Key Stats for MPC Stock

- This-Week Performance: 5%

- 52-Week Range: $115 to $247

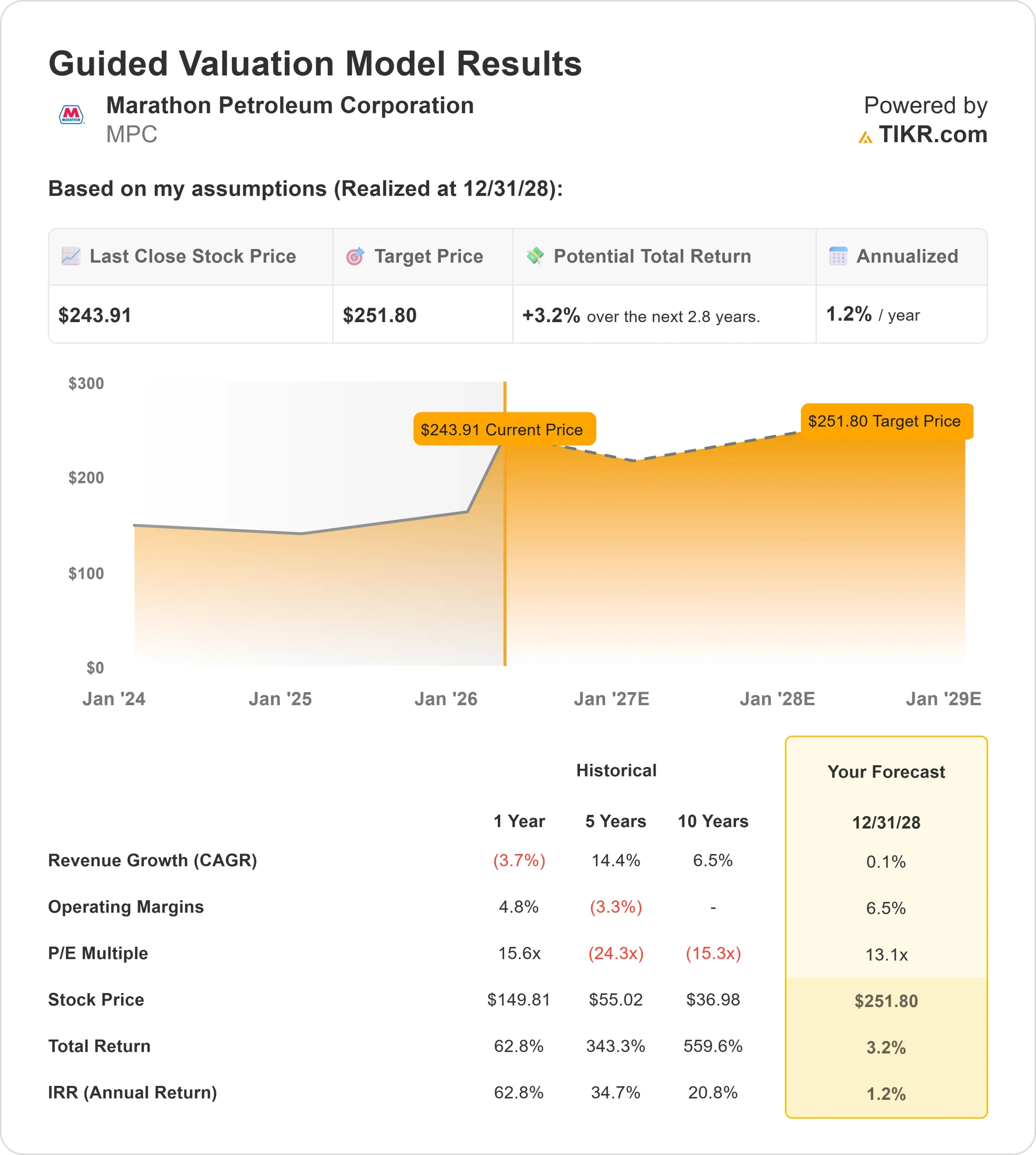

- Valuation Model Target Price: $252

- Implied Upside: 3%

Analyze your favorite stocks like Marathon Petroleum Corporation with TIKR (It’s free) >>>

What Happened?

Marathon Petroleum stock rose about 5% this week, finishing near $244 per share as refining stocks moved higher on stable fuel demand expectations and resilient refining margins.

The move came as investors rotated back into energy names, with peers like Valero Energy and Phillips 66 also gaining during the week, as investors broadly re-rated U.S. refiners benefiting from strong crack spreads and steady demand.

The stock moved higher this week primarily because investors are pricing in resilient refining margins and steady cash flow generation ahead of the next earnings cycle.

Marathon Petroleum benefits from the spread between crude oil and refined product prices, and recent data suggests those spreads have remained firm, supporting earnings visibility even as crude prices fluctuate, which is important since small changes in margins can have an outsized impact on profitability for refiners.

Recently, Marathon Petroleum highlighted strong operational performance in its 2025 annual report, reporting 94% refining utilization and 105% margin capture, while outlining expansion projects including increasing crude throughput at its Garyville refinery by 30,000 barrels per day and adding 10,000 barrels per day of premium gasoline capacity by 2027.

Management said it is “advancing planned investments at the Garyville refinery,” reinforcing its focus on capacity growth and margin optimization, while a specialty gasoline project at its El Paso refinery is expected in Q2 2026.

These projects matter because incremental throughput and higher-value product mix can directly support margins and long-term earnings power.

At the same time, Chief Commercial Officer Ricky Hessling sold about 1,626 shares at $228 per share, a relatively small transaction that did not materially impact sentiment.

Recent institutional filings showed mixed positioning across funds, with overall ownership remaining high at about 76.8%.

Sagespring Wealth Partners increased its stake by 37.7% to about 31,245 shares, Bank of Nova Scotia raised its position by 81.8% to about 170,589 shares, and Aquatic Capital Management boosted its holdings by 618.3% to about 26,514 shares, while Allworth Financial trimmed its stake by 21.4% to about 16,966 shares and L2 Asset Management reduced its position by 46.9% to about 16,808 shares.

Analyst sentiment remains generally constructive, with firms continuing to highlight strong free cash flow generation and disciplined capital returns, even as price targets have seen limited changes recently.

Compared to peers like Valero Energy and Phillips 66, Marathon Petroleum benefits from its large refining footprint and integrated logistics network, which supports more consistent margin capture across cycles.

The combination of steady institutional ownership, supportive fundamentals, and improving refining economics helped support shares this week.

Value Marathon Petroleum Corporation instantly (Free with TIKR) >>>

Is MPC Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 0.1%

- Operating Margins: 6.5%

- Exit P/E Multiple: 13.1x

Marathon Petroleum’s revenue profile has normalized after peaking near $180 billion in 2022, with recent years stabilizing closer to the $125 to $135 billion range.

This reflects a more balanced fuel pricing environment rather than structural growth, which is typical for refining businesses.

See analysts’ growth forecasts and price targets for Marathon Petroleum Corporation (It’s free) >>>

This matters because Marathon Petroleum is not driven by consistent top-line expansion. Instead, returns are tied to refining margins, cost control, and capital allocation.

Compared to peers like Valero Energy and Phillips 66, the company benefits from its scale and integrated refining and logistics network, which supports more consistent cash flow generation across cycles.

Based on these inputs, the model estimates a target price of $252, implying about 3.2% total upside over the next 3 years, suggesting the stock may already reflect much of its near-term earnings strength.

Earnings over the next year will depend primarily on refining margins, which remain the key profit driver. If spreads stay strong, the company can sustain high levels of free cash flow, while continued share repurchases can support earnings per share growth even if overall profits remain stable.

Demand trends will also matter. Stable gasoline and diesel consumption supports high refinery utilization, which helps margins. If demand weakens, profitability could come under pressure.

At current levels, Marathon Petroleum looks like a steady cash flow business rather than a high-growth opportunity, with future performance driven by margin stability, capital returns, and disciplined execution rather than rapid expansion.

How Much Upside Does MPC Stock Have From Here?

Investors can estimate Marathon Petroleum Corporation potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Marathon Petroleum Corporation in under 60 seconds with TIKR (It’s free) >>>