Key Takeaways:

- PayPal’s current stock price of $44 reflects slowing revenue growth and continued pressure in its branded checkout business, despite improving profitability and strong free cash flow generation.

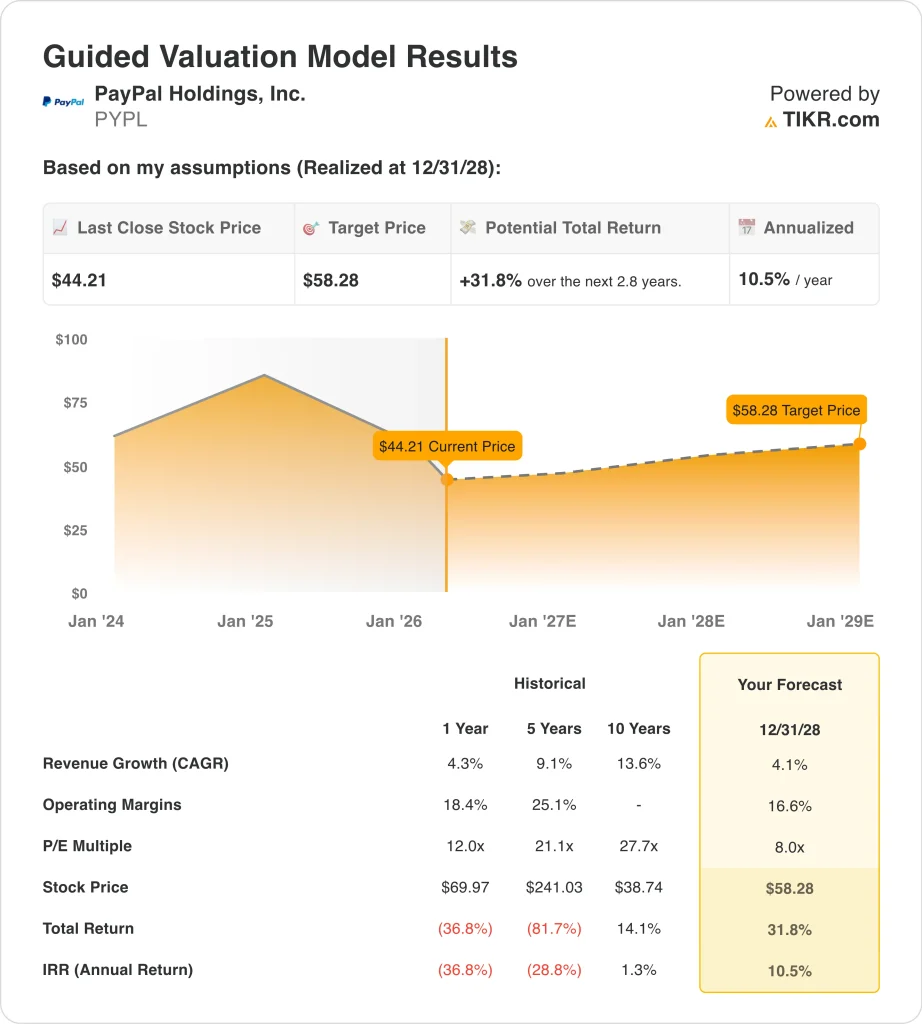

- The valuation model points to a $58 target price, implying +31.8% total return and 10.5% annualized returns, driven primarily by modest revenue growth and stable margins.

- The key debate for investors is whether PayPal can stabilize checkout performance and reaccelerate growth while maintaining its strong operating efficiency.

What Happened?

PayPal (PYPL) stock has been under pressure in recent weeks, declining sharply after a combination of weak sentiment drivers and company-specific developments. The company was removed from the S&P 100 index on March 23, 2026, which can trigger passive fund selling and reduce institutional demand. This type of index-related flow often creates short-term price pressure even when fundamentals remain intact.

At the same time, investors are reacting to ongoing concerns around PayPal’s core branded checkout product, which has faced increasing competition from Apple Pay and other digital wallets. During its recent earnings call, management acknowledged pressure across its retail merchant portfolio, reinforcing concerns that growth in its highest-margin segment is slowing. This matters because branded checkout historically drives higher take rates and profitability compared to unbranded processing.

Legal and governance concerns have also weighed on sentiment. PayPal is currently facing securities class action lawsuits tied to alleged misstatements following a significant stock decline. While these cases are ongoing, they add uncertainty and can impact investor confidence, particularly during a period of leadership transition.

On the strategic front, PayPal has introduced new initiatives such as expanding its stablecoin (PayPal USD) and enabling Venmo cross-border transfers across 90 markets. These moves highlight efforts to diversify growth and expand its ecosystem, but they are still early relative to the scale of its core checkout business. Investors appear to be taking a wait-and-see approach on whether these initiatives can materially offset slowing growth.

What the Model Says for PYPL Stock

We analyzed PayPal stock using a valuation framework based on revenue growth, operating margins, and earnings multiples.

Based on estimates of 4.1% annual revenue growth, 16.6% operating margins, and an 8x P/E multiple, the model projects PYPL stock could rise from $73 to $97 per share.

That would represent a 31.8% total return, or 10.5% annualized returns over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PYPL stock:

1. Revenue Growth: 4.1%

PayPal’s revenue has grown steadily but at a declining rate in recent years, reaching over $33 billion with growth of approximately 4.3% in the most recent period. This suggests the business is transitioning into a more mature phase. A 4.1% growth assumption reflects continued expansion without assuming a return to higher growth levels. It balances stability with competitive pressures.

The company’s growth drivers include Venmo monetization, enterprise payments, and new financial products. These areas provide incremental upside but are not yet large enough to significantly accelerate overall growth. At the same time, competition in digital wallets and checkout continues to weigh on performance. This combination supports a conservative growth outlook.

2. Operating Margins: 16.6%

PayPal’s operating margins have improved over time, reaching approximately 18.7% in recent results. However, the model assumes 16.6% to reflect potential reinvestment and competitive pricing pressure. This provides a margin of safety in the valuation. It also acknowledges that sustaining peak margins may be challenging.

The company continues to invest in product development, customer engagement, and new initiatives. These investments are necessary for long-term competitiveness but may impact near-term margins. Even so, PayPal remains highly profitable relative to peers. Margin strength is a key pillar of the investment case.

3. Exit P/E Multiple: 8x

The model applies an 8.0x P/E multiple, which is below PayPal’s historical averages. This reflects a structural re-rating of the stock as growth slows. Investors are no longer willing to pay premium multiples for the business. The lower multiple is consistent with a more mature company profile.

This assumption is critical because valuation multiples have a large impact on returns. Even with stable earnings growth, a declining multiple can limit upside. The model, therefore, remains conservative in its expectations. It does not rely on multiple expansions to drive returns.

Build your own Valuation Model to value any stock (It’s free!) >>>

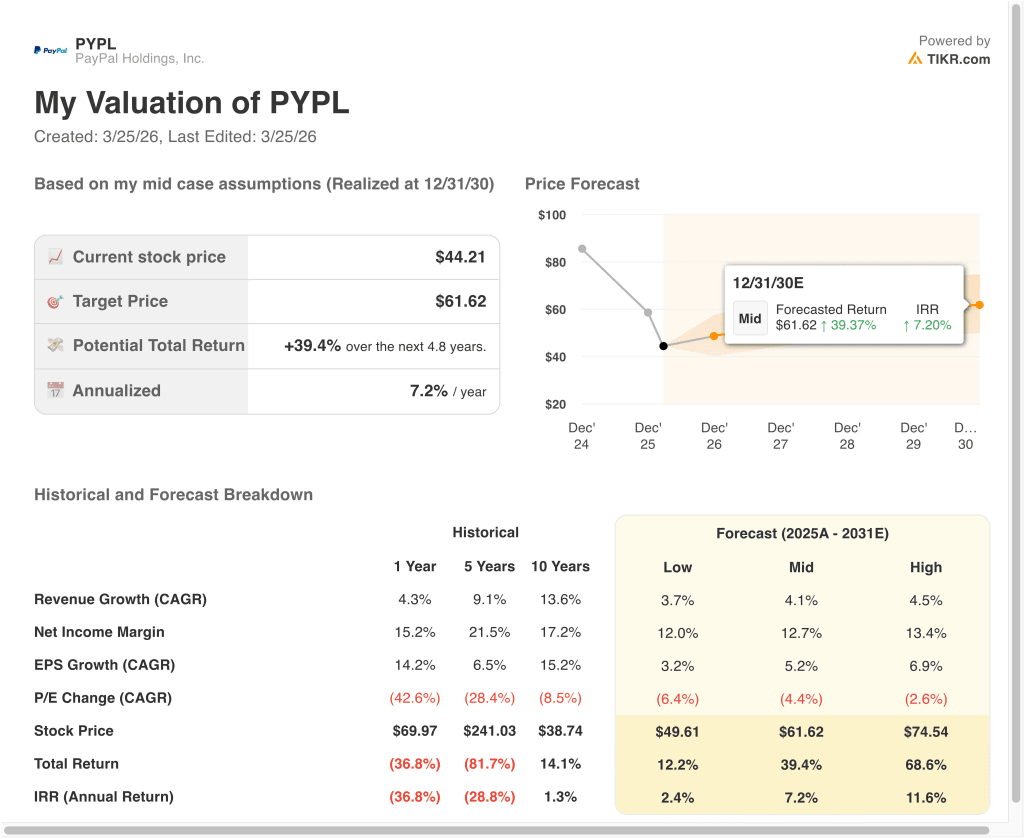

What Happens If Things Go Better or Worse?

Different scenarios for PYPL stock through 2028 show varied outcomes based on growth, margins, and valuation (these are estimates, not guaranteed returns):

- Low Case: Slower growth and continued checkout pressure → 2.4% annual returns

- Mid Case: Stable growth with solid margins and execution → 10.5% annual returns

- High Case: Improved checkout performance and stronger monetization → 11.6% annual returns

In the low case, PayPal faces continued pressure in its core checkout business and slower adoption of new initiatives. Revenue growth slows to 3.7%, and margins decline to 12.0%. The stock reached $50, implying a 12.2% total return and 2.4% annualized returns. This scenario highlights the downside risk tied to execution challenges and competitive pressure.

In the mid case, PayPal continues to grow at a steady pace while maintaining profitability. Revenue grows at 4.1%, and margins remain stable around current levels. The stock reached $58, delivering a 31.8% total return and 10.5% annualized returns. This reflects a balanced outcome where the business performs consistently but does not materially reaccelerate.

In the high case, PayPal could deliver stronger performance if branded checkout stabilizes and newer initiatives like Venmo monetization and international expansion contribute more meaningfully to growth. Revenue growth could reach 4.5%, with margins improving to 13.4% as execution strengthens. Under this scenario, the stock could reach $75, implying a 68.6% total return. This outcome would require both operational improvement and stronger investor confidence.

See what analysts think about PYPL stock right now (Free with TIKR) >>>

Should You Invest in PayPal Holdings, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PYPL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track PYPL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze PayPal stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!