Key Stats for CoStar Stock

- Past-Week Performance: -3.4%

- 52-Week Range: $40.8 to $97.4

- Current Price: $41.5

What Happened?

CoStar Group (CSGP), a real estate data and marketplace platform generating $3.2 billion in annual revenue, posted its 59th consecutive quarter of double-digit revenue growth while its residential business crossed $1.46 billion in 2025 revenue, yet the stock trades at $41.46, near its 52-week low of $40.78.

CoStar reported Q4 revenue of $900 million against the IBES estimate of $886 million, with adjusted EPS of $0.31 beating the $0.27 consensus, while guiding Q1 2026 revenue of $890 million to $900 million and full-year adjusted EBITDA of $740 million to $800 million.

Homes.com, CoStar’s residential listings portal competing directly against Zillow and Realtor.com, grew 63% in 2025 and crossed $100 million in annualized agent subscription revenue with 31,000 subscribers, while Zillow’s rental traffic fell 48% year-over-year in January per comScore data.

Andrew Florance, Founder and CEO, stated on the Q4 2025 earnings call that “in just 2 years, Homes.com has become the fastest-growing residential portal in the U.S.,” underpinned by January 2026 organic traffic rising 134% year-over-year and Homes AI users spending 16 minutes 50 seconds per session versus 4 minutes 24 seconds for non-AI users.

CoStar’s $1.5 billion share repurchase program, a targeted 26% residential revenue growth in 2026, management’s long-term projection of $4.75 billion in Homes.com revenue, and a clear EBITDA expansion glide path toward 50% residential margins position the company as the most data-entrenched challenger to incumbent real estate portals over the next decade.

Wall Street’s Take on CSGP Stock

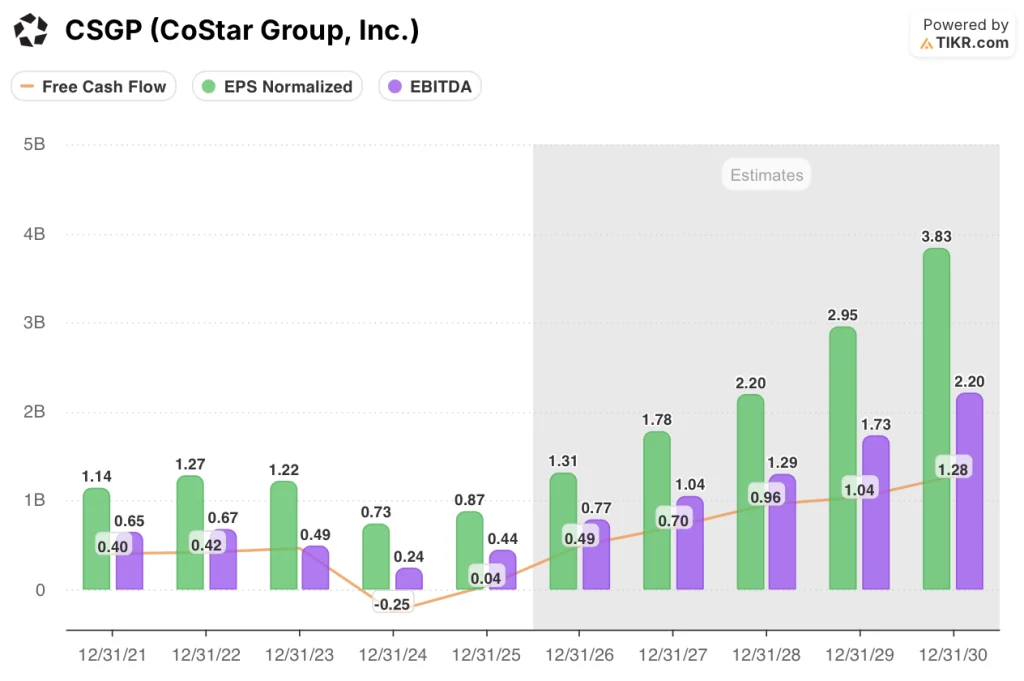

The 59-quarter revenue growth streak confirms CoStar’s top-line durability, but the real inflection now is free cash flow, which recovered from negative $250 million in 2024 to $40 million in 2025 as Homes.com brand-launch spending peaks.

The TIKR model projects 2026 normalized EPS of $1.31, up 50.6% from $0.87 in 2025, anchored by the $300 million reduction in Homes.com net investment and EBITDA expanding from $442 million to a midpoint of $770 million as marketing spend front-loads into Q1 and Q2 then fades.

Fifteen of nineteen covering analysts rate CSGP a buy or outperform, with a mean price target of $64.89 implying 56.5% upside from $41.46, reflecting Street confidence in Homes.com’s 63% revenue growth rate and the company’s confirmed residential profitability path in 2026.

The analyst price target range spans $40.00 to $100.00, a spread that maps directly to two known variables: the low anchors to continued Homes.com execution risk and the CMA hotel data probe, while the high assumes Homes AI engagement converts subscribers at scale and LoopNet’s 43% sales force expansion delivers.

What Does the Valuation Model Say?

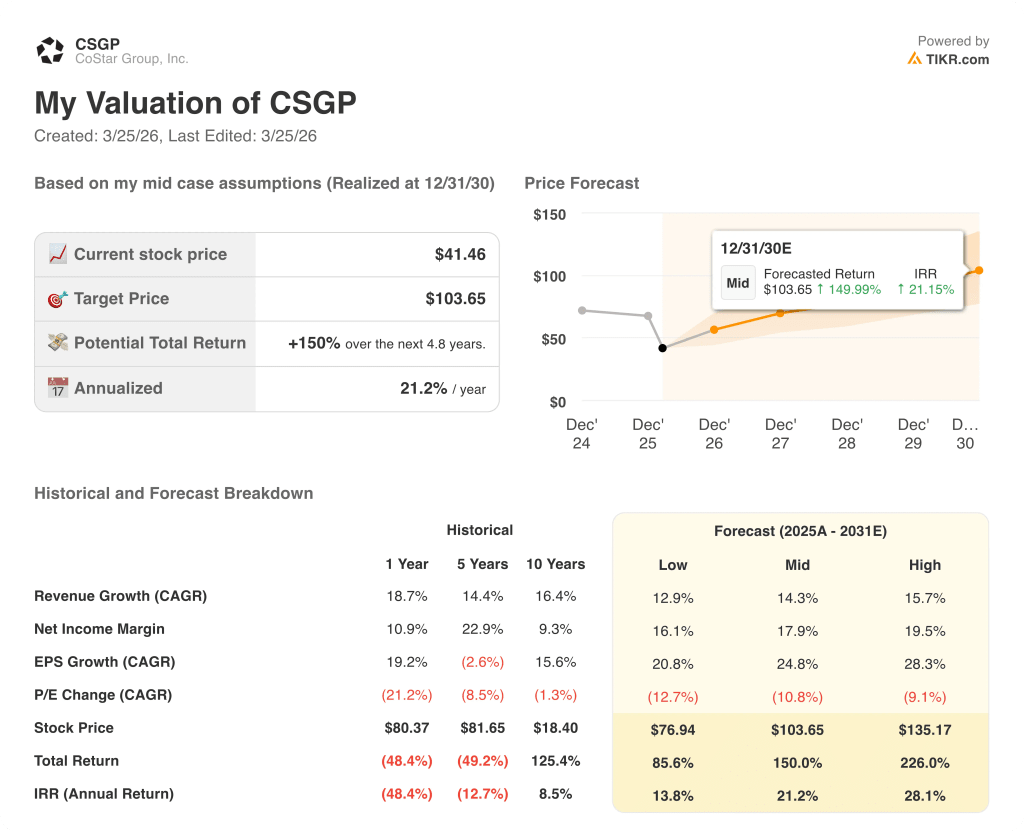

The TIKR mid-case target of $103.65, implying a 150% total return and 21.2% IRR by December 2030, is built on a 14.3% revenue CAGR and net income margins expanding from 11.2% in 2025 to 17.9% by 2030, both supported by the Homes.com investment glide path and confirmed CoStar Australia and LoopNet Europe expansion.

The market is pricing CSGP near its 52-week low while FCF is set to expand from $40 million in 2025 to $490 million in 2026, a 1,101.6% jump the stock price has not acknowledged.

Homes AI users submit 7x more email leads than non-users, a unit economics signal that directly supports the TIKR model’s assumption of accelerating Homes.com subscriber growth toward the $103.65 target.

Also, management’s confirmation of residential segment profitability in 2026, backed by a $500 million accelerated share repurchase already executing this quarter, signals this is a deliberate capital return inflection, not a distressed valuation.

The one development that breaks the model is Homes.com subscriber growth stalling; at 31,000 agents generating $100 million annualized revenue against 750,000 targeted top agents, any deceleration collapses the residential margin expansion timeline.

Watch Q1 2026 residential revenue against the $420 million to $425 million guidance range; a miss signals Homes AI engagement has not yet converted to paid subscriptions at the pace the model requires.

Should You Invest in CoStar Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CSGP stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CoStar Group, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze CSGP stock on TIKR for Free →