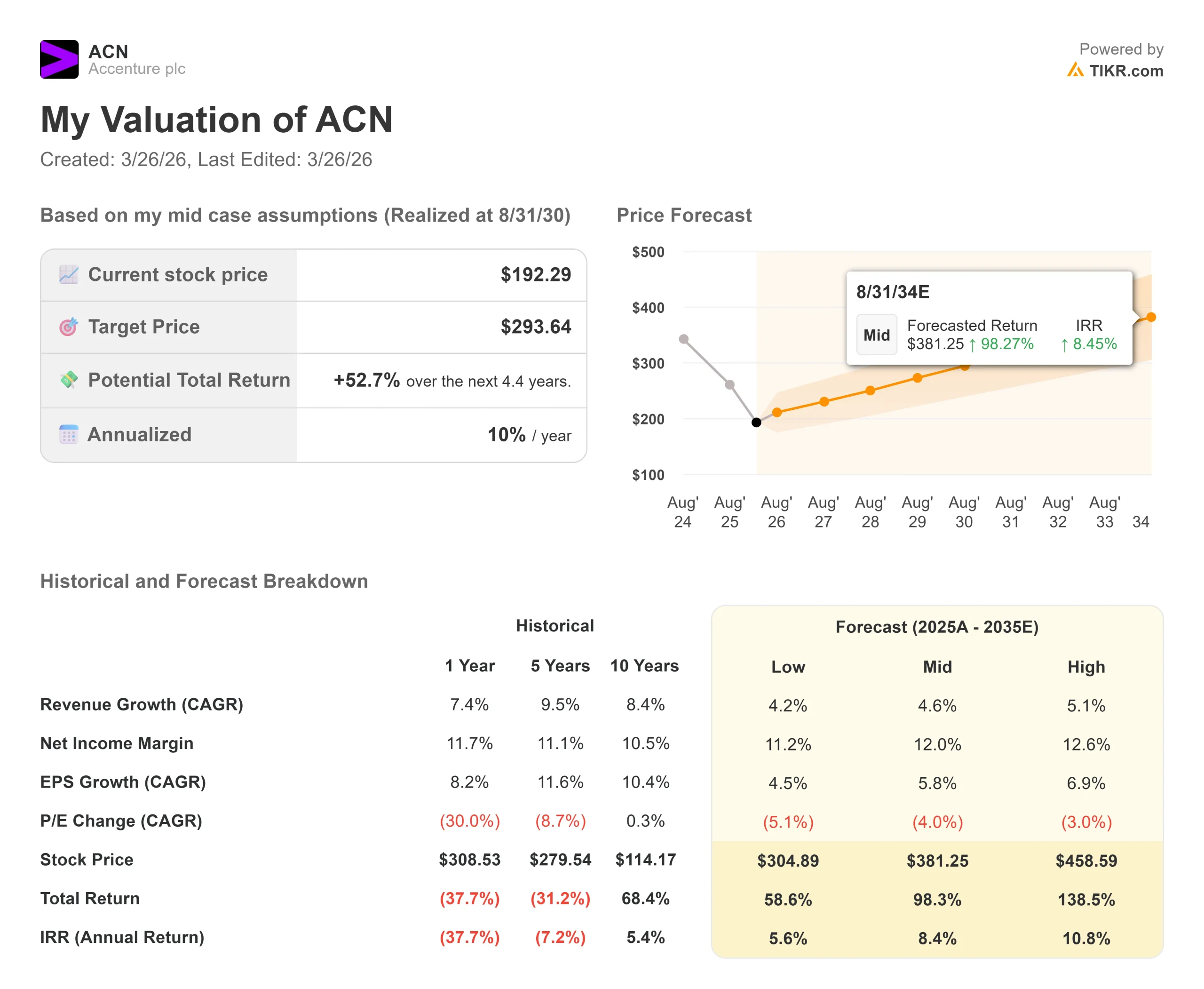

Key Stats for Accenture Stock

- Current Price: $192

- Target Price: $293

- Potential Total Return: +52.7%

- Annualized IRR: 10%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The global IT services sector has been shadowed by a lingering bearish narrative: corporate technology budgets are tightening, and traditional consulting firms that rely on billing clients by the hour will inevitably suffer.

However, during Accenture’s (ACN) Q2 2026 earnings call on March 19, CEO Julie Sweet completely dismantled this thesis.

While the broader market frets over discretionary spending cuts, Accenture is quietly experiencing a massive, multi-year reinvention cycle driven by enterprise artificial intelligence.

The sheer scale of their deal pipeline directly contradicts the narrative of a frozen IT market.

Accenture posted a staggering $22.1 billion in new bookings for the second quarter, pushing its first-half total to an incredible $43 billion.

Crucially, 41 different clients signed contracts worth more than $100 million in Q2 alone.

These mega-deals prove that large enterprises realize their newly modernized, cloud-based data cores are essentially useless without a sophisticated intelligence layer built on top of them.

To meet this demand, Accenture is radically evolving its own commercial model.

The company is actively pivoting away from an exclusive reliance on Full-Time Equivalent (FTE) structures, the legacy model of billing clients for human labor, and moving aggressively toward scalable subscription and licensing revenue.

To accelerate this, management has authorized an incredible $5 billion for acquisitions this year.

In the first half alone, they deployed $1.6 billion across strategic assets, including Faculty and other acquisitions. Separately, Accenture announced the acquisition of Ookla, a network intelligence leader, but had not yet closed it.

As Sweet noted, Ookla generated $231 million in 2025 revenue through non-FTE subscription and licensing revenue models, injecting highly accretive, non-FTE margins directly into Accenture’s ecosystem.

“We are continuing to take market share quarter after quarter because of the combination of our early leadership in advanced AI, our deep ecosystem partnerships with both established leaders and emerging players, and our decades of investments,” Sweet stated, highlighting how the firm’s unmatched scale serves as an impenetrable moat.

Internally, Accenture is applying the same technological medicine it sells to clients.

The company now boasts over 85,000 AI and data professionals, exceeding its fiscal 2026 target early.

Furthermore, 192,000 employees recently completed training in Agentic AI, systems where digital agents and human workers operate autonomously as a coordinated team.

By deploying these AI agents within its own delivery centers, Accenture is systematically stripping out its own back-office costs to protect its profitability.

See historical and forward estimates for Accenture stock (It’s free!) >>>

Is Accenture Undervalued Today?

The market’s current pricing of Accenture stock near $192 creates a massive dislocation between the company’s real-world cash generation and shareholder perception.

While some investors remain skeptical of the consulting sector’s exposure to macroeconomic headwinds, the underlying financial engine of Accenture is firing on all cylinders.

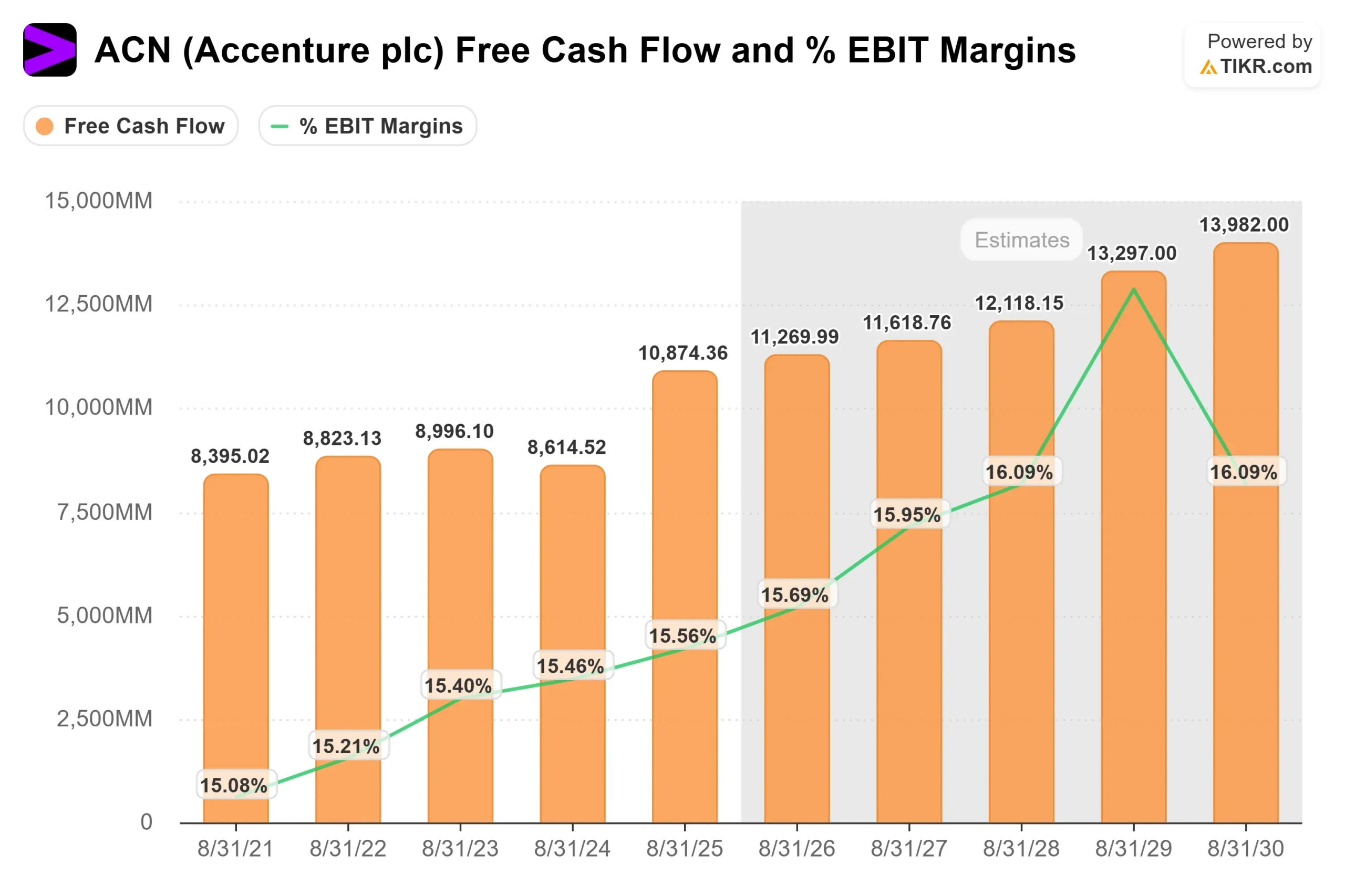

In the Q2 report, CFO Angie Park raised the full-year free cash flow guidance by $1 billion to an eye-watering range of $10.8 billion to $11.5 billion, reflecting a pristine free cash flow-to-net income conversion ratio of 1.3.

Management is not letting this cash sit idle; they are ruthlessly taking advantage of the depressed share price.

The company accelerated repurchases to buy back $1.7 billion in stock in Q2 alone, bringing the year-to-date total to $4 billion.

When a company is actively shrinking its outstanding share float by billions of dollars while simultaneously acquiring high-growth, non-FTE software assets like Ookla, the per-share intrinsic value compounds rapidly.

With total revenue guidance updated to 3% to 5% growth in local currency and operating margins steadily expanding (up 30 basis points year-over-year in Q2), the current price point fails to reflect Accenture’s successful pivot from a pure labor-arbitrage consulting firm into an integrated, AI-driven managed services monopoly.

Analyze historical revenue and share repurchases for ACN (It’s free!) >>>

The TIKR Model Analysis

The TIKR Advanced Model calculates the long-term compounding impact of Accenture, leveraging its $43 billion first-half bookings backlog and successfully pivoting toward high-margin AI subscription products.

- Current Price: $192

- Target Price: $293

- Potential Total Return: +52.7%

- Annualized IRR: 10%

Build a 4-year Valuation Model for ACN for yourself (It’s free) >>>

The Mid Case projection confidently issues a $293.64 target price. The true lever for this valuation is the forecasted defense and expansion of its profitability. TIKR’s historical snippet shows Accenture’s Net Income Margin tracking near 11.1% over the last year. Achieving the modeled 10.0% annualized return requires flawless execution of their $5 billion non-FTE acquisition strategy to reverse historic margin compression, alongside the continuous use of internal Agentic AI tools to reduce the human cost of delivering Managed Services.

If management successfully captures these delivery efficiencies while continuously shrinking the share float via their massive $4 billion buyback program, the current $192 entry point represents a rare opportunity to buy a dominant tech ecosystem at a steep discount.

Conclusion: Accenture is not just surviving the AI revolution; it is engineering the foundational infrastructure for the rest of the Fortune 500 to participate in it. While the broader market remains overly focused on traditional hourly consulting, the underlying reality, a $5 billion M&A war chest, $22 billion in quarterly bookings, and an upwardly revised $11.5 billion free cash flow target, screams value. Watch the upcoming quarters for the integration metrics on Faculty and Ookla; if those subscription models scale seamlessly into Accenture’s massive client base, the path to the $293 target is exceptionally clear.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Accenture?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Accenture, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Accenture alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Accenture on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!