Key Takeaways:

- Caterpillar is benefiting from strong demand in power generation, especially for data centers, but tariff costs and a richer valuation are limiting the model’s return outlook.

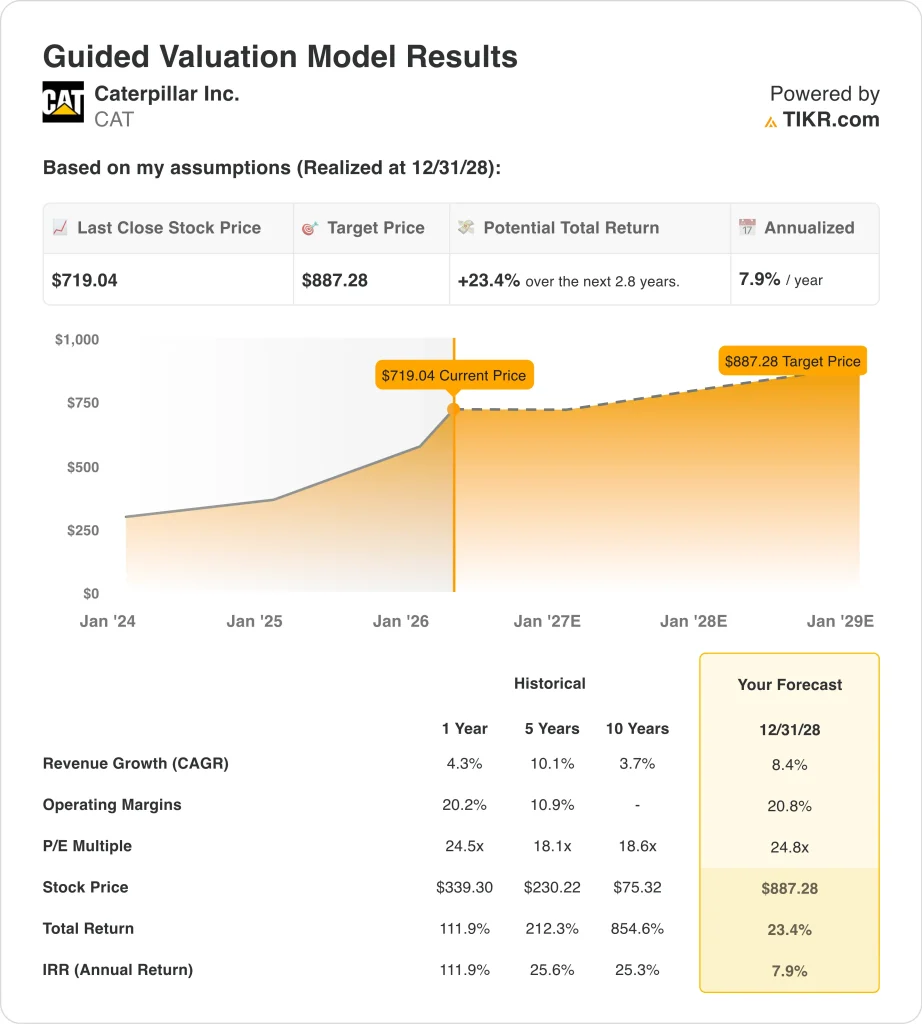

- CAT stock could reasonably reach $887 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 23.4% from today’s price of $719, with an annualized return of 7.9% over the next 2.8 years.

What Happened?

Caterpillar is still one of the market’s favorite industrial stocks because investors increasingly see it as more than a construction equipment maker. The company also sells engines, turbines, and distributed power systems, and that part of the business has become more important as data center power demand rises. In the fourth quarter, sales and revenues rose 18% to $19.1 billion, and the company ended the year with a record backlog of about $51 billion.

That backdrop helps explain why the stock is trading near $719 even after a powerful run over the past year. Investors are rewarding Caterpillar for stronger power demand, better visibility, and a business mix that now has more exposure to energy infrastructure. Reuters also reported on March 10 that Atlas Energy signed a deal with Caterpillar to secure about $840 million of power-generation equipment through 2029, which added another concrete signal that demand is broadening beyond the company’s traditional construction cycle.

The story gained another leg in mid-March when Nscale and Microsoft announced a West Virginia AI factory collaboration with NVIDIA and Caterpillar that is tied to up to 1.35 gigawatts of NVIDIA Vera Rubin NVL72 GPU capacity. For investors, that matters because it connects Caterpillar to a fast-growing buildout in on-site and backup power for large AI campuses. Caterpillar is showing up in the infrastructure layer that helps data centers operate when grid power is constrained or reliability is critical.

But investors are not only focused on growth. That is why the market is balancing enthusiasm over power demand with caution around tariffs, margins, and whether the stock already reflects much of that good news ahead of the company’s expected next earnings release on April 30.

What the Model Says for CAT Stock

We analyzed the upside potential for Caterpillar stock using valuation assumptions based on its expanding power exposure, still-healthy end markets, and a stock price that already reflects a lot of recent good news.

Based on estimates of 8.4% annual revenue growth, 20.8% operating margins, and a normalized P/E multiple of 24.8x, the model projects Caterpillar stock could rise from $719 to $887 per share by December 2028.

That would be a 23.4% total return, or a 7.9% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CAT stock:

1. Revenue Growth: 8.4%

Caterpillar grew total revenue 4.3% in 2025 to $67.6 billion, based on the financials you provided. The fourth quarter was much stronger, with sales and revenues rising 18% to $19.1 billion, helped by higher sales volume and dealer inventory changes. Management also said it entered the year with a record backlog and strong momentum.

The business drivers behind that assumption are visible across several lines. Power demand is clearly one of them, because fourth-quarter Energy & Transportation volume improved, and recent news flow included Atlas Energy’s $840 million equipment agreement through 2029. The Nscale and Microsoft announcement also supports the view that Caterpillar has growing exposure to power infrastructure tied to AI campuses.

Still, Caterpillar is not a pure growth stock. Construction, mining, and resource end markets remain cyclical, and the company’s top-line growth slowed sharply from 12.8% in 2023 to 4.3% in 2025. So the 8.4% assumption implies a stronger growth path than the latest annual result, supported by backlog and power demand but still dependent on execution.

2. Operating Margins: 20.8%

Caterpillar’s LTM EBIT margin is 17.4%, while its 2025 operating margin in the income statement was also 17.4%. That means the model’s 20.8% margin assumption implies a recovery toward earlier peak levels rather than a continuation of the latest run rate. It is achievable only if pricing, mix, and cost control improve from here.

There are reasons investors still give Caterpillar credit on margins. The business has scale, a large installed base, and a profitable parts and services ecosystem that can support earnings even when equipment cycles soften. It also generated $11.7 billion of operating cash flow and $7.5 billion of free cash flow in 2025, which shows the underlying earnings engine remains strong.

But there is also a clear reason not to get too aggressive. Fourth-quarter adjusted operating profit margin fell to 15.6% from 18.3% a year ago, despite strong revenue growth, which shows cost pressure is real. That is why a 20.8% margin assumption should be viewed as a normalized outcome over time, not a statement about what the next quarter will look like.

3. Exit P/E Multiple: 24.8x

Caterpillar’s overview data shows an LTM P/E of 38.23x and an NTM P/E of 31.46x, while the guided model uses a 24.8x exit multiple. The key point is that CAT is no longer trading like a cheap cyclical industrial. Investors are already paying a premium for quality, backlog, cash returns, and a power business that appears to have better visibility than the market used to assign.

That assumption is easier to justify now than it would have been several years ago. The Street mean target rose to $736 by March 25, 2026, and buy plus outperform ratings outnumber sells. The stock’s strong one-year run also shows the market is willing to reward Caterpillar with a richer multiple when demand visibility improves.

Even so, valuation is the main debate now. A premium multiple can hold if backlog stays firm and power demand remains strong, but it can also compress if margins disappoint or cyclical end markets cool. That is why the stock can still look like a strong business while offering a more modest expected return from today’s price.

Build your own Valuation Model to value any stock (It’s free!) >>>

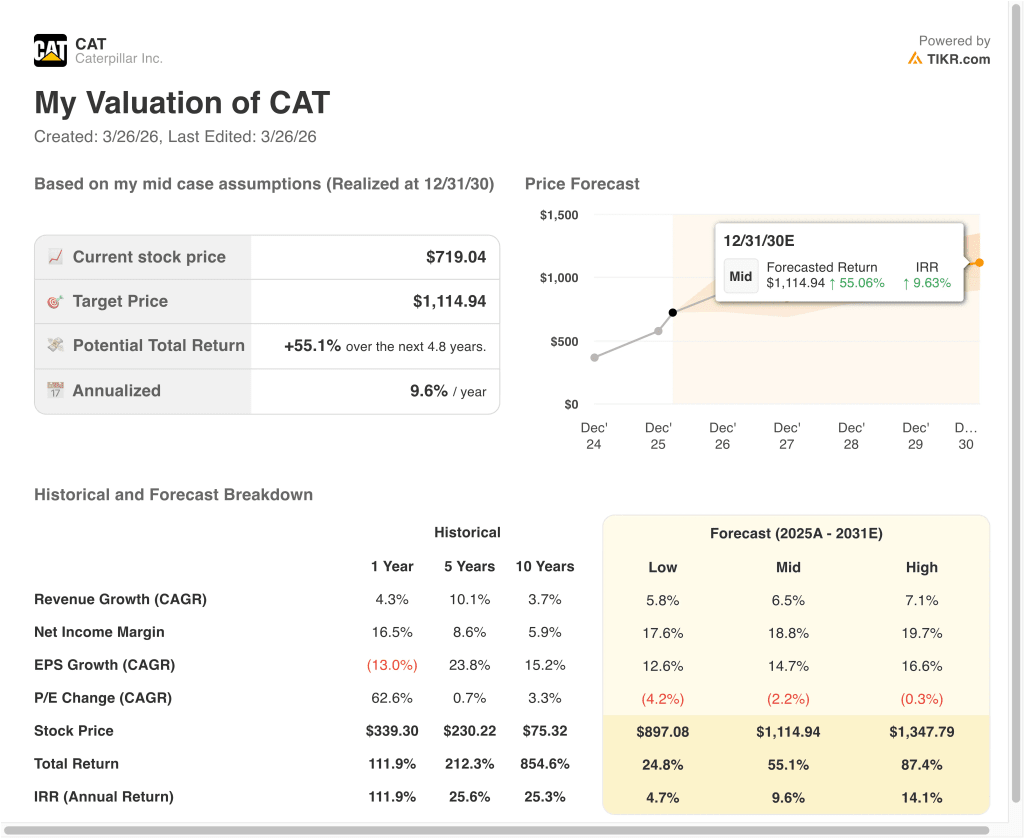

What Happens If Things Go Better or Worse?

Different scenarios for CAT stock through 2030 show varied outcomes based on power demand, margin durability, and valuation levels (these are estimates, not guaranteed returns):

- Low Case: Data-center and equipment demand cools, and margins face more pressure → 4.7% annual returns

- Mid Case: Power demand stays firm, and Caterpillar executes against backlog while margins normalize → 9.6% annual returns

- High Case: Power, services, and end-market demand stay stronger for longer → 14.1% annual returns

Even in the conservative case, Caterpillar still looks like a high-quality industrial business with durable cash flow, a large backlog, and meaningful exposure to power infrastructure.

But the main valuation takeaway is that future returns now depend more on execution than on multiple expansion alone. After such a strong run, Caterpillar may still work, but it looks more like a quality compounder than an obvious bargain.

See what analysts think about CAT stock right now (Free with TIKR) >>>

Should You Invest in Caterpillar Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAT, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Caterpillar stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!