Key Takeaways:

- Visa continues to compound high-margin revenue through payment volume growth, cross-border spending, and value-added services.

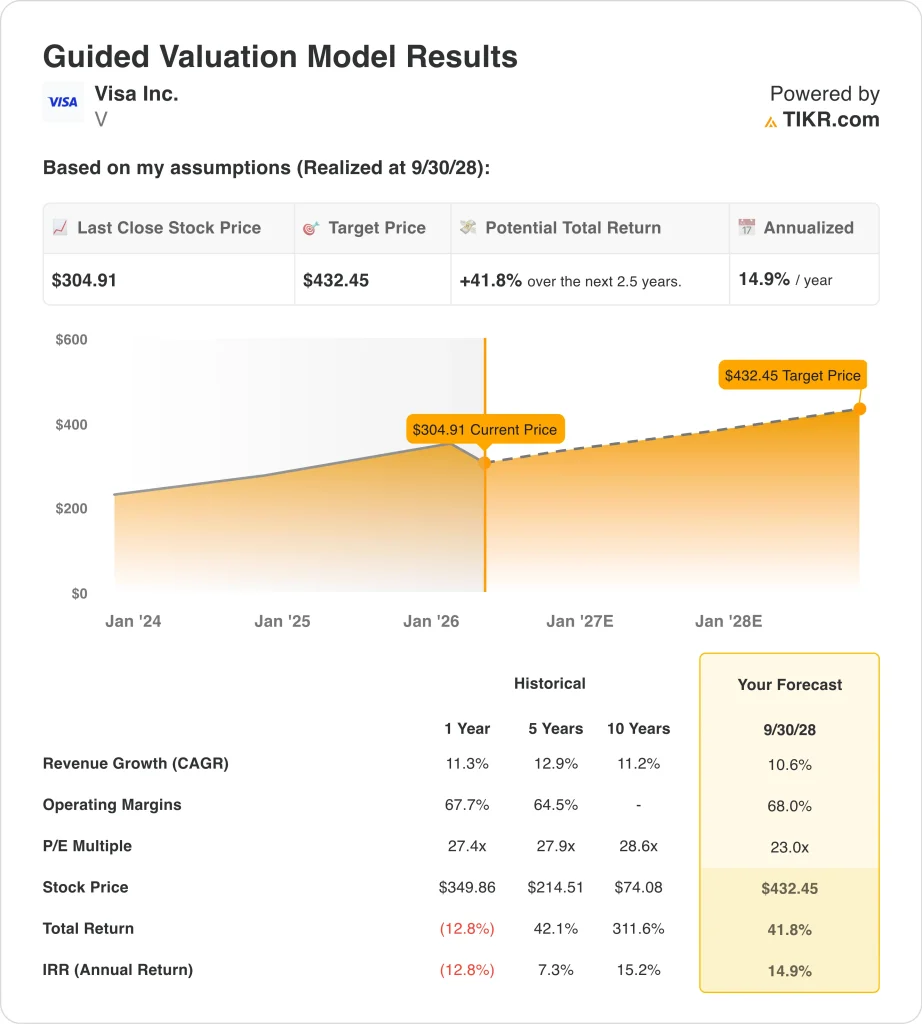

- Visa stock could reasonably reach $432 per share by September 2028, based on our valuation assumptions.

- This implies a total return of 41.8% from today’s price of $305, with an annualized return of 14.9% over the next 2.5 years.

What Happened?

Visa is still one of the strongest businesses in large-cap financial services, but the stock has pulled back in 2026. The shares were down 11.8% over the recent period, even though the business still posts industry-leading margins. That disconnect matters because Visa’s operating performance remains far steadier than the stock’s short-term moves suggest.

Visa has become relevant again this week because the market is weighing two very different stories at once. On one hand, the company keeps reporting resilient spending trends, expanding crypto and stablecoin initiatives, and deepening its role in global money movement. On the other hand, investors are also processing regulatory headlines, new fintech competition, and a broader reset in payments valuations after the stock’s 2026 pullback.

The most important recent operating update was the January earnings release. CEO Ryan McInerney said Visa delivered “a very strong fiscal first quarter” with revenue up 15% and non-GAAP EPS up 15%, driven by resilient consumer spending, a strong holiday season, and continued strength in value-added services, commercial products, and money movement solutions. That matters because it shows the business itself did not weaken in the way the stock price recently did.

Visa expanded its work with Bridge on March 3, saying stablecoin-linked Visa cards are already live in 18 countries and planned to expand to over 100 countries by year-end, while Reuters also reported that Visa’s stablecoin settlement activity had reached a $4.5 billion annualized run rate in January. For a smart generalist, stablecoins are digital tokens designed to hold a stable value, and Visa is trying to make sure those assets still move through trusted payment infrastructure rather than around it.

There is also a legal angle investors cannot ignore. Reuters reported on March 17 that Visa and Mastercard won the right to appeal a UK ruling that said certain merchant fees breached competition law. That headline did not change Visa’s day-to-day network economics overnight, but it did remind investors that even elite payments franchises can face headline risk from regulation and litigation.

Here’s why Visa stock could still provide solid returns through 2028 and beyond.

What the Model Says for Visa Stock

We analyzed the upside potential for Visa stock using valuation assumptions based on its durable network effects, steady double-digit revenue growth, and unusually high margins.

Based on estimates of 10.6% annual revenue growth, 68.0% operating margins, and a normalized P/E multiple of 23.0x, the model projects Visa stock could rise from $305 to $432 per share.

That would be a 41.8% total return, or a 14.9% annualized return over the next 2.5 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Visa stock:

1. Revenue Growth: 10.6%

Visa has grown revenue from $24.1 billion in fiscal 2021 to $40.0 billion in fiscal 2025, with LTM revenue at $41.4 billion. In fiscal Q1 2026, revenue rose 15%, supported by strong payment volume, cross-border activity, and value-added services.

That growth rate also looks grounded against the company’s history. Your guided model shows 11.3% one-year revenue growth and 12.9% five-year CAGR. Based on analysts’ consensus estimates, we used a 10.6% forecast, which reflects continued growth without assuming acceleration.

2. Operating Margins: 68%

Visa is one of the highest-margin businesses in large-cap finance. Recent data shows an LTM EBIT margin of 67.0%, and the income statement shows operating margins have stayed in the high-60s for years. That consistency is one reason Visa keeps earning a premium valuation.

The assumption also matches how the business scales. Gross margins are 97.8%, and much of Visa’s incremental revenue drops through at high profitability. Based on analysts’ consensus estimates, we use 68.0% operating margins, which is close to where the business already operates.

3. Exit P/E Multiple: 23x

Visa has an LTM P/E of 28.6x and an NTM P/E of 23.1x. The model uses a 23.0x exit multiple, so it does not rely on multiple expansion. Instead, most of the modeled return comes from business growth.

That assumption also looks reasonable against Visa’s balance sheet and cash generation. LTM net debt is just $4.8 billion, net debt to EBITDA is 0.16x, and LTM free cash flow is $22.9 billion. Those numbers support a premium multiple, but the model still stays close to today’s forward earnings framework.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

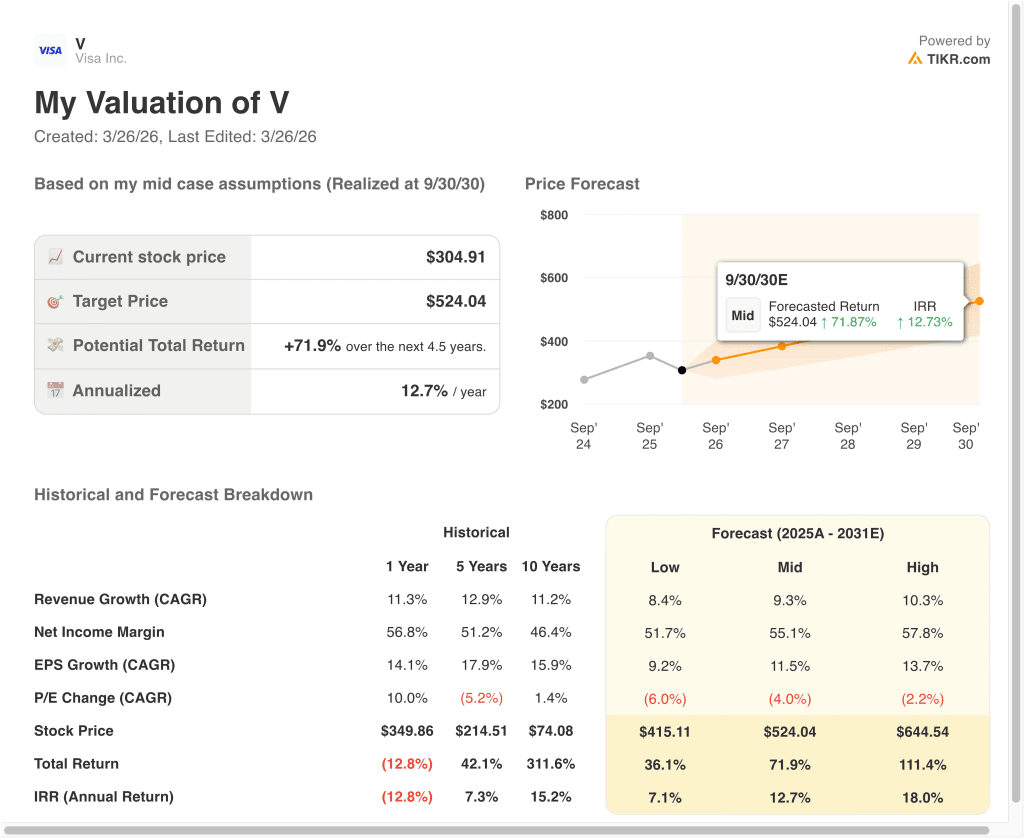

Different scenarios for Visa stock through 2030 show varied outcomes based on execution, spending trends, and valuation compression or expansion (these are estimates, not guaranteed returns):

- Low Case: Revenue growth slows and the valuation multiple compresses further → 7.1% annual returns

- Mid Case: Visa keeps compounding across consumer payments, cross-border, and value-added services → 12.7% annual returns

- High Case: Growth stays strong, margins remain elite, and the market rewards the network with a higher ending value → 18.0% annual returns

The low case still shows how durable the business is. In that scenario, the advanced model points to a $415.11 share price by September 2030 and a 36.1% total return. That is a lower outcome, but it is still supported by recurring network activity and strong free cash flow.

The mid case points to $524.04 per share, with a 71.9% total return and 12.7% annualized returns. That case assumes 9.3% revenue CAGR, 55.1% net income margins, and some valuation compression. In other words, the return still comes mostly from business growth.

The high case reaches $644.54 per share with 18.0% annualized returns. That would likely require stronger growth and a more favorable market backdrop for premium payments stocks. Even in the conservative case, Visa remains a business with exceptional margins, modest leverage, and durable global payment exposure.

See what analysts think about Visa stock right now (Free with TIKR) >>>

Should You Invest in Visa Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Visa, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Visa alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Visa stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!