Key Takeaways:

- Eli Lilly and Company is riding a powerful wave of GLP‑1 demand, with revenue surging as Mounjaro and Zepbound scale globally.

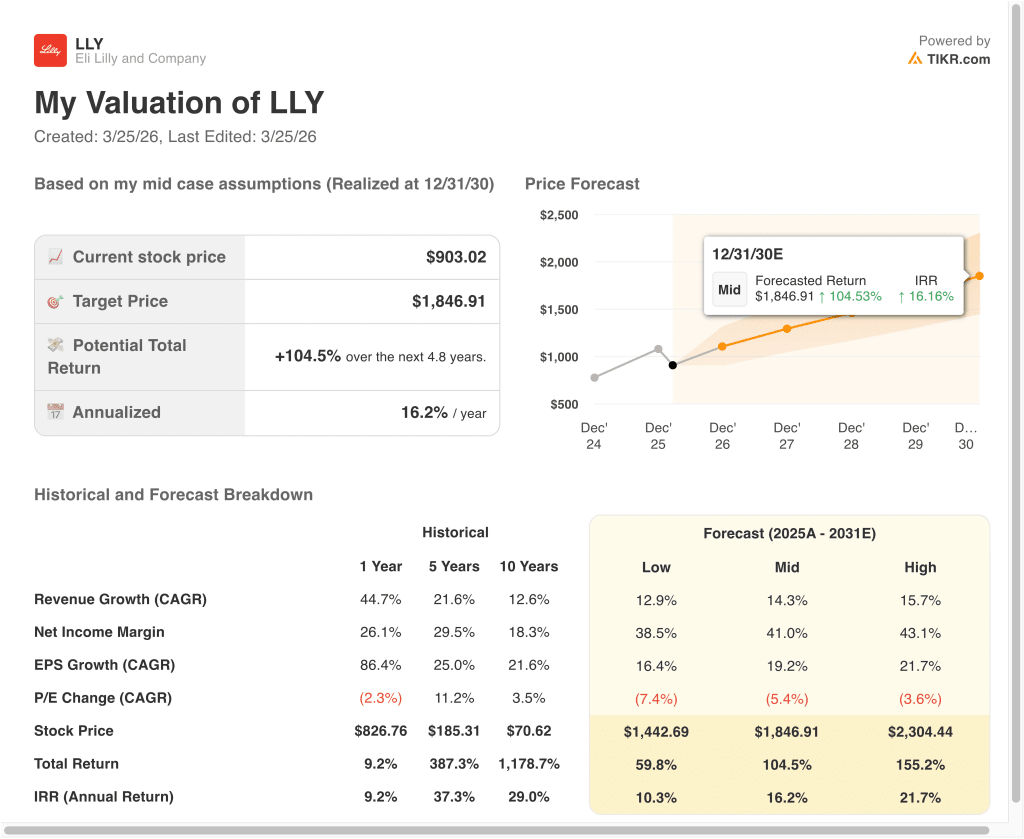

- LLY stock could reasonably reach $1,846.91 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 104.5% from today’s price of $903, with an annualized return of 16.2% over the next 4.8 years.

Eli Lilly and Company (LLY) sits at the center of the market’s obesity‑drug boom. The company develops and sells human pharmaceutical products in the U.S. and worldwide. It runs major franchises in cardiometabolic disease, oncology, immunology, and neuroscience. Its fastest‑growing products are GLP‑1‑based drugs like Mounjaro and Zepbound, which target diabetes and obesity.

Recent years show how fast the business has scaled. Revenue has climbed from the high‑$20 billion to roughly $65 billion. Growth rates moved from high teens to more than 40% as GLP‑1 sales ramped. Margins also expanded, with gross margins in the low‑80% range and operating margins in the mid‑40s. Investors now ask whether this pace can last and if today’s price already reflects years of future success.

The stock has been volatile because expectations are high. Strong earnings, upbeat guidance, and new obesity launches have pushed shares to record levels at times. Trial updates for next‑generation drugs, like retatrutide, added more excitement after showing meaningful A1C and weight reductions. But headlines about safety warnings, pricing debates, and new competitors can quickly pull the stock back. Each new data point shifts how investors think about Lilly’s long‑term earnings power.

Here’s why Eli Lilly stock could provide strong returns through 2030 as it monetizes GLP‑1 growth and scales other key franchises.

What the Model Says for LLY Stock

We analyzed the upside potential for Eli Lilly stock using valuation assumptions based on its leadership in obesity and diabetes treatments, expanding margins, and sustained revenue growth.

Based on the model, the stock could rise from $903 to $1,507 per share by 2028. That implies a 66.9% total return, or a 20.3% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for LLY stock:

1. Revenue Growth: 18%

Eli Lilly has delivered exceptional revenue growth, with recent annual growth rates exceeding 40% in the past year. This growth has been driven primarily by Mounjaro and other cardiometabolic products, which continue to gain market share globally.

The company is also expanding into obesity treatments, a market that is still in its early stages. As more patients gain access and insurance coverage improves, revenue growth could remain elevated. Additionally, international expansion provides another layer of upside.

Based on analysts’ consensus estimates, we use an 18% revenue growth assumption. This reflects strong demand but also considers potential normalization as supply constraints ease and competition increases.

2. Operating Margins: 48.5%

Lilly’s operating margins have historically been strong, with recent levels around 31.8%. However, margins are expected to expand significantly as high-margin GLP-1 drugs scale and manufacturing efficiencies improve.

The company benefits from pricing power in its core products, especially given limited competition in certain indications. As production scales, fixed costs are spread over higher volumes, which supports margin expansion.

At the same time, Lilly continues to invest heavily in R&D and manufacturing capacity. These investments may temporarily pressure margins but are essential for long-term growth.

Based on analysts’ consensus estimates, we assume a 48.5% operating margin, reflecting both scale benefits and a favorable product mix shift toward higher-margin therapies.

3. Exit P/E Multiple: 9.4x

Lilly currently trades at a premium valuation, with a P/E multiple around the mid-20s. This reflects strong growth expectations and its leadership position in a rapidly expanding market.

Historically, pharmaceutical companies with breakthrough products have commanded higher multiples. However, as growth stabilizes, multiples often compress toward more normalized levels.

Based on analysts’ consensus estimates, we use a 26.0x exit P/E multiple, which balances Lilly’s growth profile with potential future normalization. This assumption aligns with current market expectations while remaining conservative relative to peak valuations.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CVS stock through 2030 show varied outcomes based on margin recovery and execution (these are estimates, not guaranteed returns):

- Low Case: Growth slows due to competition or pricing pressure → 10.3% annual returns

- Mid Case: Continued strong adoption of GLP-1 drugs → 16.2% annual returns

- High Case: Accelerated global expansion and new indications → 21.7% annual returns

Even in the conservative case, the stock offers double-digit returns, supported by strong demand and expanding margins. The mid and high cases reflect the potential for Lilly to dominate a large and growing market.

Recent stock movements are closely tied to updates around supply expansion and demand visibility. Investors are reacting to both the pace of manufacturing scale-up and ongoing prescription growth data.

Additionally, macro factors like healthcare policy and drug pricing discussions can influence sentiment. However, Lilly’s differentiated products provide some insulation from broader industry pressures.

Financially, the company continues to show strong efficiency metrics, including gross margins near 77.7% and EBIT margins above 21%. These figures reinforce the strength of its business model and support premium valuation multiples.

At the same time, forward growth expectations remain robust, with projected revenue CAGR around 10% and EBITDA growth near 9.6% over the next two years. These metrics indicate that while growth may normalize, it remains strong relative to peers.

See what analysts think about LLY stock right now (Free with TIKR) >>>

Should You Invest in Eli Lilly and Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LLY, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track LLY alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Eli Lilly stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!