Key Takeaways:

- American Airlines operates with ~$54.6 billion in revenue but faces margin pressure and high debt levels, impacting valuation.

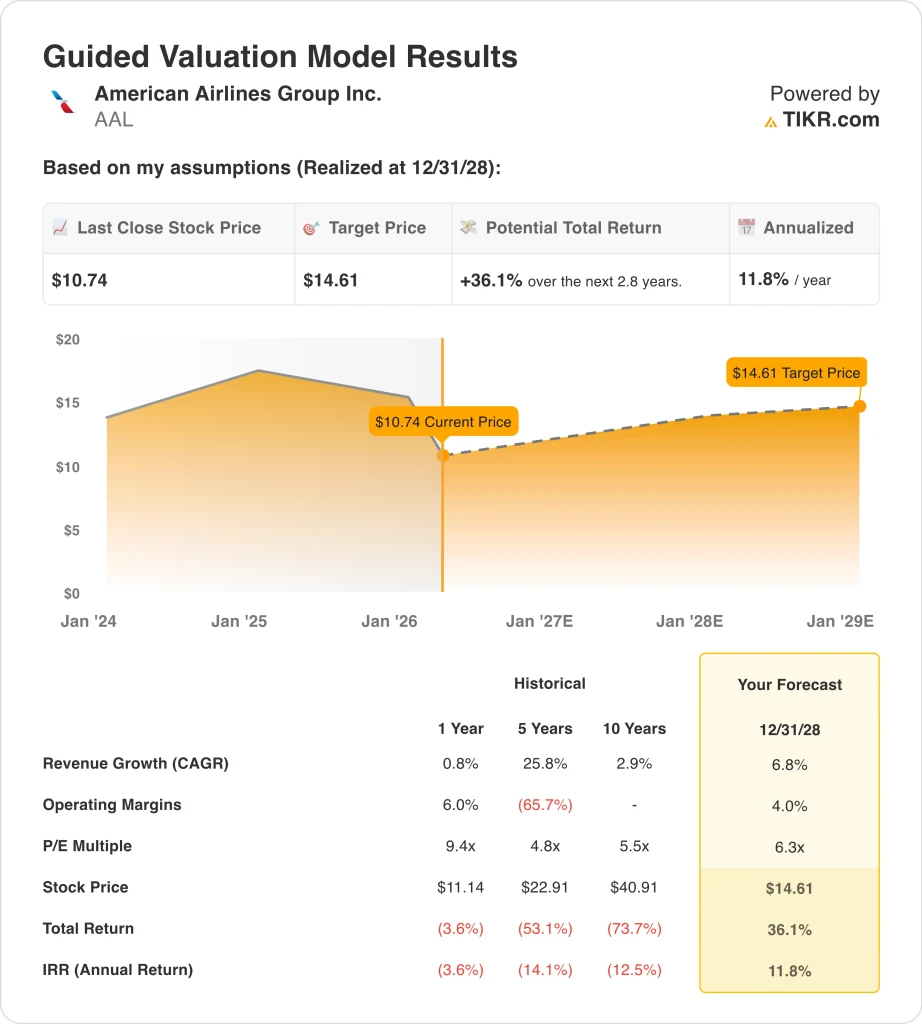

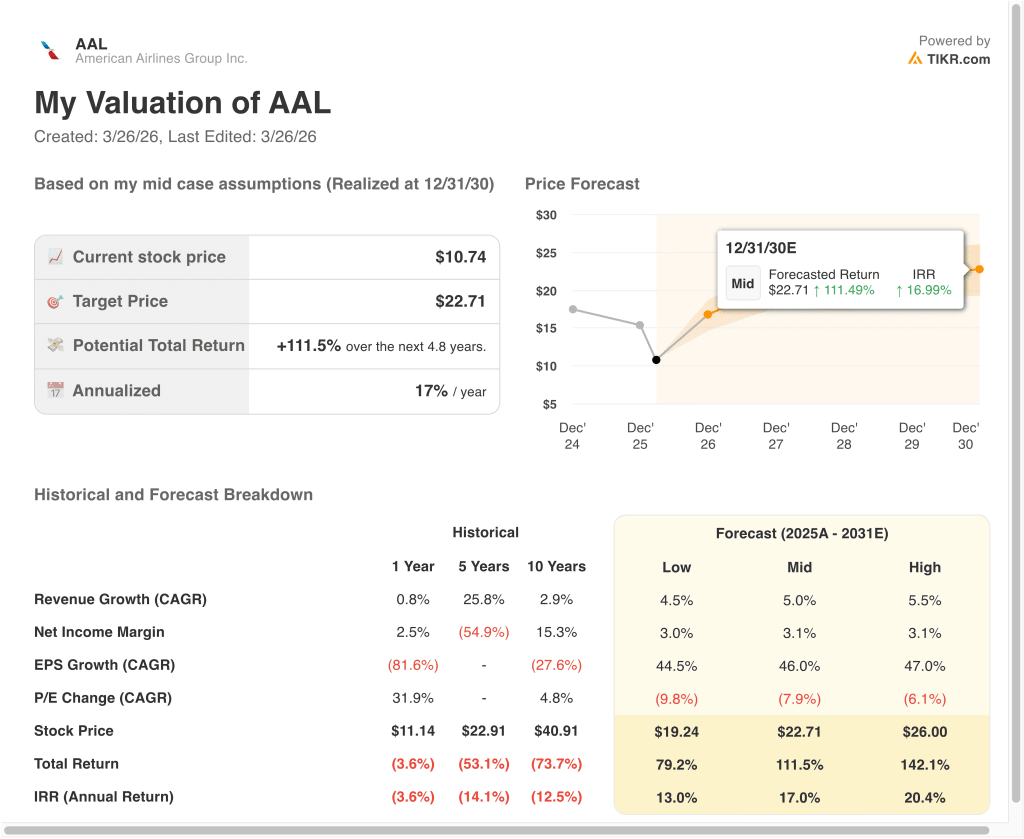

- AAL stock could reasonably reach $23 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 111.5% from today’s price of $11, with an annualized return of 17% over the next 4.8 years.

What Happened?

American Airlines Group Inc. (AAL) is navigating a complex recovery phase where demand remains strong, but profitability remains volatile. The company operates one of the largest global airline networks, yet faces structural challenges from fuel costs, labor, and leverage.

The airline industry has seen strong passenger demand post-pandemic, but margins have compressed due to rising jet fuel prices and operational disruptions. This creates a disconnect between stable revenue growth and weaker earnings power.

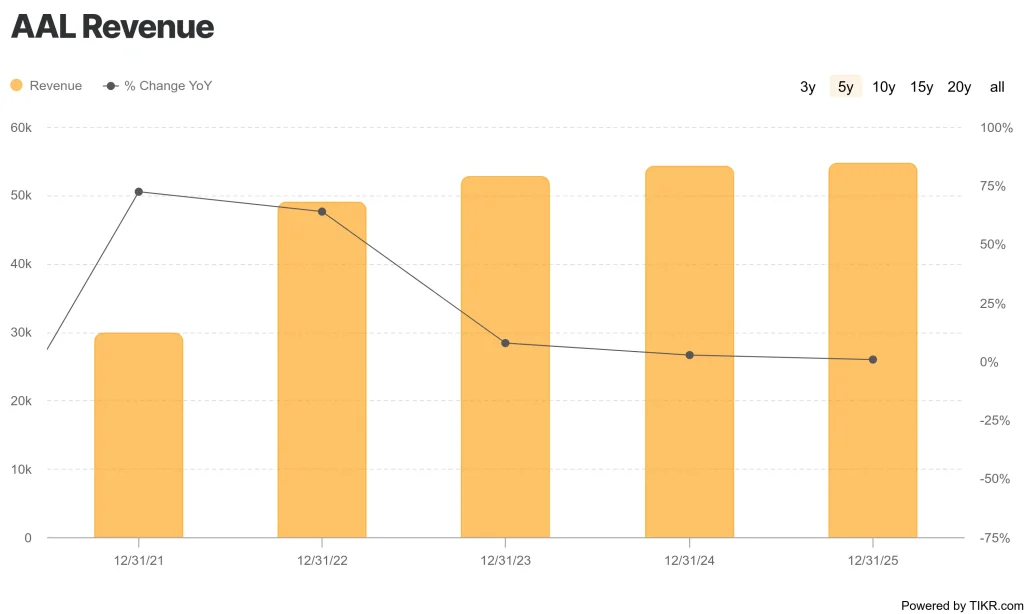

American Airlines generated $54.6 billion in total revenue over the last twelve months, but operating margins remain thin at just 3.1%. This reflects cost pressures and limits the company’s ability to convert demand into profits.

Recent Reuters coverage highlights that airlines are facing higher jet fuel costs, which directly compress margins. At the same time, competitors like Delta and United have adjusted capacity and pricing expectations, influencing sector-wide valuation.

Operational challenges have also played a role. Events like winter storms, airport disruptions, and safety-related headlines have impacted flight schedules and investor confidence, even if these issues are temporary.

Here’s why American Airlines stock could deliver meaningful long-term returns if margins stabilize and leverage declines over time.

What the Model Says for AAL Stock

We analyzed the upside potential for American Airlines stock using valuation assumptions based on moderate revenue growth, gradual margin recovery, and stable valuation multiples.

Based on estimates of 5.0% annual revenue growth, 3.1% operating margins, and a normalized P/E multiple of 6.3x, the model projects American Airlines stock could rise from $11 to $23 per share.

That represents a 111.5% total return over the next 4.8 years, or approximately 17% annualized returns.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for AAL stock:

1. Revenue Growth: 5%

American Airlines has grown revenue from $29.9 billion in 2021 to $54.6 billion LTM, driven by post-pandemic recovery. However, growth has slowed to just 0.8% year-over-year in 2025.

This reflects a more mature demand environment where capacity and pricing are stabilizing. While travel demand remains resilient, growth is no longer accelerating at prior rates.

Based on analysts’ consensus estimates, we assume 5.0% growth, which aligns with long-term industry trends and reflects steady demand without aggressive expansion.

2. Operating Margins: 3.1%

Operating margins have declined from 7.6% in 2023 to 3.1% in the latest period. This reflects rising costs across fuel, labor, and operations.

Airlines operate with structurally thin margins, and American Airlines is particularly sensitive due to its cost structure. Gross margins have also declined to 22.7%, reinforcing this pressure.

Based on analysts’ consensus estimates, we maintain a 3.1% margin assumption, reflecting stabilization rather than significant improvement.

3. Exit P/E Multiple: 6.3x

American Airlines currently trades at a low forward earnings multiple, reflecting cyclical risk and high leverage. The company also carries approximately $30.4 billion in net debt.

Low valuation multiples are typical for airlines due to volatility and capital intensity. However, they can expand if profitability stabilizes.

Based on analysts’ consensus estimates, we use a 6.3x multiple, consistent with current levels and reflecting a cautious valuation framework.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for American Airlines stock through 2030 show varied outcomes depending on cost pressures and margin recovery (these are estimates, not guaranteed returns):

- Low Case: Fuel costs remain elevated, and margins compress further → 13.0% annual returns

- Mid Case: Stable demand and modest margin recovery → 17.0% annual returns

- High Case: Strong pricing power and cost normalization → 20.4% annual returns

Even in the conservative case, the model suggests positive returns, supported by stable demand and gradual financial improvement. The key driver across all scenarios is margin expansion. Revenue growth is relatively predictable, but profitability determines valuation outcomes.

American Airlines remains a highly cyclical investment tied to macro conditions, fuel prices, and operational execution. Investors are effectively betting on whether margins can recover toward historical levels.

Looking ahead, investors are focused on the upcoming Q1 2026 earnings report on April 22, 2026. This will provide clarity on whether cost pressures are stabilizing or continuing to weigh on earnings.

See what analysts think about AAL stock right now (Free with TIKR) >>>

Should You Invest in American Airlines Group Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AAL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AAL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze American Airlines stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!