Key Takeaways:

- United Airlines is navigating rising fuel costs and capacity cuts while still expanding premium travel and fleet investments.

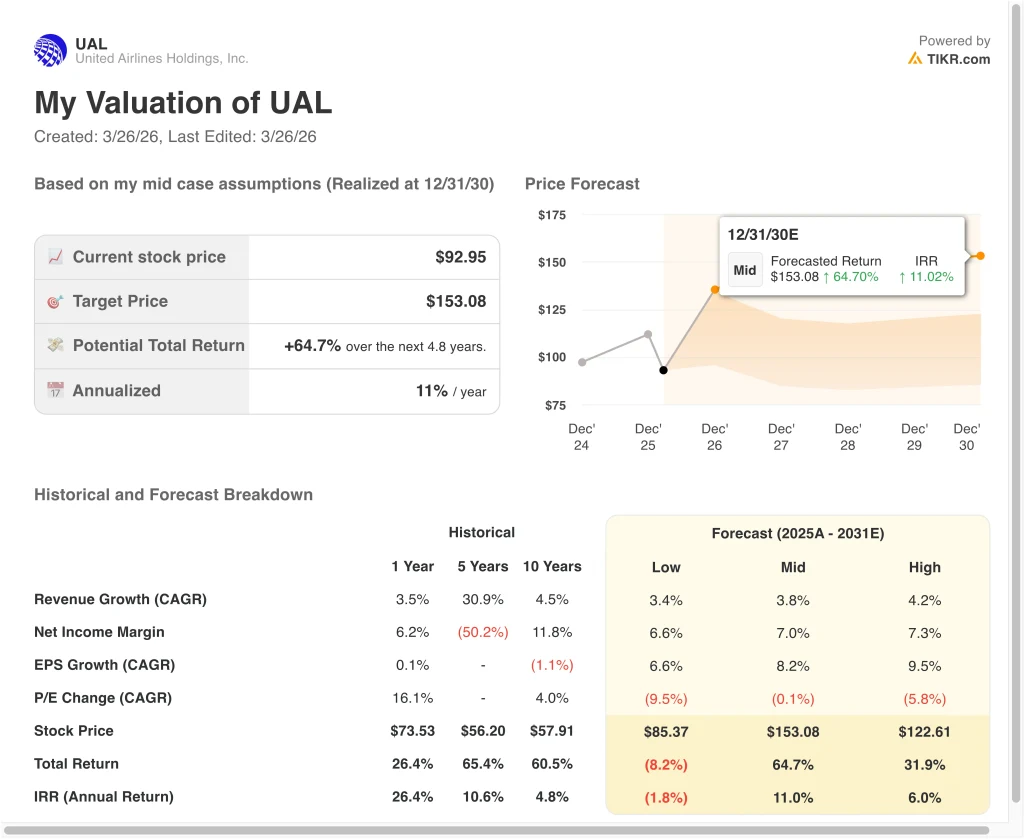

- UAL stock could reasonably reach $153 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 65% from today’s price of $92.95, with an annualized return of 11.0% over the next 4.8 years.

What Happened?

United Airlines (UAL) stock has been under pressure recently as investors react to rising fuel costs and capacity adjustments. The company warned that jet fuel prices could climb significantly, with management modeling scenarios where oil reaches $175 per barrel through 2027. That outlook has raised concerns about near-term profitability and margins across the airline industry.

At the same time, United announced plans to cut about 5% of scheduled flights due to higher fuel costs. This reflects a broader industry response, where airlines reduce capacity to protect pricing and margins when input costs rise. Investors are interpreting this as a defensive move, but also as a signal that demand elasticity may be tested if fares rise.

Recent commentary from CEO Scott Kirby reinforced this dynamic, noting that higher fuel prices will have a “meaningful” impact on first-quarter results. The company has also indicated that fares may increase in response, which could support revenue but risks dampening demand. This push-and-pull between pricing power and demand sensitivity is central to how the stock is being priced today.

Despite these pressures, United continues to invest aggressively in long-term growth. The airline plans to take delivery of over 250 new aircraft by 2028 and is expanding premium offerings. These investments suggest management is positioning for structural demand growth, even as short-term volatility remains elevated.

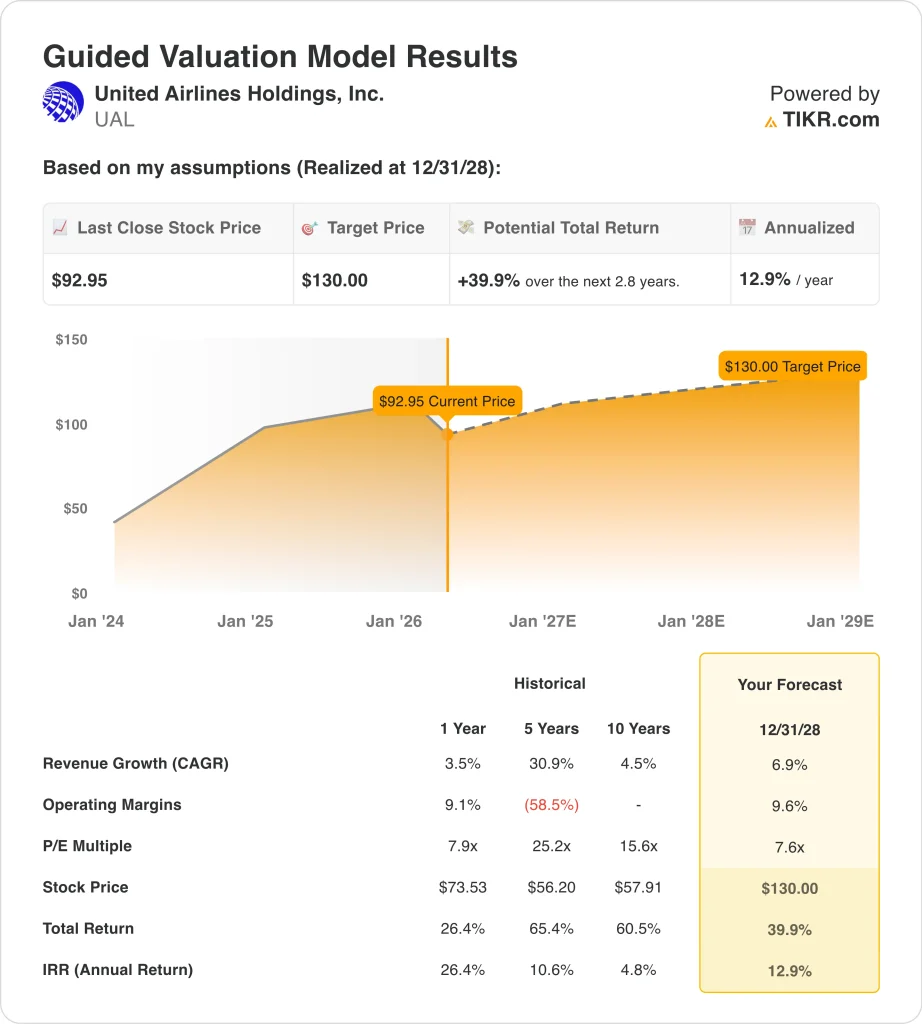

What the Model Says for UAL Stock

We analyzed the upside potential for United Airlines stock using valuation assumptions based on its steady revenue recovery, improving profitability, and ongoing fleet and premium expansion strategy.

Based on estimates of 6.9% annual revenue growth, 9.6% operating margins, and a 7.6x P/E multiple, the model projects UAL stock could rise from $93 to $130 per share by 2028.

That represents a 39.9% total return, or 12.9% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UAL stock:

1. Revenue Growth: 6.9%

United has delivered steady top-line recovery, with total revenue reaching about $59 billion in 2025, up from $24.6 billion in 2021. However, growth has slowed to 3.5% recently, reflecting normalization after post-pandemic demand recovery.

Management continues to focus on premium travel, international routes, and capacity optimization. The company is also expanding operations at key hubs like Chicago O’Hare, targeting higher utilization and pricing power.

Based on these trends, a 6.9% growth assumption reflects moderate expansion driven by pricing, premium mix, and fleet upgrades, balanced against macro uncertainty and fuel-driven demand risks.

2. Operating Margins: 9.6%

UAL’s operating margins have improved significantly from negative levels in 2021 to about 8.6% LTM. This reflects cost discipline, higher load factors, and improved pricing across key routes.

However, margins remain sensitive to fuel costs, which are one of the largest expense drivers. Recent guidance suggests near-term pressure, especially if oil prices remain elevated.

A 9.6% margin assumption reflects modest expansion from current levels, supported by premium offerings and efficiency gains, but constrained by structural cost volatility.

3. Exit P/E Multiple: 7.6x

UAL currently trades at a forward P/E of about 7.6x, which is in line with historical airline valuations. The sector typically trades at lower multiples due to cyclicality, capital intensity, and sensitivity to macro conditions.

Compared to peers like Delta and American Airlines, United’s valuation reflects a balance between growth investments and operational risk. The company’s improving balance sheet, with net debt declining to about $18.8 billion, supports valuation stability.

Based on analysts’ consensus estimates, we maintain a 7.6x exit multiple, assuming the market continues to value airlines conservatively despite improving fundamentals.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for UAL stock through 2030 varied outcomes based on revenue growth, margins, and valuation multiples (these are estimates, not guaranteed returns):

- Low Case: Fuel costs remain elevated, and demand weakens → -1.8% annual returns

- Mid Case: Stable demand and gradual margin expansion → 11.0% annual return

- High Case: Strong premium demand and cost control improve profitability → 6.0% annual returns

Even in the conservative case, United Airlines reflects a business that has structurally improved since 2021. Revenue growth, margin recovery, and debt reduction all point to a more resilient operating model.

However, the stock remains highly sensitive to external factors like oil prices, economic cycles, and travel demand. That’s why valuation remains relatively compressed despite improved fundamentals.

Even in the conservative case, UAL stock offers positive returns supported by its improving profitability, premium strategy, and disciplined capital allocation.

See what analysts think about UAL stock right now (Free with TIKR) >>>

Should You Invest in United Airlines?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UAL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UAL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze United Airlines stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!