Key Stats for Freshpet Stock

- Past-Week Performance: -15.7%

- 52-Week Range: $46.8 to $89.9

- Current Price: $58.9

What Happened?

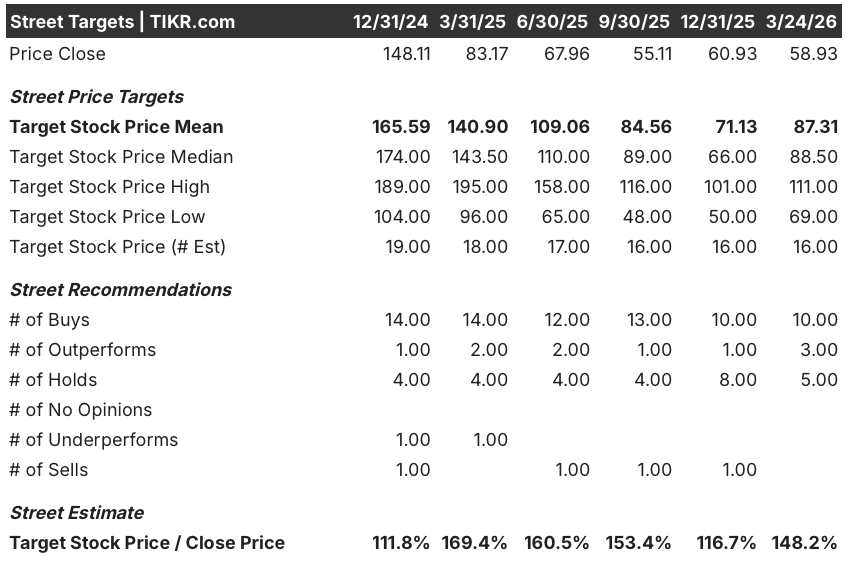

After a 60% stock collapse in 2025 that priced Freshpet (FRPT), a fresh and refrigerated dog food maker selling through 30,235 retail stores, as a broken growth story, shares have fallen another 15.7% this past week as the company’s below-consensus EBITDA guidance overshadowed its first-ever positive free cash flow and a historic manufacturing technology upgrade, with the stock now at $58.93 against a Street mean target of $87.31.

Accordingly, Q4 FY2025 results, reported February 23, showed adjusted EBITDA of $61.2M beating the $57.78M estimate by 6%, yet FY2026 EBITDA guidance of $205M–$215M came in well below the $226.2M consensus, triggering the selloff even as Morgan Stanley upgraded the stock to “Overweight” on February 24, raising its price target to $90 from $71 on reduced competitive risk from General Mills’ Blue Buffalo Love Made Fresh.

Freshpet’s MVP households, its highest-spending buyers who average $506 annually and now represent 71% of net sales, grew 11% to 2.4M households in FY2025, outpacing overall household penetration growth of 10% and demonstrating that the core demand base remains intact despite the guidance miss that drove this week’s selloff.

The company’s first manufacturing line using breakthrough new production technology began shipping product to customers in January, and on the Q4 earnings call, William Cyr, Chief Executive Officer, stated that “the products produced in that new line are exceptional, and the early indications are that the new line should deliver significant quality, throughput and yield benefits,” directly supporting the 2027 adjusted gross margin target of at least 48%.

Freshpet enters its recovery phase with ~$400M in cash following the $95.5M January proceeds from the sale of its Ollie investment, fridge island tests expanding from 16 to 28 stores with an optional $20M–$50M CapEx acceleration available mid-year, and a 2027 adjusted EBITDA margin target of 20%–22% underpinned by OEE improvements, omnichannel build-out, and new technology deployment across additional production lines.

Wall Street’s Take on FRPT Stock

The EBITDA beat in Q4, where adjusted EBITDA of $61.2M topped the $57.78M estimate by 6%, confirms that Freshpet’s manufacturing efficiency gains are outpacing the revenue deceleration, making the 2027 margin target credible.

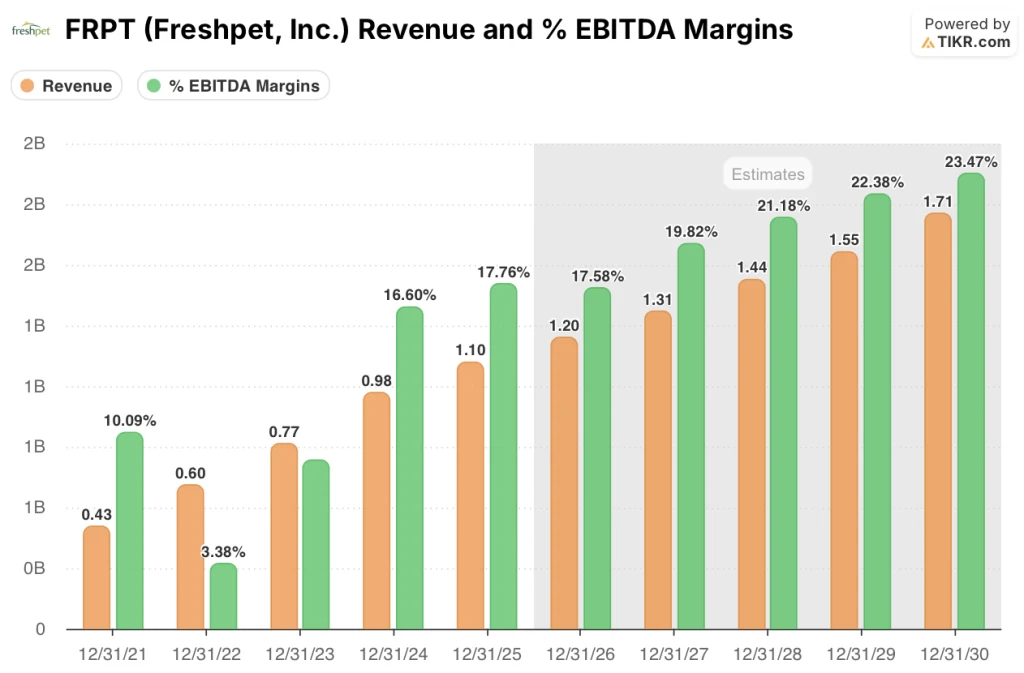

Revenue is forecast to grow from $1.10B in FY2025 to $1.31B by FY2027 at a 9.4% CAGR, while EBITDA margins expand from 17.8% to 19.8%, powered by OEE-driven volume absorption over a fixed cost base requiring no new staffing in FY2026.

Despite the 60% stock decline in 2025, 13 of 16 covering analysts rate FRPT a buy or outperform, with a mean price target of $87.31, implying 48.2% upside from $58.93, as the Street prices in the 2027 EBITDA margin recovery to 20%-plus.

The target range runs from $69 on the low end to $111 on the high end, where the bear case reflects continued macro-driven household penetration stagnation, and the bull case captures full fridge island rollout and accelerated new manufacturing technology deployment.

What Does the Valuation Model Say?

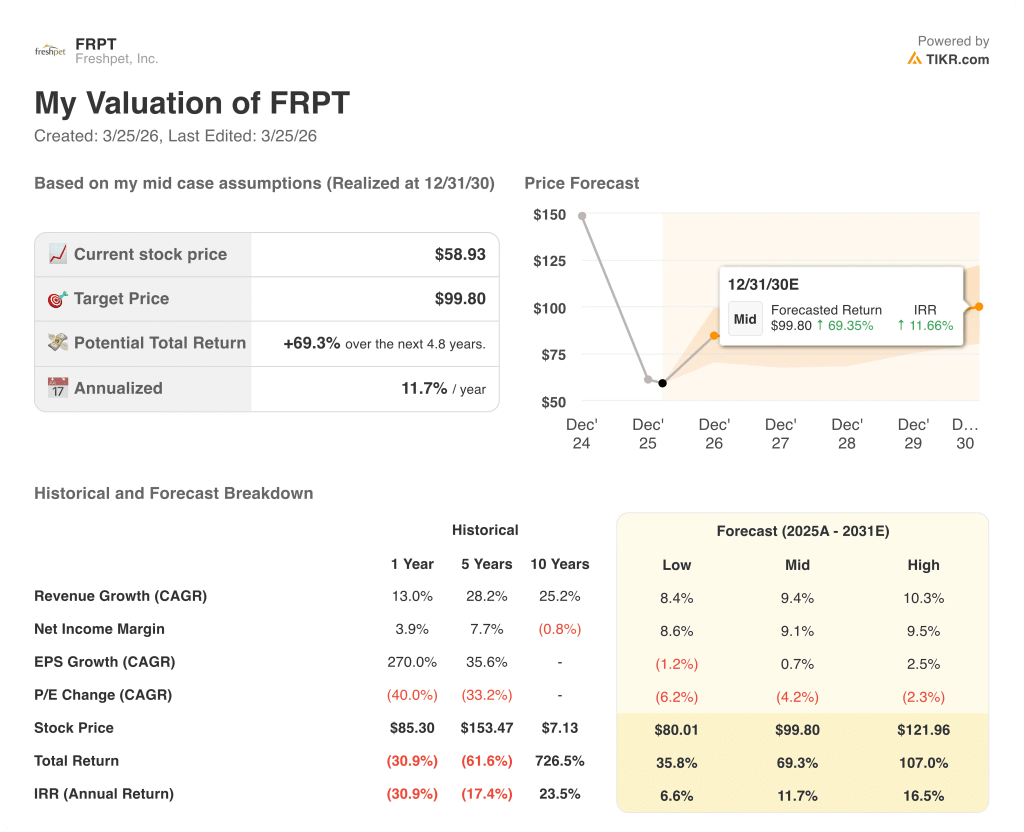

The TIKR mid-case targets $99.8 per share on a 9.4% revenue CAGR and EBITDA margin expansion to 23.5% by FY2030, a trajectory already validated by the first new-technology production line delivering product to customers in January and management’s 48%-plus gross margin target for 2027.

The market is treating FY2026’s normalized EPS drop to $1.36 as structural deterioration; it is a one-year incentive comp and investment reset, not a margin breakdown.

The TIKR model targets $99.8 anchored by the $95.5M Ollie sale proceeds boosting cash to ~$400M and three simultaneous growth levers entering their early commercial phases.

MVP households, Freshpet’s highest-spending buyers averaging $506 annually, grew 11% in FY2025 and now represent 71% of net sales, confirming the core demand base is intact despite macro noise.

Elevated beef input costs and a still-soft consumer sentiment index, if sustained through mid-2026, compress gross margin and prevent EBITDA from overcoming the incentive compensation reset, breaking the 2027 margin recovery path.

Thus, Q2 2026 results are the critical checkpoint: watch whether adjusted gross margin exceeds 48% and whether fridge island expansion triggers the optional $20M–$50M CapEx increase, confirming the inflection is tracking ahead of plan.

Should You Invest in Freshpet, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FRPT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Freshpet, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FRPT stock on TIKR for Free →