Key Stats for Mattel Stock

- Past-Week Performance: -7.7%

- 52-Week Range: $14 to $22.5

- Current Price: $15

What Happened?

Hot Wheels, Mattel‘s die-cast vehicle line that generated $1.75 billion in gross billings in 2025, just notched its eighth consecutive record year even as the broader company missed fourth-quarter estimates by $78 million and watched its stock collapse 25% to $15.90 on February 11.

Mattel’s Q4 2025 earnings call on February 10 revealed net sales of $1.77 billion against an IBES estimate of $1.844 billion, with adjusted gross margin contracting 480 basis points to 46% as the company leaned into promotions to clear December inventory after U.S. retailer orders decelerated sharply late in the holiday season.

Hot Wheels’ double-digit gross billings growth anchored a Vehicles category that expanded 11% for the full year to $1.99 billion, while challenger categories combining Action Figures, Building Sets, and Games collectively grew 13%, suggesting the company’s non-Barbie portfolio is carrying material weight that rival Hasbro’s more entertainment-dependent lineup has struggled to match consistently.

CEO Ynon Kreiz stated on the Q4 2025 earnings call that “2026 will be an important year for Mattel as we implement our new brand-centric strategy to grow our IP-driven play and family entertainment business,” tying directly to the February 10 announcement of full acquisition of Mattel163, a mobile games studio with over 550 million downloads and more than $200 million in annual revenue, now wholly owned after Mattel paid $159 million for NetEase’s 50% stake.

Mattel’s $1.5 billion share repurchase program, a $150 million strategic investment targeting digital games and first-party data capabilities, the June 5 Masters of the Universe theatrical release, and a Paramount licensing deal covering Teenage Mutant Ninja Turtles starting 2027 collectively position the company to pursue management’s guided double-digit adjusted operating income growth in 2027 after a deliberate investment year in 2026.

Wall Street’s Take on MAT Stock

Mattel’s February 10 earnings miss and the $150 million investment drag it disclosed for 2026 have compressed the stock to $14.95, a level that treats a deliberately guided, one-year earnings trough as permanent impairment rather than a funded transition.

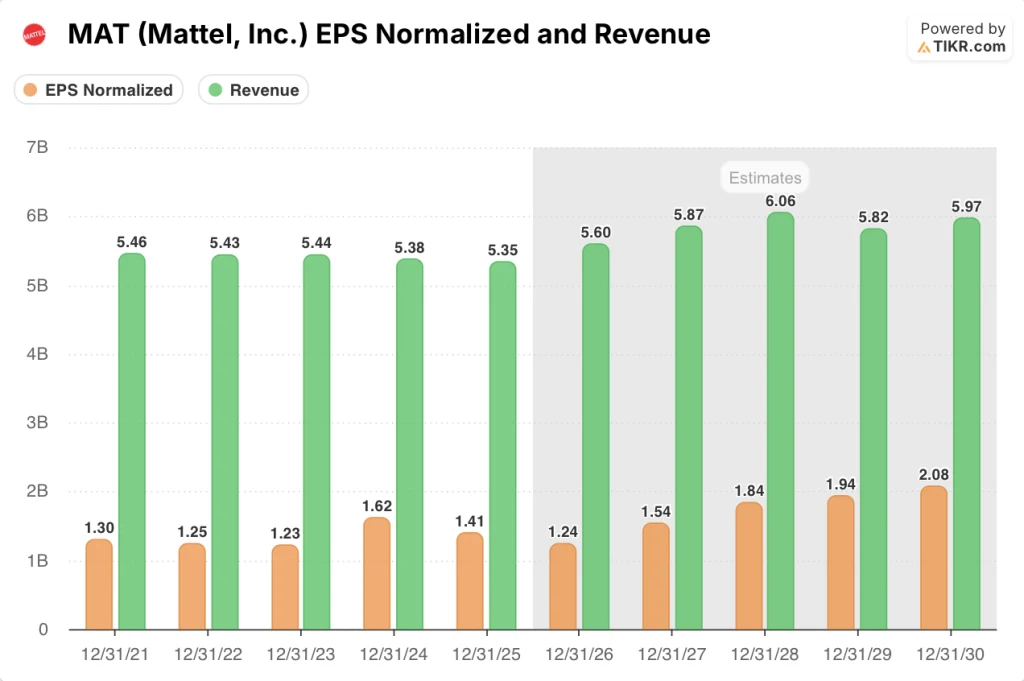

TIKR’s forward estimates shows normalized EPS recovering 23.6% to $1.54 in 2027 after falling to $1.24 in 2026, a rebound driven specifically by Mattel163’s full-year revenue consolidation, self-published mobile game monetization, and the $150 million investment burden rolling off the P&L entirely.

Meanwhile, revenue is estimated to grow 4.7% to $5.60 billion in 2026 and 4.8% to $5.87 billion in 2027, supported by Hot Wheels’ guided double-digit growth, the Teenage Mutant Ninja Turtles product launch, and the Masters of the Universe theatrical release on June 5 — all confirmed, dated catalysts.

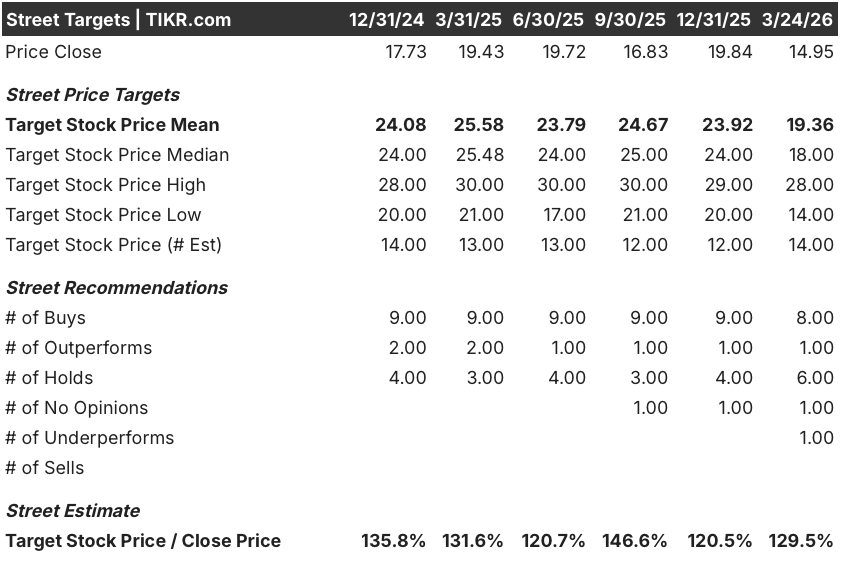

Eight analysts rate MAT a buy, one an outperform, six a hold, and one an underperform, with a mean price target of $19.36 implying 29.5% upside from the current $14.95, as the Street awaits confirmation that the 2026 investment spend converts into 2027 profitability rather than a recurring cost base.

The analyst target range spans $14 to $28, with the low end reflecting sustained margin pressure if December 2025’s U.S. consumer weakness persists into 2026, and the high end pricing in full execution of the mobile gaming strategy and Barbie’s guided return to growth in 2027.

What Does the Valuation Model Say?

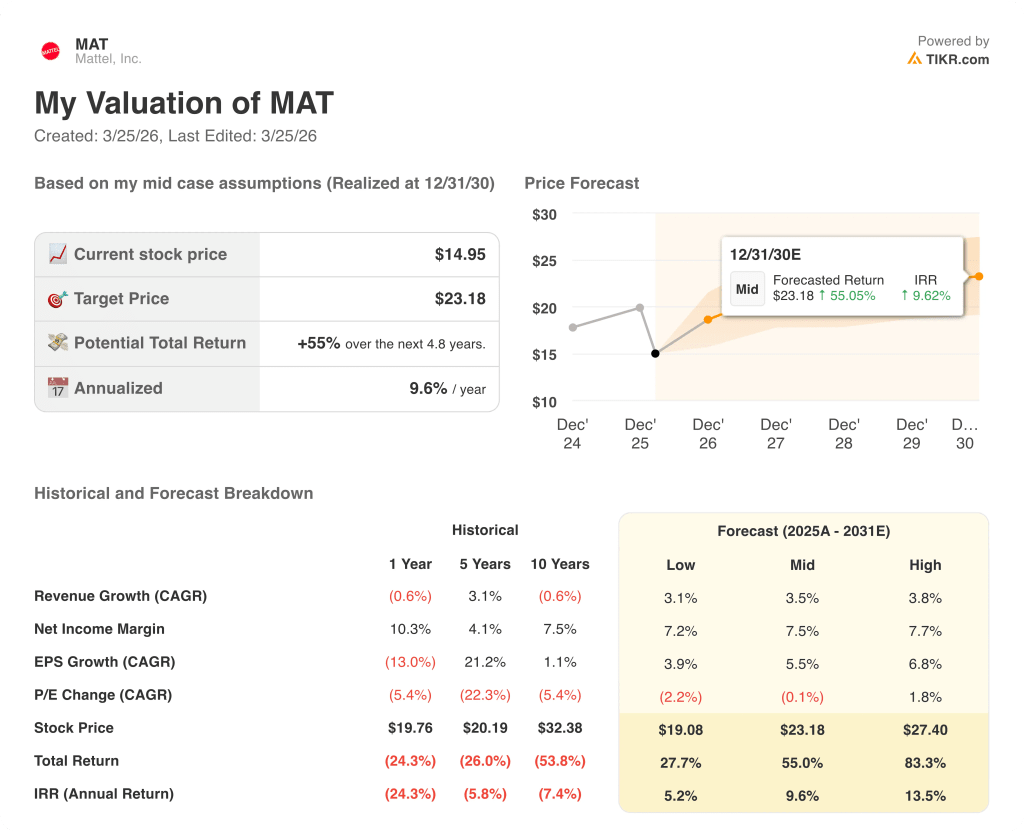

The TIKR mid-case target of $23.18 implies a 55% total return by December 2030 at a 9.6% annual IRR, anchored by a 3.5% revenue CAGR and a net income margin recovering to 7.5% as high-margin digital games and licensing revenue replace the dilutive inventory clearance activity that crushed Q4 adjusted gross margin to 46%.

The market is pricing MAT as a structurally impaired toy manufacturer, ignoring that Mattel163 alone generates over $200 million in annual revenue at high margin, now fully consolidated.

The TIKR $23.18 target is justified by the 2027 EPS recovery to $1.54, itself underwritten by the Mattel163 full-year contribution, mobile game self-publishing ROI, and $50 million in additional cost savings under the Optimizing for Profitable Growth program.

CEO Ynon Kreiz’s open-market share purchase on February 12, filed via Form 4 with the SEC, confirms management conviction precisely when the stock was trading near its 52-week low of $13.95.

If U.S. retailer inventory conservatism deepens through mid-2026, the $5.60 billion revenue estimate and the 2027 EPS recovery both slip, and the TIKR target price compresses toward the $19.08 low-case scenario.

The Masters of the Universe theatrical release on June 5 is the single nearest-term test: strong toy sell-through tied to that launch would validate the entertainment-to-toy flywheel and confirm the 2027 growth acceleration is on track.

Should You Invest in Mattel, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MAT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Mattel, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MAT stock on TIKR for Free →