Key Takeaways:

- Verizon’s recent rerating has been driven by a fourth-quarter earnings beat, stronger 2026 guidance, the closing of the Frontier deal, and a more aggressive capital return plan.

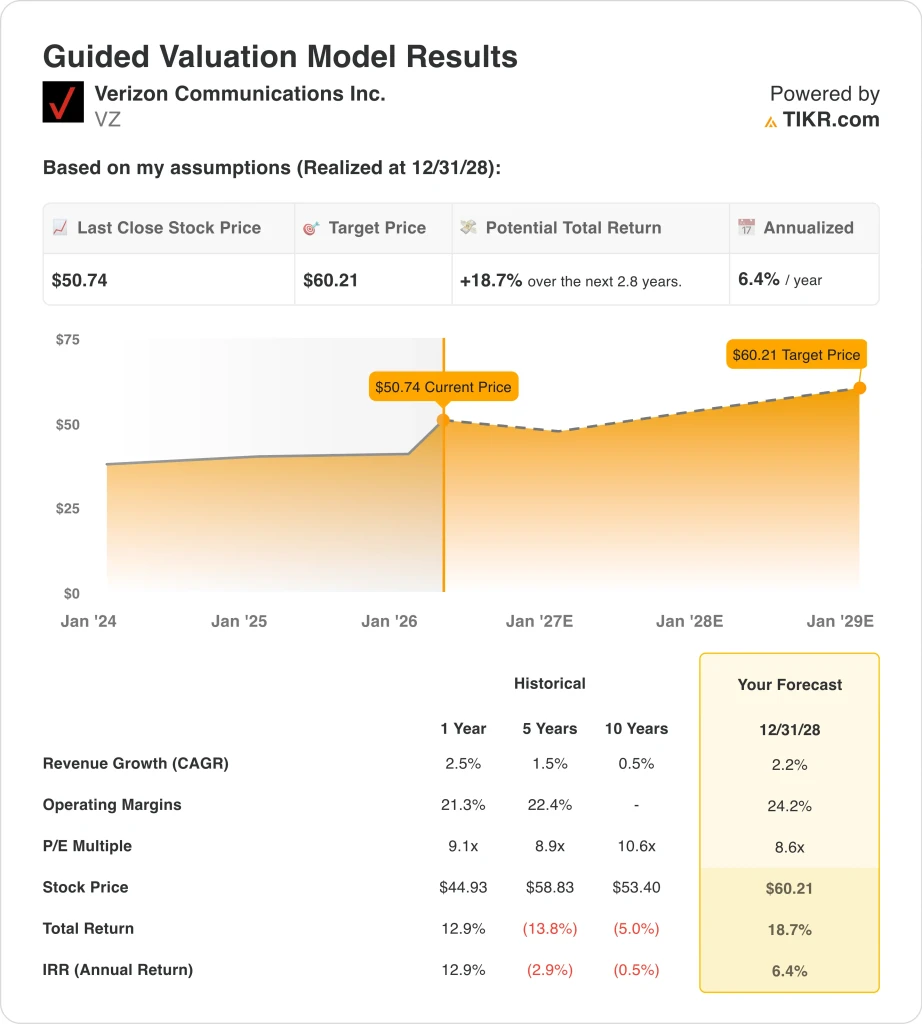

- Verizon stock now trades near $51, while the valuation model points to a $60 fair value by 2028 based on 2.2% revenue growth, 24.2% operating margins, and an 8.6x P/E multiple.

- That implies an 18.7% total return from today’s price of $50.74, or a 6.4% annualized return over the next 2.8 years.

What Happened?

Verizon Communications Inc. (VZ) stock moved higher because the market got a cleaner operating story in late January. The company posted 616,000 postpaid phone net additions in Q4 2025, which was its best fourth quarter for that metric since 2019. It also reported 372,000 broadband net additions, including 319,000 fixed wireless access net additions, so investors saw growth in both mobile and home connectivity.

The guidance also changed the tone. Verizon said 2026 adjusted EPS should land between $4.90 and $4.95, and it expects total mobility and broadband service revenue growth of 2.0% to 3.0%. That matters because Verizon had spent much of the last few years trading like a slow-growth defensive stock, but this outlook suggested the company may be entering a more stable growth phase.

The Frontier deal added another reason for the market to pay attention. Verizon said the transaction expands its fiber footprint to almost 30 million passings, and that gives it more homes and businesses to sell into with bundled wireless and broadband products. In telecom, bundling matters because it can lower churn, lift household revenue, and make customer acquisition more efficient over time.

Still, investors are not treating Verizon like a no-risk turnaround. Reuters reported in February that Verizon Consumer Group CEO Sowmyanarayan Sampath is stepping down, while March brought legal noise from the advertising dispute with T-Mobile and fresh regulatory discussion around foreign telecom call centers. The next major catalyst is first-quarter earnings on April 27, so the market is now waiting to see whether the better Q4 momentum carries into the rest of the year.

Here’s why Verizon stock could deliver positive but more moderate returns through 2028 as better subscriber growth, broadband scale, and cost discipline support earnings, but much of the early rerating has already happened.

What the Model Says for VZ Stock

We analyzed the upside potential for Verizon stock using valuation assumptions based on its larger broadband footprint, stable wireless cash flows, and moderate earnings growth outlook.

Based on estimates of 2.2% annual revenue growth, 24.2% operating margins, and a normalized P/E multiple of 8.6x, the model projects Verizon stock could rise from $50.74 to $60.21 per share.

That would be a 18.7% total return, or a 6.4% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for VZ stock:

1. Revenue Growth: 2.2%

Verizon’s revenue base has been steady, and that is the right place to start. Revenue was $138.2 billion in 2025, up 2.5% from $134.8 billion in 2024, after a 0.6% increase in 2024 and a 2.1% decline in 2023. That pattern fits a mature telecom business that can still grow, but usually does so gradually.

The drivers behind that growth are becoming more balanced. Wireless service remains the biggest engine, but Verizon is also adding broadband customers through Fios and fixed wireless access. In Q4 2025, Verizon reported 372,000 broadband net additions, including 67,000 Fios internet net additions, which was its best fourth quarter for Fios net adds since 2020.

Based on analysts’ consensus estimates, we used a 2.2% forecast. That fits Verizon’s 2026 guidance for 2.0% to 3.0% total mobility and broadband service revenue growth, and it also reflects the broader fiber opportunity created by the Frontier acquisition. It is a modest assumption, but it matches the company’s size, market position, and recent growth profile.

2. Operating Margins: 24.2%

Verizon remains a profitable business, even though growth is not fast. Operating income was $31.6 billion in 2025, and operating margin was 22.9%, while gross margin was 59.1%. Those figures show why investors still treat Verizon as a cash-generating telecom leader rather than a structurally impaired asset.

Margins matter here because telecom is capital-intensive, and Verizon still carries a large network and debt load. The company generated $37.1 billion of operating cash flow and $20.1 billion of free cash flow in 2025, so profitability is what funds dividends, debt service, and network investment. That also explains why investors responded well when management paired stronger growth signals with disciplined financial targets.

Based on analysts’ consensus estimates, we use 24.2% operating margins. That is above the recent 22.9% level, but it is not an aggressive leap if Verizon gets a better mix, more scale from broadband, and cleaner cost execution. It also fits the company’s turnaround message, which is focused on healthier volumes and more efficient operations.

3. Exit P/E Multiple: 8.6x

Verizon is not being valued like a growth stock, and the model reflects that. The shares currently trade at about 9.0x earnings based on market data, while the guided valuation model uses an 8.6x exit P/E. That means the valuation case does not rely on investors paying a richer multiple in the future.

That conservative multiple makes sense because leverage still shapes the story. Verizon ended 2025 with $184.8 billion of total debt and $165.8 billion of net debt, while TIKR overview data shows LTM net debt to EBITDA at 2.97x. The company also issued €2.25 billion and £600 million of junior subordinated notes in February, so balance-sheet management remains central to the investment case.

Based on analysts’ consensus estimates, we maintain an 8.6x exit multiple. That is a practical assumption for a mature telecom with a high dividend yield, slower top-line growth, and a large debt burden. So if the stock outperforms from here, it will likely come from earnings and cash flow improving faster than expected, not from a big expansion in valuation.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

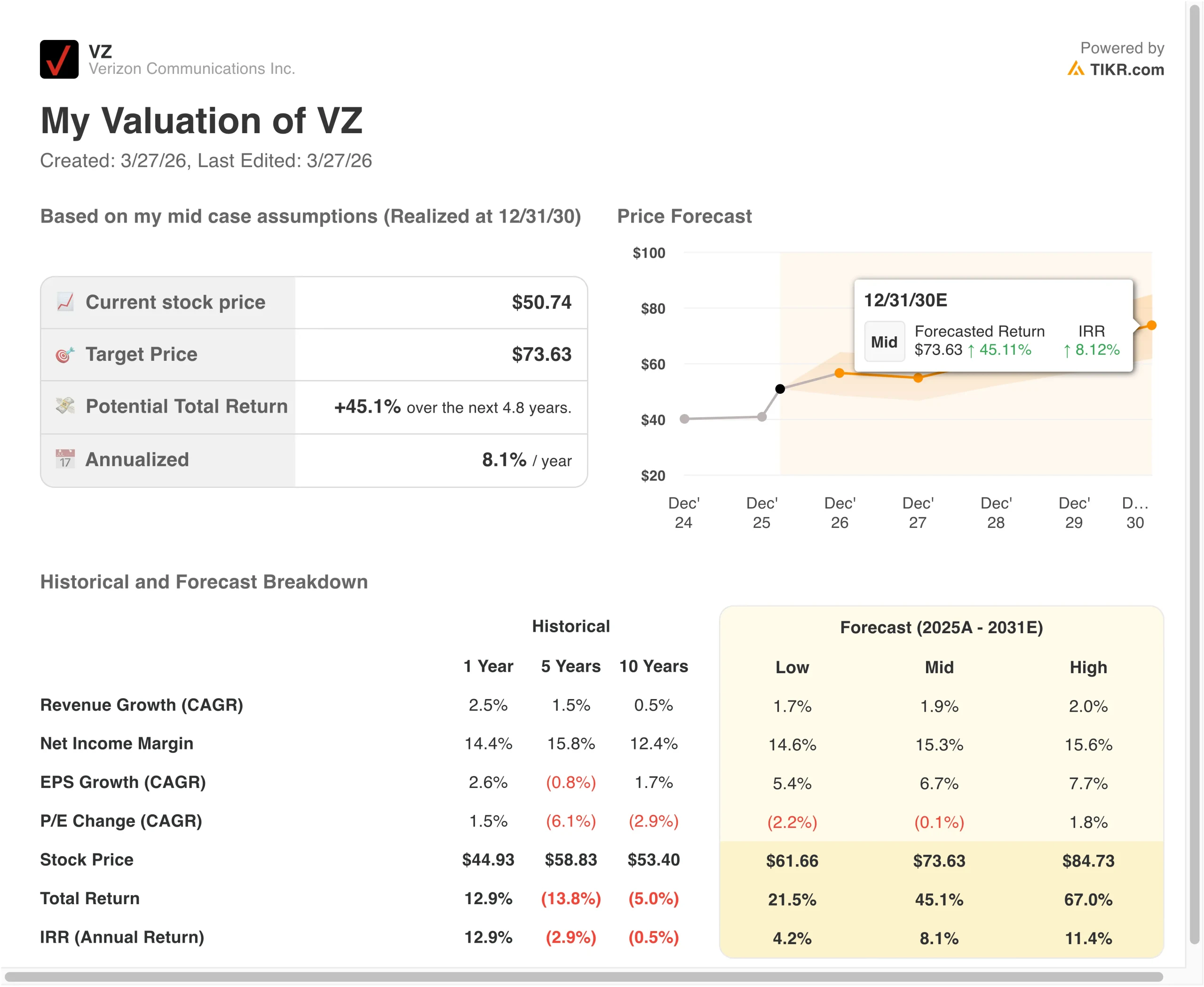

Different scenarios for Verizon stock through 2030 show varied outcomes based on wireless growth, broadband execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Verizon’s broadband growth slows, wireless competition stays intense, and margin expansion remains limited → 4.2% annual returns

- Mid Case: Verizon continues to grow broadband and wireless service revenue steadily, while margins improve modestly → 8.1% annual returns

- High Case: Verizon executes well on fiber expansion, broadband bundling, and subscriber growth, while profitability improves further → 11.4% annual returns

Even in the low case, Verizon still appears supported by its recurring service revenue, large wireless base, and strong dividend profile. The mid case suggests the stock can still produce respectable returns, but not enough to clearly stand out as deeply undervalued today. The high case shows that stronger execution in broadband and margins could create more attractive long-term returns, especially if Verizon proves that recent momentum is sustainable.

Going forward, investors will likely focus most on postpaid phone net additions, broadband customer growth, and free cash flow execution. The April 21, 2026, earnings report is the next major checkpoint, because it will show whether the stronger Q4 trends are continuing into the new year. If Verizon keeps improving growth while managing leverage and protecting margins, the stock could continue to justify a higher valuation over time.

See what analysts think about VZ stock right now (Free with TIKR) >>>

Should You Invest in Verizon Communications Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VZ, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VZ alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Verizon Communications stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!