Key Stats for KLA Stock

- This Week Performance: +3.2%

- 52-Week Range: $551.3 to $1,693.4

- Current Price: $1,451.1

What Happened?

KLA Corporation (KLAC), the semiconductor process control equipment leader that inspects and measures chip defects to improve manufacturing yields, set a $26 billion revenue target for 2030 at its March 12 Investor Day, implying roughly 15% annual growth from its record $12.7 billion in 2025, even as shares trade at $1,451.13 following a 6% single-session pullback on March 26.

At the same March 12 Investor Day, KLA’s board authorized a new $7 billion share repurchase program on top of $3.94 billion remaining from its April 2025 authorization, and raised its quarterly dividend 21% to $2.30 per share, marking the company’s 17th consecutive annual dividend increase.

KLA’s process control intensity metric, which measures how much chipmakers spend on inspection and measurement tools as a share of total equipment spending, rose from 5.3% to 7.4% between 2019 and 2025 and is targeted to reach 9% by 2030, a structural shift driven by larger AI chip die sizes, more complex high-bandwidth memory stacking, and advanced packaging, where KLA grew from 10% market share in 2020 to roughly 50% in 2025.

Bren Higgins, CFO and Executive Vice President of Global Operations, stated on the same Investor Day that “our view for 2026 now is that we expect the total company to be up somewhere in the high teens in terms of year-over-year growth versus 2025,” reflecting strengthening customer momentum and improved second-half visibility tied to greenfield fab construction schedules.

KLA’s 2030 model projects $84 non-GAAP EPS and operating margins of 45% to 47%, supported by a combined roughly $11 billion in buyback authorization, a raised service revenue growth target of 13% to 15% annually, and an e-beam inspection business that expanded from under $100 million to $400 million in revenue and continues scaling into high-bandwidth memory production.

Wall Street’s Take on KLA Stock

The March 12 Investor Day’s $26 billion 2030 revenue target and combined roughly $11 billion in buyback authorization directly support TIKR’s FY2026E free cash flow estimate of $4.81 billion, up 28.3% from $3.75 billion in FY2025, as process control intensity expansion funds shareholder returns simultaneously.

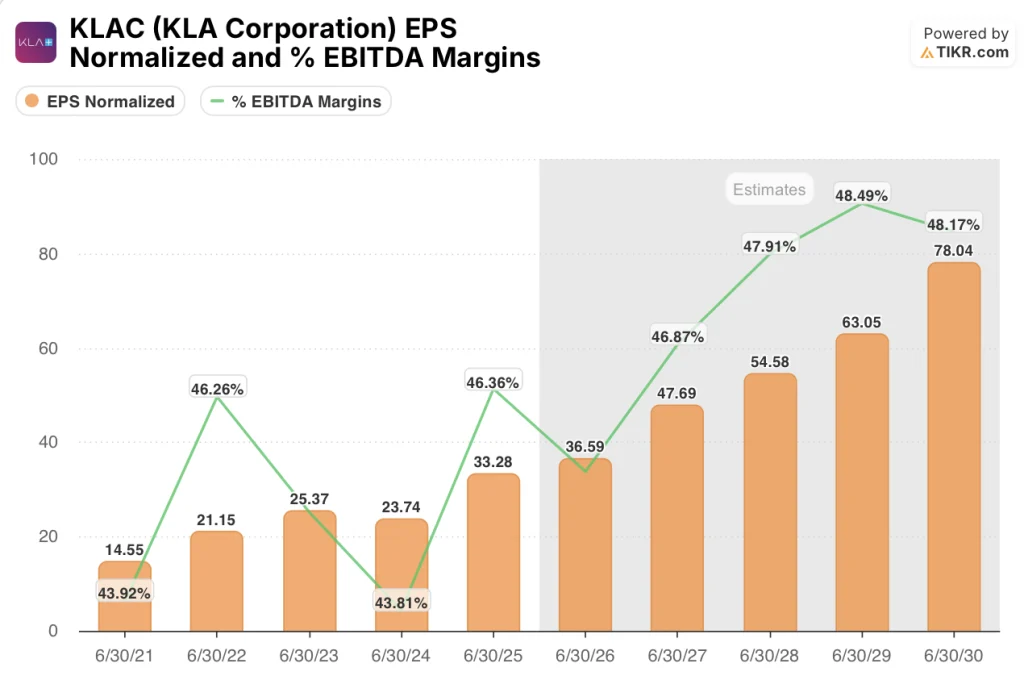

TIKR estimates place KLA’s normalized EPS at $33.28 in FY2025, rising to $36.59 in FY2026E and $78.04 by FY2030E, a 17.3% CAGR, as greenfield fab construction, accelerating high-bandwidth memory adoption, and advanced packaging share gains drive EBITDA margins from 46.4% to 48.2% while the service business, which tripled from $1 billion to $3 billion in six years, compounds at its raised 13% to 15% annual target.

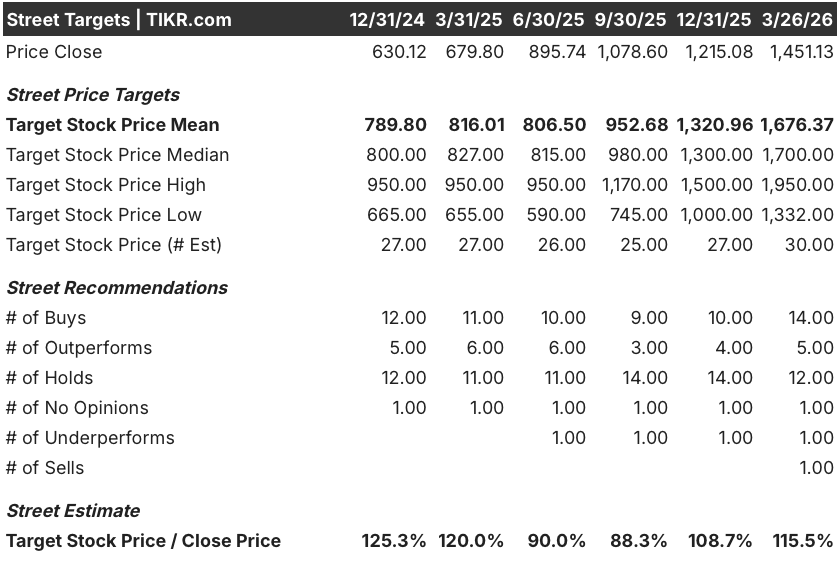

Fourteen analysts rate KLAC a buy, five say outperform, and twelve hold, with a mean price target of $1,676.37 implying 15.5% upside from $1,451.13, a consensus that reflects confidence in KLA’s 2026 high-teens revenue growth guidance but likely underweights the structural intensity expansion driving the 2030 model.

The spread between the Street’s low target of $1,332.00 and high of $1,950.00 maps precisely to the two dominant risks: the low anchors to gross margin compression from DRAM chip inflation and tariffs already flagged as a combined 125 to 200 basis point headwind, while the high reflects full execution on advanced packaging share and greenfield-driven second-half 2026 acceleration.

What Does the Valuation Model Say?

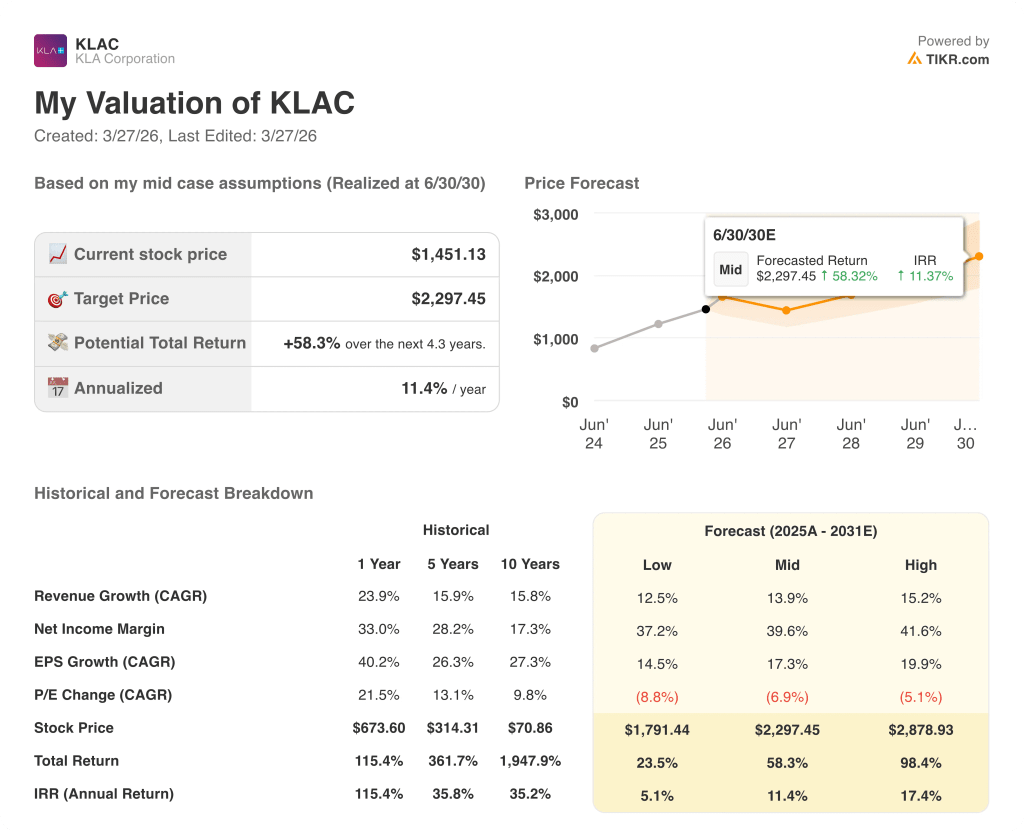

The TIKR mid-case target of $2,297.45, implying 58.3% total return at an 11.4% IRR by June 30, 2030, is built on 13.9% revenue CAGR and net income margin expansion to 39.6%, justified by KLA’s process control intensity rising from 7.4% to a targeted 9% of a $215 billion wafer equipment market that management sees as structurally underpinned by AI-driven chip complexity.

The market is treating the March 26 6% selloff as cyclical noise, but KLA’s FCF margin already reached 35.9% in FY2026E estimates — proof the compounding model survives cost headwinds.

TIKR’s $2,297.45 target requires 13.9% revenue CAGR; KLA’s own 2030 plan targets $26 billion from $12.7 billion, implying roughly 15% annually — the model’s core assumption is actually conservative relative to management’s own guidance.

KLA’s service business, now $3 billion annually and growing at a raised 13% to 15% target with 80%-plus contract penetration and 95% two-year revenue recurrence, signals durable compounding that purely equipment-cycle-focused investors continue to underweight.

Gross margin guidance of approximately 62% for full-year 2026, already flagged as the cycle trough, breaks the TIKR model if DRAM chip inflation persists beyond 2026 and prevents the expected recovery toward the 63%-plus long-term target.

The June 2026 quarter guidance, expected to confirm second-half 2026 acceleration toward approximately 20% year-over-year Semi PC systems growth, is the single number that validates whether KLA’s supply constraints are clearing on schedule.

Should You Invest in KLA Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up KLAC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track KLA Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze KLAC stock on TIKR for Free →