Key Stats for Tyler Technologies Stock

- This Week Performance: -3.9%

- 52-Week Range: $283.7 to $621.3

- Current Price: $341.1

What Happened?

Tyler Technologies (TYL), the dominant software provider for U.S. local and state governments, sits 45% below its 52-week high of $621.34 despite posting record free cash flow of $620.8M in FY 2025 and authorizing a fresh $1.0B buyback in February, creating a valuation reset that increasingly looks disconnected from the underlying business.

CFO Brian Miller confirmed that the subscription revenue grew 16.1% while SaaS revenue, the cloud-native subset that carries the highest margins, surpassed $200M in a single quarter for the first time, even as total Q4 revenue of $575.2M missed the $591.1M consensus estimate and sent shares down over 8% in extended trading.

The operational engine behind the beat-and-guide dynamic is Tyler’s cloud migration program, in which on-premises government clients convert their legacy software licenses to subscription agreements at a 1.7x to 1.8x revenue uplift, with Q4 2025 setting an all-time quarterly record for both the number and dollar value of those conversions, including L.A. County, Travis County, and Collin County among the notable signings.

Lynn Moore, President and CEO, also stated on the same Q4 2025 earnings call that “annual contract value from flips signed this quarter rose 64.5% over last year and 54.8% sequentially,” anchoring forward SaaS revenue confidence at a moment when the company’s 2026 guidance for 20.5% to 22.5% SaaS growth has already been de-risked by roughly 13 percentage points of that target sitting in contracted but not yet recognized backlog.

The pending $212.5M acquisition of For The Record, a digital court-recording platform with AI-powered multilingual transcription, a June 9 Investor Day in Frisco where management will detail the AI product roadmap, and a $885M remaining buyback authorization collectively frame a multi-year compounding case: Tyler’s 2030 target of $1.0B in free cash flow rests on a cloud transition that is still only 53% complete across its 45,000-installation base.

Wall Street’s Take on TYL Stock

The record Q4 free cash flow print and the all-time high flip quarter together confirm that Tyler’s cloud transition, the operational shift driving both revenue uplift and margin expansion, is accelerating precisely as the stock trades at its most depressed multiple in years.

Normalized EPS grew to $11.31 in FY 2025 and, as TIKR estimates, expands to $12.54 in FY 2026 and $14.19 in FY 2027, supported by SaaS guidance of 20.5% to 22.5% growth and an EBITDA margin expanding from 27.9% toward 29.2%, both driven by the 1.7x to 1.8x revenue uplift from on-premises clients converting to cloud subscriptions.

Twelve analysts currently rate TYL a buy, six an outperform, and four a hold, with a mean price target of $443.48 implying 30.0% upside from the current $341.07 close, reflecting Street conviction that the Q4 earnings miss was a timing and contract-reserve issue, not a structural deterioration.

The analyst target range spans $325.00 on the low end to $650.00 on the high end, where the bear case hinges on prolonged government budget caution slowing SaaS bookings, and the bull case reflects full execution on the 2027 to 2029 flip peak that CFO Brian Miller has now guided toward explicitly.

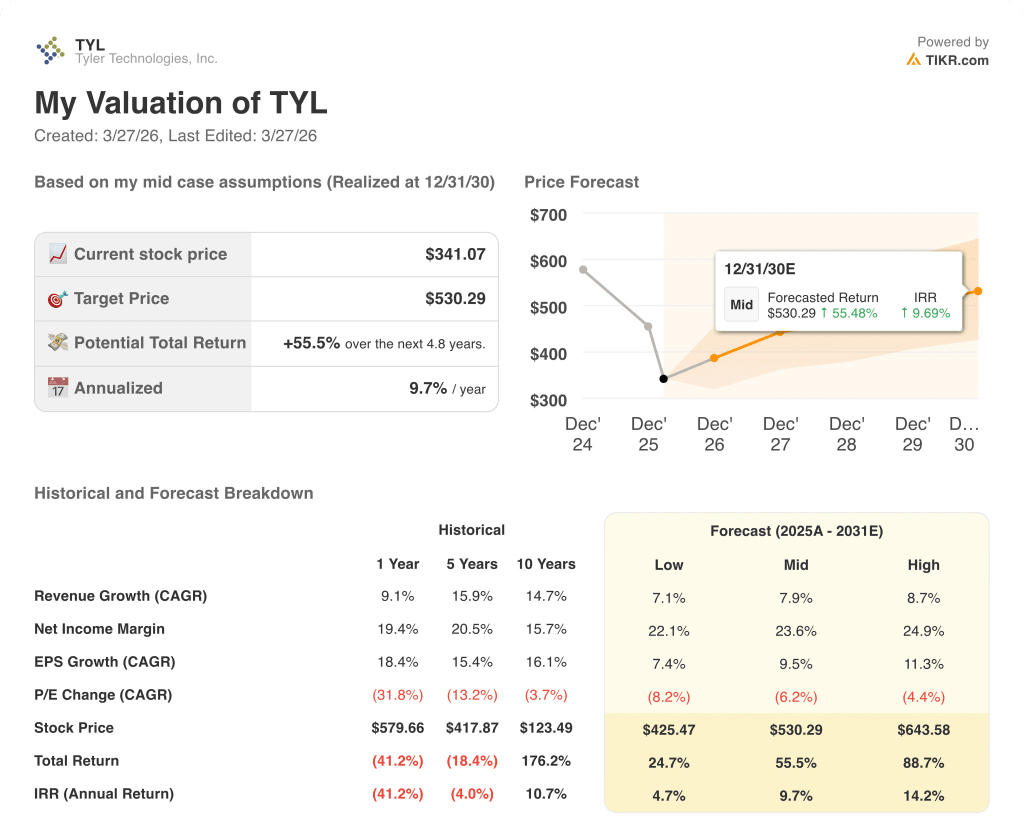

What Does the Valuation Model Say?

The TIKR mid-case model sets a price target of $530.29 by December 2030, implying a 55.5% total return and a 9.7% IRR, anchored to a 7.9% revenue CAGR and net income margins expanding from 19.4% today toward 23.6%, both of which are conservative relative to management’s own 30%+ non-GAAP operating margin target for the same period.

The market is pricing Tyler as if the cloud transition is stalling, yet Q4 delivered record flip volumes with ACV up 64.5% year over year.

The TIKR $530.29 target rests on roughly 8% annual revenue growth, already bracketed by the company’s own $2.50B to $2.55B FY 2026 guidance and a backlog where 13 percentage points of the 21.5% SaaS midpoint is already contracted.

Management’s authorization of a $1.0B buyback at current levels, with $885.0M still available, signals that the board views $341 as a structural discount, not a fair reflection of the compounding FCF trajectory.

The key risk is that government budgets tighten faster than expected, compressing SaaS bookings growth below the 4% full-year 2025 baseline and pushing the flip peak beyond the 2027 to 2029 window the model assumes.

The June 9 Investor Day in Frisco will be the clearest confirmation point, where updated 2030 targets and the AI product monetization roadmap will either validate or challenge the TIKR model’s 7.9% revenue CAGR assumption.

Should You Invest in Tyler Technologies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TYL stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Tyler Technologies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TYL stock on TIKR for Free →