Key Stats for Norwegian Cruise Line Stock

- Past-Week Performance: +0.4%

- 52-Week Range: $14.2 to $27.2

- Current Price: $20.2

What Happened?

Norwegian Cruise Line Holdings (NCLH), a cruise operator running three brands across the mass and luxury segments, enters 2026 with activist investor Elliott Investment Management holding a 10%-plus stake and demanding a board overhaul after the company guided full-year adjusted earnings per share to $2.38, 7% below the $2.55 analyst consensus, while shares trade at $20.22, well below their 52-week high of $27.18.

On March 2, Norwegian reported Q4 revenue of $2.24 billion, missing the $2.35 billion IBES estimate by $103 million, while adjusted EPS of $0.28 beat the $0.26 estimate, as CFO Mark Kempa cited a 40% surge in Caribbean capacity deployed without aligned revenue management, sales, and marketing, creating pricing pressure that dragged full-year net yield guidance to flat.

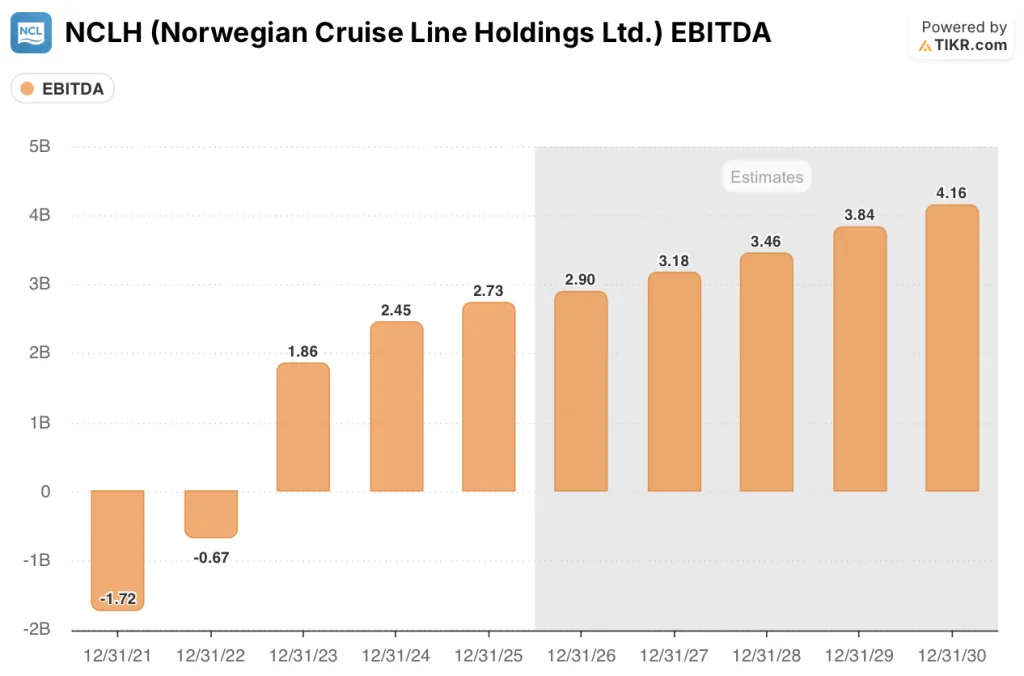

Adjusted EBITDA grew 11% to $2.73 billion in 2025 and is projected to reach $2.95 billion in 2026, underpinned by a third consecutive year of sub-inflationary unit cost growth at 0.9%, though the Norwegian brand, the largest of the three, bears the brunt of execution failures in the Caribbean, Bahamas, Philadelphia, and Alaska while the luxury Regent Seven Seas and Oceania brands posted January bookings up 20% year-over-year.

John Chidsey, President and CEO, stated on the Q4 2025 earnings call that “our strategy is sound, our execution and coordination have not been, and a culture of accountability is essential and necessary going forward,” a direct acknowledgment of the misaligned commercial apparatus behind the Caribbean capacity ramp that pushed Q1 2026 net yield growth to an expected decline of 1.6%.

Elliott’s board pressure, the Great Tides Waterpark opening at private island Great Stirrup Cay scheduled for summer 2026, a 51% fuel hedge cushioning a $100-per-barrel oil environment triggered by the U.S.-Iran conflict, and 17 ships on order through 2037 collectively define a turnaround story whose financial payoff, by management’s own admission, phases in through 2027 and beyond as net leverage holds near 5.2x.

Wall Street’s Take on NCLH Stock

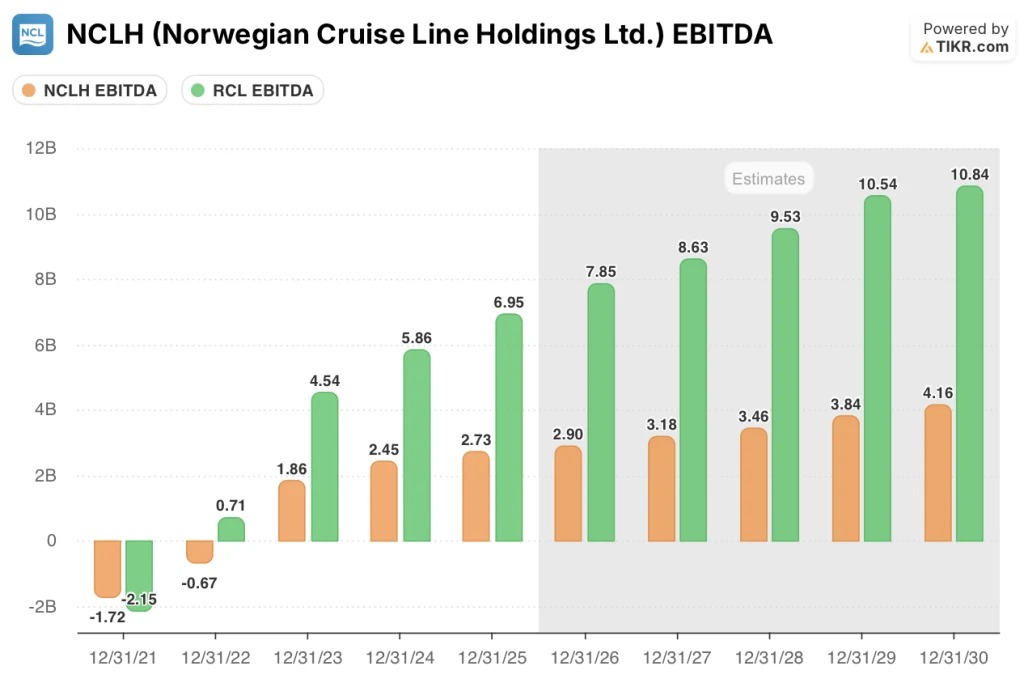

Elliott’s board pressure and Norwegian’s self-inflicted Caribbean capacity misfire have pulled NCLH’s EBITDA, a measure of operating profit before interest, taxes, and depreciation, to a 27.8% margin in 2025, creating the widest valuation gap versus peers in recent memory and setting the stage for a turnaround trade if new Chidsey’s execution fixes hold.

TIKR estimates projects EBITDA climbing from $2.73 billion in 2025 to $2.9 billion in 2026 and $3.18 billion in 2027, supported by three consecutive years of sub-inflationary unit cost growth already in evidence and a Great Stirrup Cay waterpark opening this summer that management expects to lift Caribbean yield into the fourth quarter.

Norwegian’s 27.8% EBITDA margin in 2025 sits 11.4% below Royal Caribbean’s 39.2%, a peer that just hit record profit guidance for 2026 on the back of disciplined revenue management and strong transatlantic demand, making the gap between the two operators the clearest argument for what Norwegian leaves on the table when execution falters.

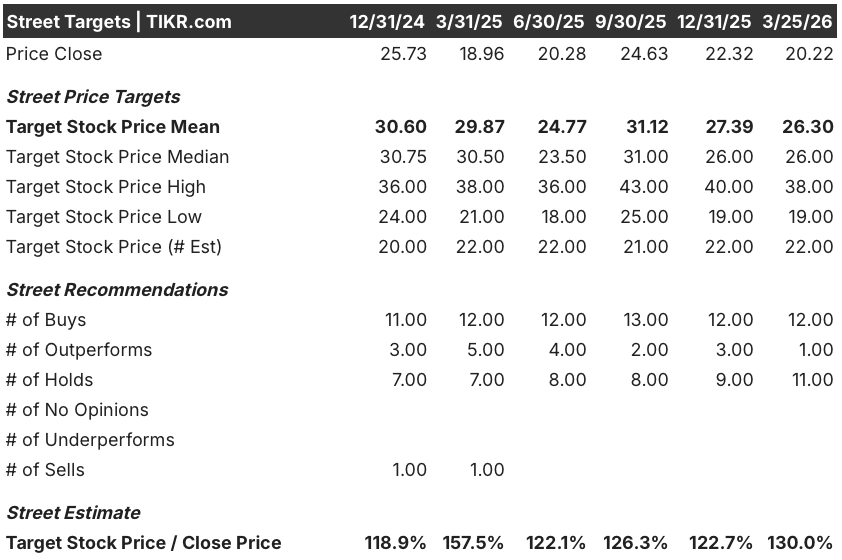

Analyst sentiment has shifted notably cautious: 12 buys, 1 outperform, and 11 holds among 22 analysts covering NCLH, with a mean price target of $26.3 implying 30% upside from $20.22, reflecting a street that believes the recovery is real but wants execution proof before upgrading.

The low target of $19 prices in a scenario where Middle East-driven oil above $100 per barrel overwhelms Norwegian’s 51% fuel hedge and Elliott’s board fight extends into a prolonged proxy war, while the high target of $38 assumes Chidsey closes the EBITDA margin gap and Great Stirrup Cay drives the Caribbean yield recovery management has promised for Q4.

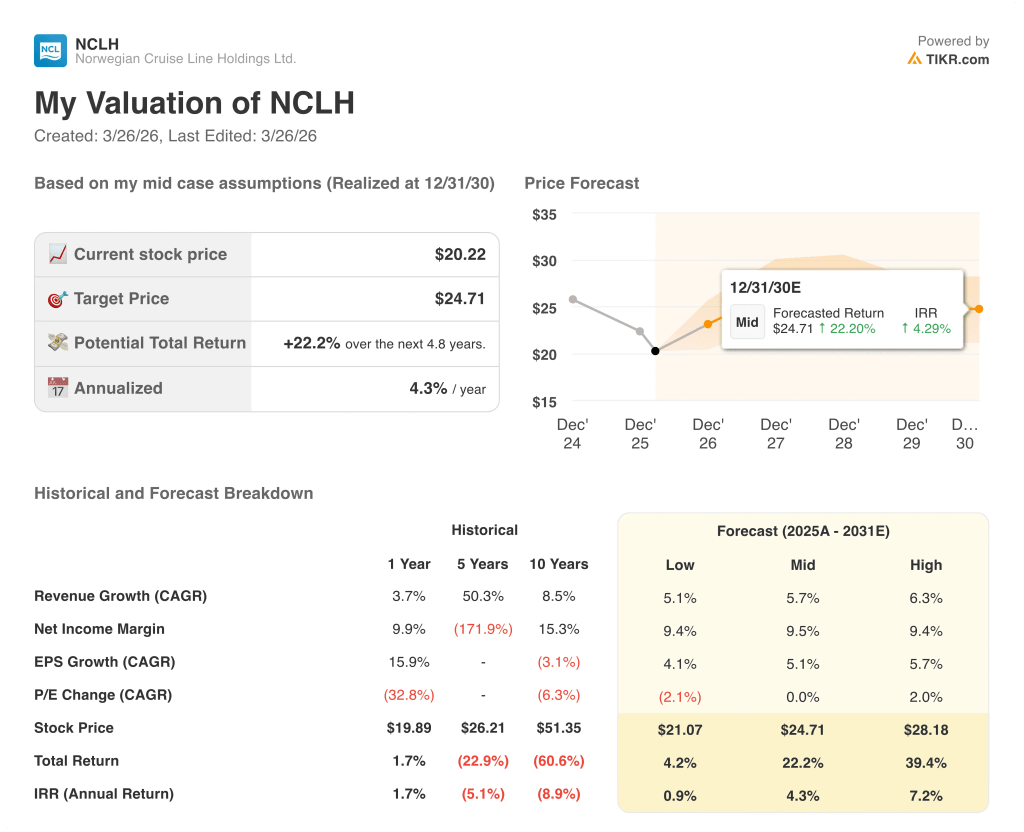

What Does the Valuation Model Say?

The TIKR mid-case model prices NCLH at $24.71 by December 2030, assuming a 5.7% revenue CAGR and net income margins recovering to 9.5%, both grounded in the cost discipline already delivered and the yield inflection expected as new revenue management systems, installed six to eight weeks before the earnings call, begin directing commercial strategy across all three brands.

The market is pricing NCLH as a broken operator; the EBITDA trajectory from $2.73 billion in 2025 to $3.18 billion in 2027 says otherwise.

Luxury brands Regent Seven Seas and Oceania, which posted January bookings up 20% year-over-year, confirm the asset base is not impaired; only the Norwegian mass brand is underperforming, and Chidsey has already replaced leadership across revenue management, marketing, and brand operations.

Chidsey’s explicit acknowledgment on the Q4 earnings call that the company “underinvested in technology, revenue management capabilities and customer-facing systems” is a management signal that the problem is diagnosed and capital is now directed at the right gap, not a deflection.

A sustained Brent crude move above $100 per barrel that exhausts Norwegian’s 51% 2026 fuel hedge breaks the $2.95 billion EBITDA guidance and forces another downward revision, compounding the credibility damage already inflicted by the Q4 revenue miss.

Q2 2026 earnings will be the first test of whether Chidsey’s commercial realignment is moving bookings off the bottom; watch net yield guidance revision and any update to the Great Stirrup Cay waterpark opening timeline.

Should You Invest in Norwegian Cruise Line Holdings Ltd.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NCLH stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norwegian Cruise Line Holdings Ltd. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NCLH stock on TIKR for Free →