Key Takeaways:

- Disney is entering a new chapter after Josh D’Amaro officially became CEO in March, while the market weighs leadership change against steady gains in streaming, parks, and cash flow.

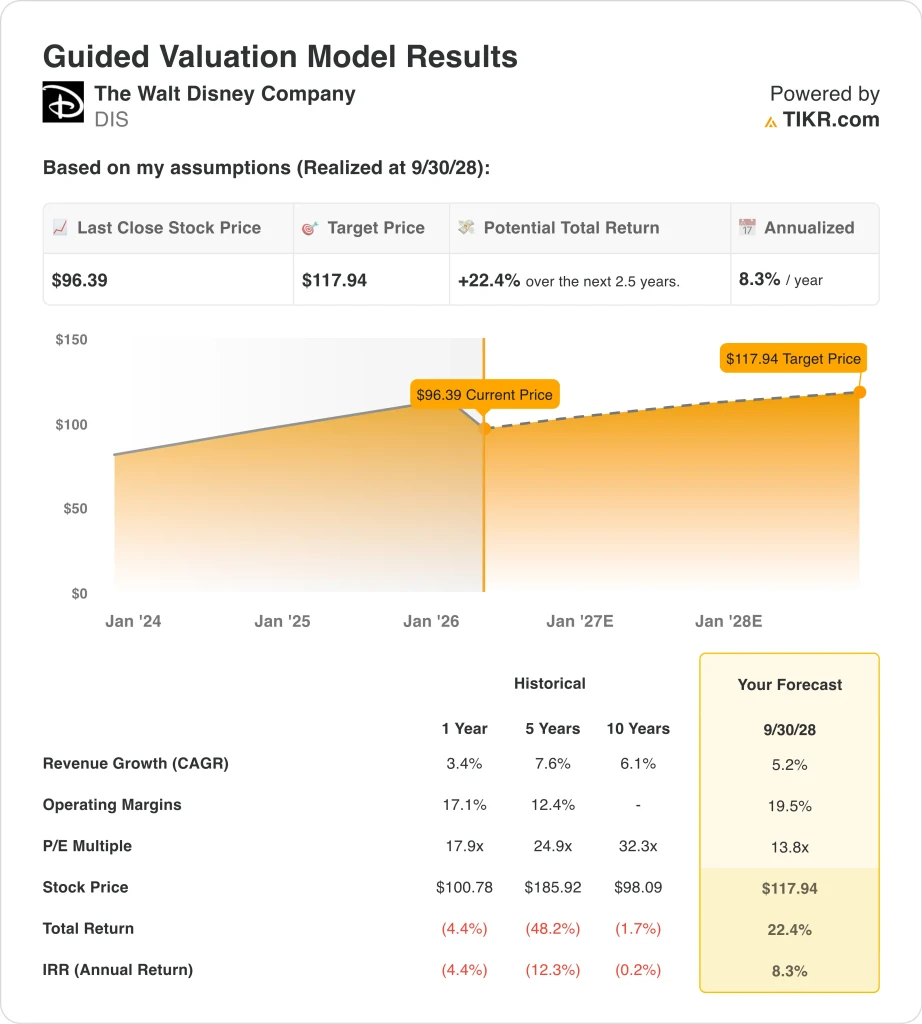

- DIS stock could reasonably reach $118 per share by September 2028, based on our valuation assumptions.

- This implies a total return of 22.4% from today’s $96 price, with an annualized 8.3% return over the next 2.5 years.

- Disney’s latest quarter showed 5.0% revenue growth to $26.0 billion and adjusted EPS of $1.63, but the stock has still been under pressure as investors reassess succession, streaming competition, and valuation after a weak recent share-price trend.

What Happened?

The Walt Disney Company (DIS) is relevant right now because the story changed from turnaround to transition. Josh D’Amaro officially took over as CEO at the March 18 annual shareholder meeting, ending the long succession debate around Bob Iger. That matters because investors are now judging whether Disney can keep improving operations while changing leadership at the top. D’Amaro told employees Disney would work more as “one Disney” and focus on more personalized and engaging consumer experiences.

The tone around the stock has become more cautious than enthusiastic. Disney beat first-quarter fiscal 2026 expectations, with adjusted EPS of $1.63, and revenue rose 5.0% to $26.0 billion. Yet the stock still fell sharply over the past three months, and that suggests investors want more proof that earnings growth can continue after a strong 2025.

The core business has improved, but the market is still sorting out what deserves a premium multiple. Streaming is now profitable, parks remain Disney’s biggest earnings engine, and the company keeps using its brands across film, TV, sports, consumer products, and experiences. But leadership change, media disruption, and fresh questions around AI partnerships have kept Disney in debate mode rather than full rerating mode.

There is also a broader media backdrop affecting sentiment. Investors are watching how Disney handles AI, smart-TV distribution issues, and the changing economics of traditional television. The recent OpenAI and Sora headlines added one more reminder that big media companies are navigating both opportunity and disruption at the same time.

What the Model Says for DIS Stock

We analyzed the upside potential for Disney stock using valuation assumptions based on its improving margins, moderate revenue growth, and a lower earnings multiple than its historical average.

Based on estimates of 5.2% annual revenue growth, 19.5% operating margins, and a normalized P/E multiple of 13.8x, the model projects Disney stock could rise from $96.39 to $117.94 per share.

That would be a 22.4% total return, or an 8.3% annualized return over the next 2.5 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DIS stock:

1. Revenue Growth: 5.2%

Disney’s revenue growth has become steadier, but not spectacular. Total revenue rose from $88.9 billion in 2023 to $91.4 billion in 2024 and then to $94.4 billion in 2025, while first-quarter fiscal 2026 revenue reached $26.0 billion, up 5.0% from a year earlier. That pattern supports a mid-single-digit growth assumption because Disney is no longer in rebound mode, but it is still expanding across multiple businesses.

The company’s growth drivers are now more balanced. Experiences continues to benefit from strong guest spending and high demand for parks and cruises, while Entertainment has improved as streaming losses have narrowed and content monetization has become more disciplined. Sports also remain important because ESPN still gives Disney a major live-content asset as traditional TV bundles keep evolving.

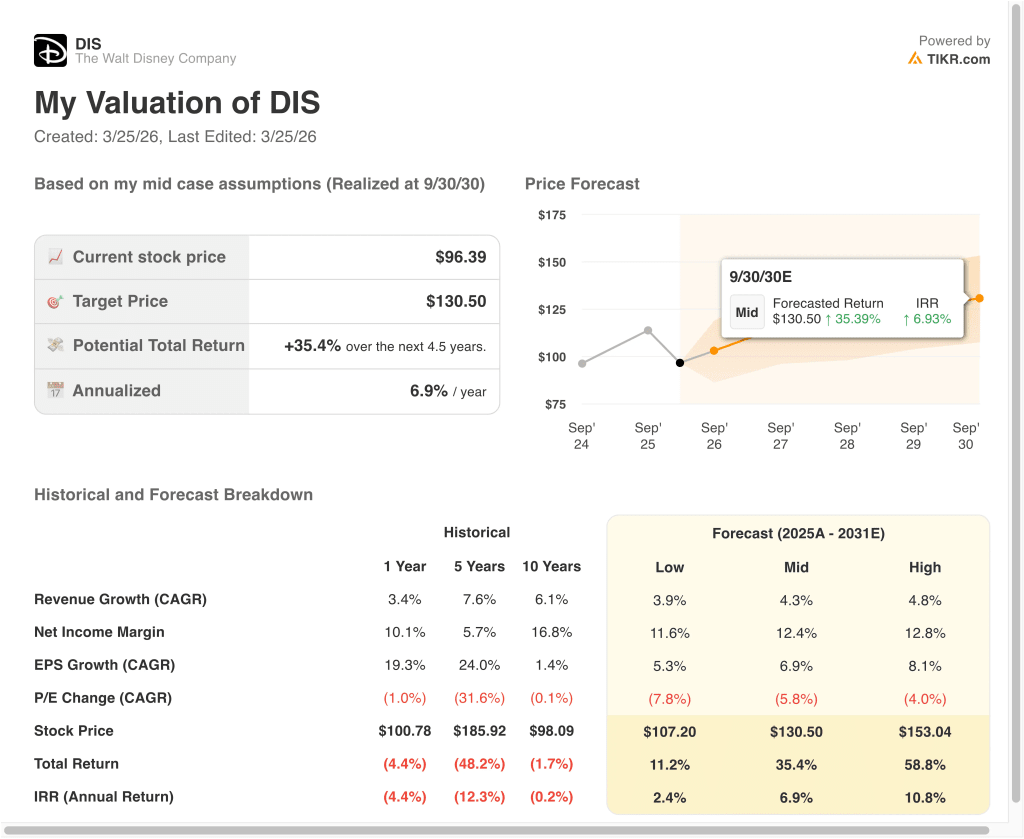

The overview shows a forward 2-year revenue CAGR of 5.7%, while the advanced model’s mid-case uses 4.3% growth through 2030. That means the 2028 model is asking for solid but not heroic revenue expansion, which feels consistent with Disney’s current size and mix.

2. Operating Margins: 19.5%

Margin expansion is the most important part of Disney’s valuation story. Operating margin improved from 10.5% in 2023 to 13.5% in 2024 and 14.9% in 2025, while the LTM EBIT margin stands at 14.6%. Gross margin also improved from 33.4% in 2023 to 37.8% in 2025, which shows that the business is becoming more efficient again.

The market cares about this because Disney used to be seen as a margin-repair story. Streaming profitability, better cost control, and the strength of Experiences have changed that narrative. First-quarter fiscal 2026 results continued the trend, with total segment operating income up year over year, which supports the idea that the company can keep lifting profitability if execution remains disciplined.

Still, 19.5% is a fairly ambitious operating margin assumption relative to where Disney is today. It implies further gains from streaming, continued resilience in parks, and better monetization across the portfolio. That can happen, but it also explains why the stock is not obviously cheap, because part of the valuation already depends on Disney converting recent operational progress into a structurally higher-margin business.

3. Exit P/E Multiple: 13.8x

Disney does not need a premium multiple for the model to work. The guided valuation uses a 13.8x exit P/E, which matches the NTM P/E and sits below Disney’s 1-year historical P/E of 17.9x and far below its 5-year historical P/E of 24.9x from the guided model image. So this assumption is conservative relative to Disney’s own history.

That lower multiple reflects how investors still view the business. Disney has better earnings, but it also faces structural questions around television, content spending, and succession after Bob Iger. A lower exit multiple says the market may continue to treat Disney as a solid but slower-growing media and experiences company, rather than as a high-multiple growth story.

The balance sheet supports that cautious framing. Disney’s LTM net debt stands at about $41.0 billion, and net debt to EBITDA is 2.0x. That is manageable, and debt has declined from earlier years, but it still means part of Disney’s investment case depends on steady free cash flow and disciplined capital returns instead of pure multiple expansion.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for DIS stock through 2030 show varied outcomes based on streaming execution, park demand, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Streaming growth slows, park demand softens, and the valuation compresses further → 2.4% annual returns

- Mid Case: Disney keeps improving margins, grows revenue steadily, and delivers more balanced earnings growth → 6.9% annual returns

- High Case: Streaming scales, Experiences stays strong, and investor confidence improves around the new leadership team → 10.8% annual returns

Even in the conservative case, Disney stock offers positive returns supported by its unmatched portfolio of brands, improving profitability, and strong cash generation. Free cash flow rose from $4.9 billion in 2023 to $8.6 billion in 2024 and then to $10.1 billion in 2025, before reaching $7.1 billion on an LTM basis. That matters because Disney has more room to invest in growth, pay dividends, and repurchase stock when cash generation is healthy.

The mid-case likely depends on Disney continuing to execute across all three major segments. Entertainment needs to keep improving streaming economics, Sports needs to preserve the value of ESPN, and Experiences needs to remain a dependable earnings base.

The high case would require a cleaner narrative and stronger confidence from investors. Disney would probably need more evidence that the CEO transition is working, that streaming can remain profitable, and that park demand can hold up even in a slower economy. If those pieces fall into place, the stock could earn a better outcome, but the current models suggest Disney looks more like a steady compounder than a dramatic rerating candidate.

See what analysts think about DIS stock right now (Free with TIKR) >>>

Should You Invest in The Walt Disney?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DIS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DIS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze The Walt Disney stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!