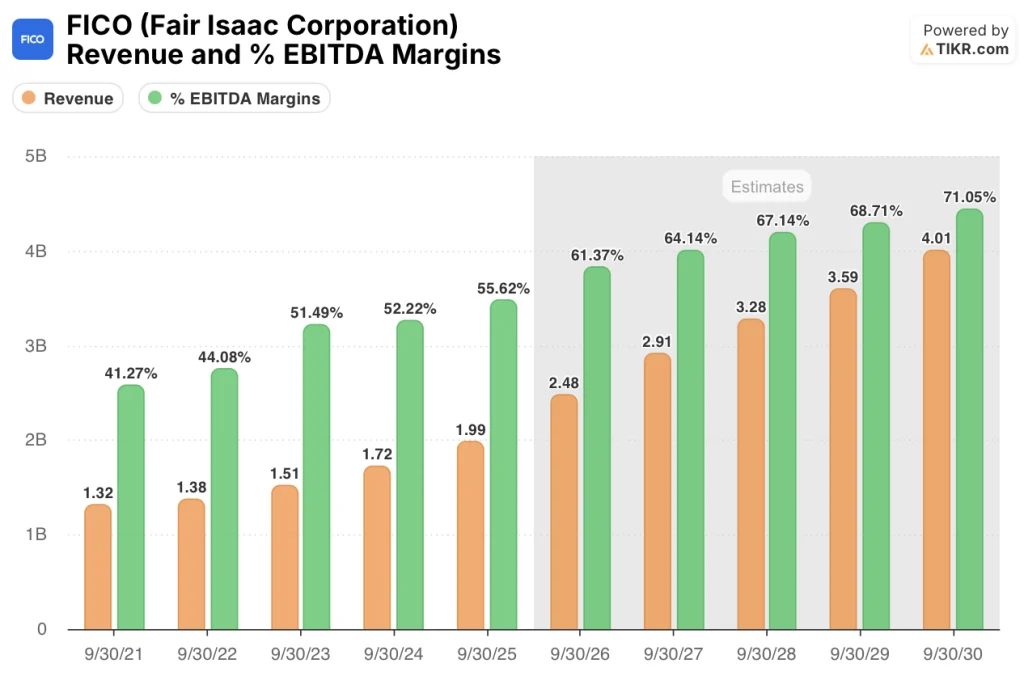

The record $38 million in Q1 software ACV bookings — annual contract value, the forward revenue signed but not yet recognized — directly supports the TIKR model’s FY2026E revenue estimate of $2.48 billion, a 24.6% jump from FY2025’s $1.99 billion, as platform ARR growing 33% annually converts bookings into durable recurring income.

Margin expansion is already arriving in the actuals: Q1 non-GAAP operating margin hit 54%, up 432 basis points year-over-year, tracking ahead of the TIKR model’s FY2026E EBITDA margin assumption of 61.4%, which itself would represent a 580-basis-point improvement from FY2025’s 55.6%, driven by operating leverage on a largely fixed-cost Scores business.

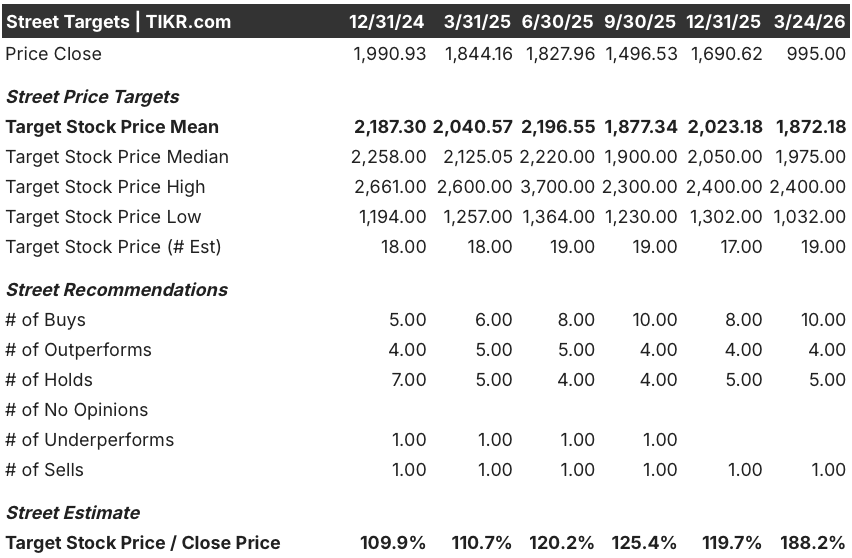

Fourteen analysts rate FICO a buy or outperform against five holds and one sell, with a mean price target of $1,872.18 — implying 88.2% upside from the current $995 close — as consensus anchors to normalized EPS growth of 40.0% in FY2026E and a free cash flow inflection to $1.03 billion, up 38.9% year-over-year.

The $1,368 spread between the street’s low target of $1,032 and high of $2,400 reflects two binary outcomes: the low anchors to a scenario where AI disruption erodes Scores pricing power or VantageScore gains mortgage market footing, while the high requires FICO Score 10T adoption across conforming and nonconforming markets to accelerate origination volumes and unit pricing simultaneously.

What Does the Valuation Model Say?

The TIKR mid-case model prices FICO at $1,953.55 by September 2030, implying a 96.3% total return and a 16.1% annualized IRR, built on a 14.4% revenue CAGR and net income margins expanding to 44.5%, assumptions grounded in the mortgage Direct Licensing Program reaching 70-80% of the reseller market and platform ARR compounding through 150-plus enterprise customers adding use cases.

The market is treating a 40.0% FY2026E normalized EPS growth company as a value trap, pricing FICO at $995 against $41.84 in estimated earnings — a 23.8x forward multiple on a business that held 90% lender penetration through the selloff.

Five resellers covering 70-80% of the mortgage market are now live or in final integration testing under the Direct Licensing Program, validating the TIKR model’s assumption that Scores revenue sustains above 20% growth through FY2026; the mid-case target of $1,953.55 requires that program to go live without a material delay.

CFO Steve Weber’s statement that “we don’t want to get into the situation where we’re continually updating our guidance every quarter” signals deliberate conservatism, not fundamental deterioration — the Q2 earnings call is the moment management’s own telegraphed guidance raise either confirms or denies the TIKR model’s 24.6% revenue growth assumption for FY2026.

If mortgage origination volumes contract materially — whether from rate increases, a credit card APR cap reducing consumer credit activity, or macro-driven lender pullback — Scores revenue, which drove 60% mortgage origination growth in Q1, decelerates sharply and the TIKR model’s $2.48 billion FY2026E revenue estimate becomes unreachable.

Watch the Q2 FY2026 earnings call for a guidance raise: management explicitly telegraphed it, and the specific number to track is whether B2B Scores revenue sustains above 30% growth, which is the operational tripwire for the TIKR model’s FY2026E normalized EPS estimate of $41.84.

Should You Invest in Fair Isaac Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FICO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fair Isaac Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FICO stock on TIKR for Free →