Key Takeaways:

- Carnival reported record 2025 revenue of $26.6 billion, record adjusted EBITDA of $7.2 billion, and net income of $2.8 billion, which helps explain why investors still view the cruise operator as a recovery story with improving earnings quality.

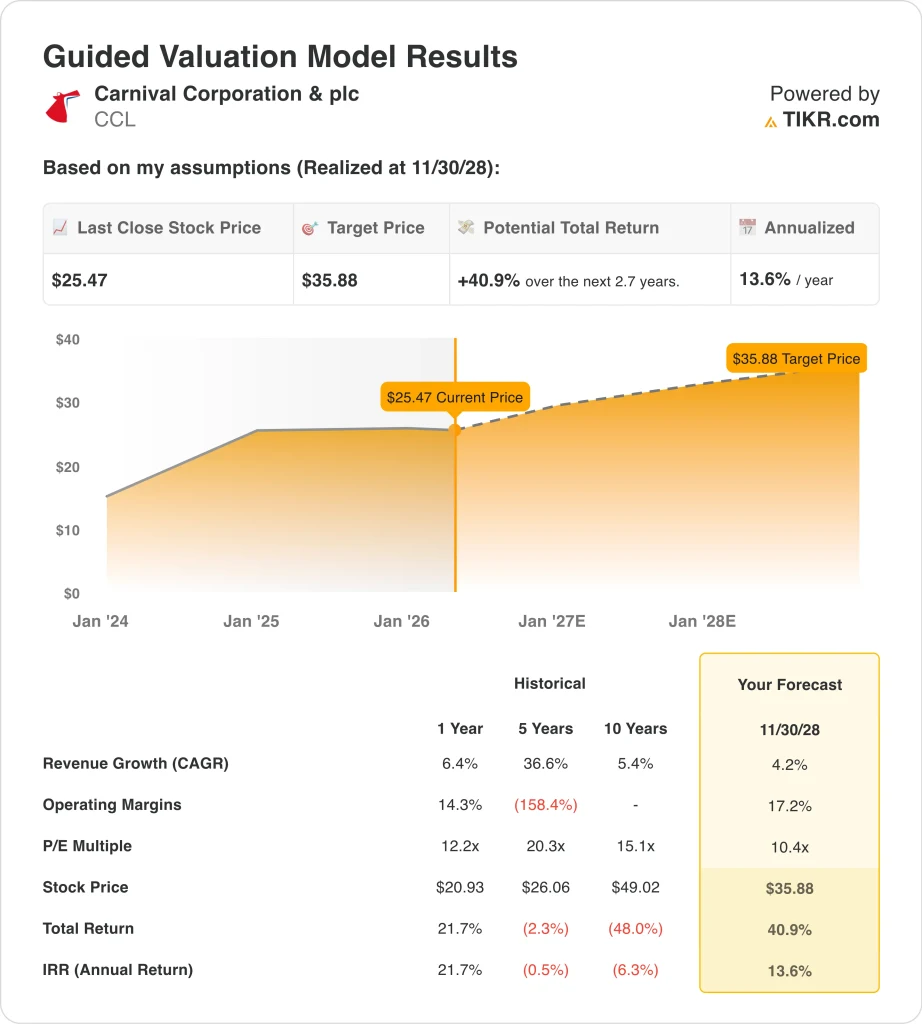

- CCL stock could reasonably reach $36 per share by November 2028, based on our valuation assumptions.

- This implies a total return of 41% from today’s $26 price, with an annualized 14% return over the next 2.7 years.

- Rising oil prices have created a key near-term risk because Reuters reported Carnival is the only major U.S. cruise line that does not hedge fuel, making the stock more sensitive to energy shocks.

What Happened?

Carnival Corporation (CCL) has become relevant again this week because investors are balancing strong operating momentum against a fresh rise in fuel risk. The company is set to report first-quarter 2026 results on March 27, and that event matters because it should give the market an updated view on bookings, yields, and costs heading into the key summer season. Carnival’s investor relations site says the conference call will be held on March 27 at 10:00 a.m. Eastern time.

The tone around the stock has turned more cautious than bearish. Carnival finished fiscal 2025 with record revenue of $26.6 billion, record adjusted EBITDA of $7.2 billion, and a net debt to adjusted EBITDA ratio of 3.4x, which was good enough for Fitch to recognize investment-grade leverage metrics. CEO Josh Weinstein said, “2025 was a truly phenomenal year,” and added that “the momentum is carrying into 2026,” helped by historical high pricing and occupancy for the booked position.

That strong setup has been challenged by a macro issue that investors cannot ignore. Carnival could be the hardest hit among major U.S. cruise operators from higher oil prices because it does not hedge fuel, and the company said a 10% rise in fuel cost per metric ton would reduce 2026 net income by $145 million. That helps explain why cruise stocks have swung with each move in energy markets and geopolitical headlines.

At the same time, travel demand has remained firm enough to support the group. Cruise and airline demand trends continue to show resilience, even as fuel prices rise. In plain language, investors are weighing whether higher costs can be passed on through strong ticket prices and onboard spending, which is why Carnival’s stock keeps moving with both booking confidence and oil.

What the Model Says for CCL Stock

We analyzed the upside potential for Carnival stock using valuation assumptions based on its steadier growth profile, improving margins, and still-moderate earnings multiple.

Based on estimates of 4.2% annual revenue growth, 17.2% operating margins, and a 10.4x P/E multiple, the model projects CCL stock could rise from $25 to $36 per share.

That would be a 40.9% total return, or a 13.6% annualized return over the next 2.7 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CCL stock:

1. Revenue Growth: 4.2%

Carnival’s revenue rebound is now maturing into a more normalized growth story. Total revenue rose from $21.6 billion in 2023 to $25.0 billion in 2024 and then to $26.6 billion in 2025, while year-over-year growth slowed from 77.4% in 2023 to 15.9% in 2024 and 6.4% in 2025. That pattern supports using a lower forward growth rate than the post-pandemic rebound years, while still recognizing that demand remains healthy.

Management’s latest commentary supports that view. Carnival said its cumulative advanced booked position for 2026 remained in line with 2025 record levels at historical high prices in constant currency, and the earnings presentation said about two-thirds of 2026 was already booked at historical high pricing and occupancy. Based on those facts, a 4.2% revenue growth assumption looks aligned with the company’s current booking strength and forward expectations.

2. Operating Margins: 17.2%

Carnival’s margin recovery is one of the clearest reasons the stock has re-rated. Gross margin improved from 50.1% in 2023 to 53.5% in 2024 and 55.5% in 2025, while operating margin improved from 8.6% to 14.1% to 16.4% over the same period. Operating income reached $4.4 billion in 2025, which means more of each revenue dollar is now flowing through to profit.

The latest quarter also showed that pricing and cost control are still working together. Carnival reported fourth-quarter adjusted EBITDA of $1.5 billion, adjusted EBITDA margin expansion of nearly 300 basis points year over year, and disciplined cost growth excluding fuel. A 17.2% operating margin assumption is therefore only a modest step above the latest 16.4% LTM EBIT margin.

3. Exit P/E Multiple: 10.4x

Carnival still trades at a valuation that reflects both progress and caution. The stock trades around 12.6x LTM P/E, while historical multiples have been higher. That gap suggests analysts see upside, but the market still discounts the stock for leverage and macro sensitivity.

Using a 10.4x exit P/E therefore builds in continued skepticism rather than full multiple expansion. Carnival ended the latest period with $26.1 billion of net debt and 3.43x net debt to EBITDA, even after major balance sheet improvement. So the model assumes investors keep assigning the stock a restrained multiple unless debt keeps falling and earnings keep compounding.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CCL stock through 2030 show varied outcomes based on booking strength, fuel costs, and continued deleveraging (these are estimates, not guaranteed returns):

- Low Case: Fuel costs remain elevated, and pricing power weakens slightly → 10l2% annual returns

- Mid Case: Strong demand and steady deleveraging support earnings growth → 14.6% annual returns

- High Case: Continued pricing strength and margin expansion with stable fuel costs → 18.6% annual returns

Even in the conservative case, Carnival stock offers positive returns supported by stronger earnings, rising customer deposits, and a balance sheet that is moving in the right direction, though the next major catalyst is still the March 27 earnings report.

See what analysts think about CCL stock right now (Free with TIKR) >>>

Should You Invest in Carnival Corporation & plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Carnival Corporation stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!