Key Stats for Pool Corporation Stock

- Past-Week Performance: -3.1%

- 52-Week Range: $197.7 to $345

- Current Price: $203.2

What Happened?

The world’s largest wholesale distributor of swimming pool supplies, Pool Corporation (POOL), now trades at $203.24 after shedding 32.9% in 2025, even as gross margin expanded 20 basis points to 29.7% on disciplined pricing while new U.S. pool construction hit roughly 60,000 units, half the pandemic peak.

On February 19, Pool reported Q4 adjusted EPS of $0.84, missing the $0.98 consensus, and guided FY2026 diluted EPS of $10.85 to $11.15, a midpoint of $11 that fell below the $11.62 analyst estimate, sending shares down 7.8% in premarket trading.

Gross margin in Q4 reached 30.1%, up 70 basis points year-over-year, driven by pricing discipline, supply chain execution, and expanded private label sales, outperforming the broader pool equipment sector even as Q4 revenue missed consensus by $16.9 million on hurricane recovery base effects.

Jefferies then cut its price target to $245 from $300 on February 20, maintaining a “hold” rating and citing no expected rebound in construction or repair-and-remodel activity, while noting Pool’s customer base is expanding more slowly and acquisition activity has tapered.

CEO Peter Arvan stated on the Q4 2025 earnings call that “we are starting to see the gains from that” in reference to POOL360 Unlocked, Pool’s AI-enhanced digital ordering platform, which reached a record 15% of full-year sales and peaked at 17% during pool season.

Pool’s forward position rests on three converging drivers: a variable speed pump replacement cycle building across a 6-million-plus U.S. installed base, $530 million in annual shareholder returns that management grew 10% even through the downturn, and an April 23 Q1 2026 earnings call where low single-digit revenue growth would trigger a $10 million to $15 million incentive compensation reload confirming the recovery is real.

Wall Street’s Take on POOL Stock

Pool’s Q4 gross margin expansion to 30.1% confirms the pricing discipline and supply chain execution that underpin the TIKR model’s FY2026E FCF recovery to $390 million, a 25.9% rebound from the trough of $310 million, driven by pre-season inventory purchases made ahead of vendor price increases.

The fundamental case rests on two inflections arriving simultaneously: FY2026E normalized EPS of $11, reversing three straight years of double-digit percentage declines, while FCF margin recovers from 5.9% to 7.2% as the 50-plus greenfield locations opened since 2021 begin absorbing fixed costs and contributing operating leverage.

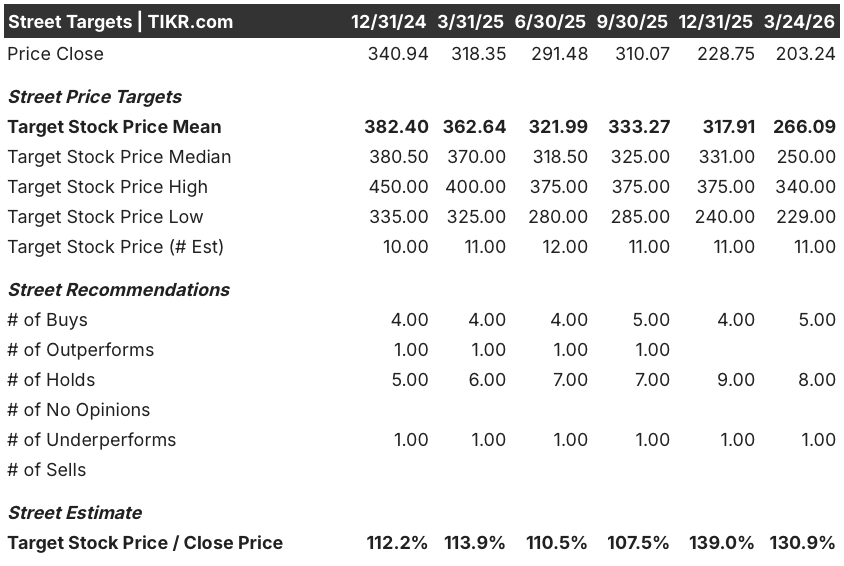

The street is cautiously positioned, with 5 buys against 8 holds and 1 underperform across 14 analysts, a mean price target of $266.09 implying 30.9% upside from $203.24, as consensus waits for the April 23 Q1 2026 results to confirm whether low single-digit revenue growth is materializing before committing to a recovery call.

The spread from the street’s low target of $229 to the high of $340 maps directly onto two competing outcomes: the low reflects a scenario where new pool construction stays near 60,000 units and discretionary spending fails to recover, while the high requires the pent-up renovation and remodel demand management described to finally translate into permit acceleration.

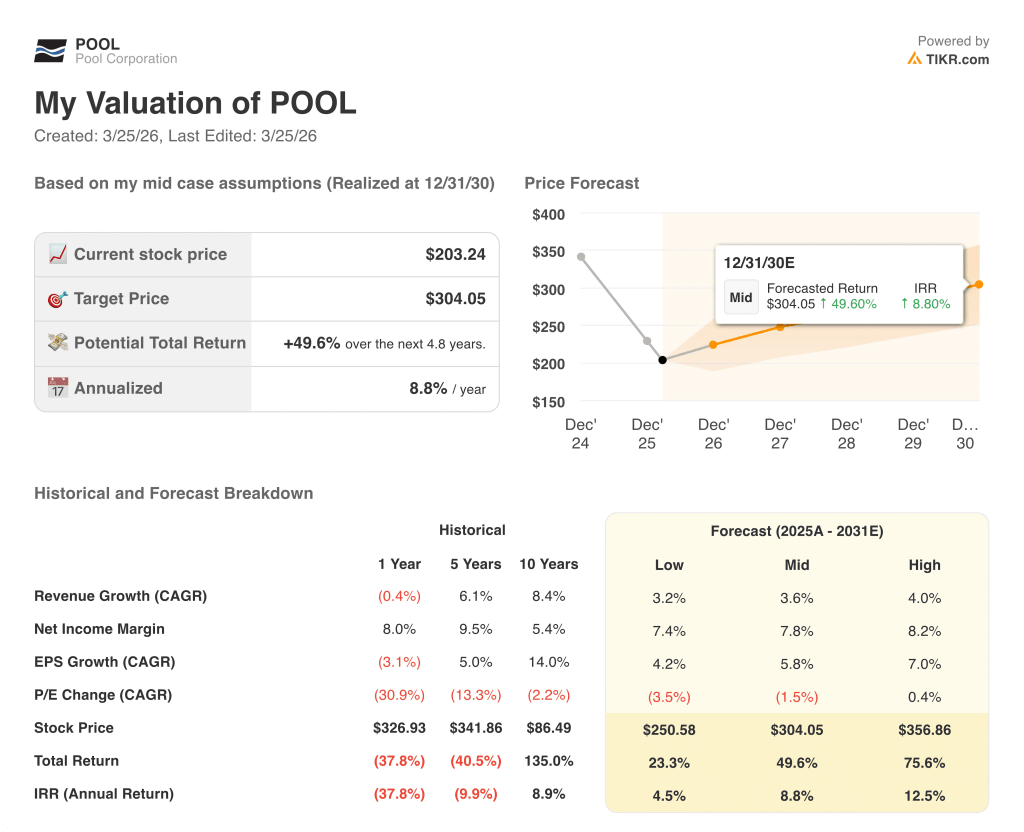

What Does the Valuation Model Say?

The TIKR mid-case model reaches $304.05 by December 2030, a 49.6% total return at an 8.8% IRR, built on a 3.6% revenue CAGR and net income margins recovering to 7.8%, assumptions grounded in POOL360 Unlocked driving digital penetration past 15% of sales and the variable speed pump replacement cycle adding incremental equipment demand.

The market is pricing Pool as though the 32.9% decline in 2025 reflects a permanent earnings reset, but gross margin expanded 20 basis points to 29.7% even in the worst year.

Four consecutive directors and officers purchased shares between February 25 and March 4, the TIKR model’s $304.05 target requires only a 3.6% revenue CAGR and 7.8% net income margins, both supported by management’s confirmed pricing pass-throughs and capacity absorption thesis.

Arvan’s February 19 statement that dealer sentiment is “much more encouraging than not” heading into the 2026 season signals the recovery thesis is operational, not speculative.

Also, if discretionary spending fails to recover and new pool construction falls below 60,000 units, the incentive compensation reload of $10 million to $15 million hits without the revenue to offset it, compressing the FY2026E EBITDA margin below 12.4% and breaking the FCF recovery assumption.

Watch the April 23 Q1 2026 earnings call for low single-digit revenue growth confirmation; that number triggers the incentive comp reload and validates the TIKR model’s $390 million FCF estimate for the full year.

Should You Invest in Pool Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up POOL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pool Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze POOL stock on TIKR for Free →