Key Stats for NXP Stock

- This Week Performance: +2.9%

- 52-Week Range: $148.1 to $256.4

- Current Price: $196.9

What Happened?

NXP Semiconductors (NXPI), a Dutch chipmaker supplying processors and software for cars, factories, and connected devices, crossed a structural inflection point in Q4 2025 as its automotive accelerated growth drivers, the higher-value products tied to software-defined vehicles and advanced driver assistance, rose to 43% of auto revenue and the industrial segment posted 24% year-over-year growth, even as the stock sits 23% below its 52-week high of $256.36 at $196.92.

NXP reported Q4 2025 revenue of $3.34B on February 3, beating the IBES estimate of $3.31B, with non-GAAP EPS of $3.35 topping the $3.27 consensus, while Q1 2026 guidance of $3.15B implies 11% year-over-year growth, the strongest forward signal the company has issued in several years.

NXP’s industrial and IoT segment, which sells edge processors and microcontrollers to factories, medical devices, and energy systems, grew 24% year-over-year in Q4, with its physical AI products, chips running artificial intelligence locally on devices rather than in the cloud, growing roughly 30% in 2025 and expected to more than double their revenue share in 2026, outpacing peers Infineon and STMicroelectronics on industrial AI traction.

Rafael Sotomayor, President and CEO, stated on the Q4 2025 earnings call that “the NXP-specific secular drivers for our business are now outweighing the broader industry cyclical headwinds, which we have experienced over the last few years,” a claim backed by broad year-over-year growth across all four segments in Q1 2026 guidance.

NXP’s path to earnings compounding rests on three converging forces: SDV processors scaling from $1B in 2024 toward a $2B target by 2027, the VSMC joint venture in Singapore, a 300-millimeter fabrication facility built with Vanguard and TSMC expertise, unlocking 200 basis points of gross margin expansion upon full load in 2028, and a capital return program that has delivered $23B to shareholders over a decade while net leverage sits at a manageable 1.9x.

Wall Street’s Take on NXPI Stock

The Q4 2025 beat, which landed revenue 7% above the year-ago period and non-GAAP EPS at $3.35 against a $3.27 consensus, confirms that NXP’s inventory correction is fully behind it and that content-driven growth in software-defined vehicles and physical AI edge computing is now the primary revenue engine.

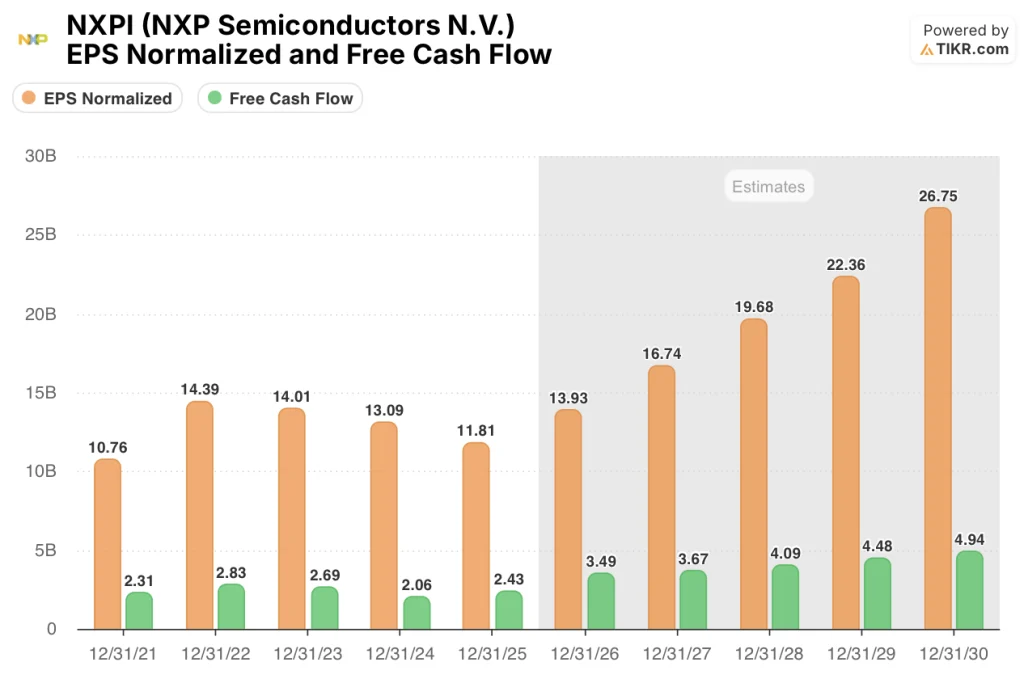

FCF surged 18% in 2025 to $2.43B after two consecutive years of decline, and the TIKR model projects a 43.9% jump to $3.49B in 2026 as factory utilization recovers and the MEMS divestiture removes a below-corporate-margin drag on the cost structure.

Normalized EPS of $11.81 in 2025 is forecast to reach $13.93 in 2026 and $16.74 in 2027, compounding at roughly 19%-20% annually, driven by the SDV processor ramp, physical AI design win conversions, and EBIT margin expansion from 33.1% to 36.9% over the same window.

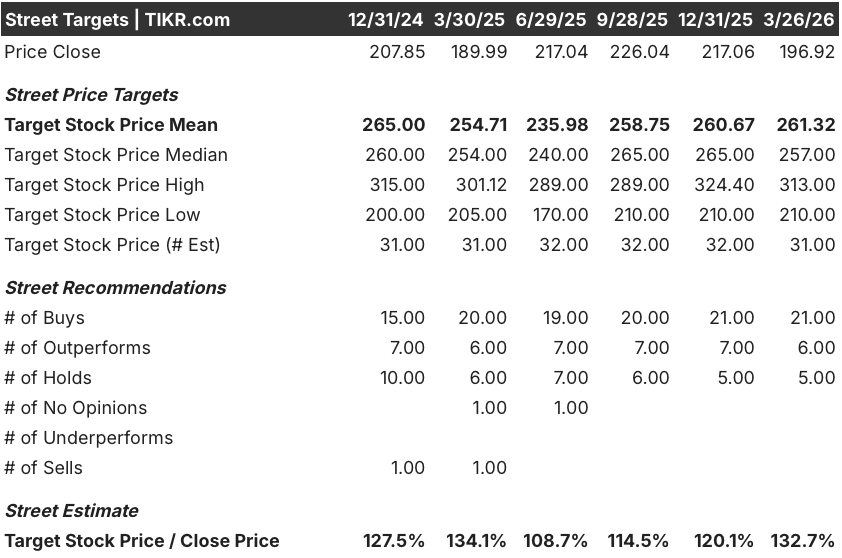

Twenty-one analysts rate NXPI a buy, six call it outperform, and five hold, with zero sells, a mean price target of $261.32 representing 32.7% upside from the current $196.92, as the Street anticipates the 11% year-over-year Q1 2026 guidance as evidence that the multi-year growth model is re-engaging on schedule.

The spread between the $210.00 low target and $313.00 high target reflects genuine disagreement about execution pace: the bear case anchors to subdued auto production volumes and EV program delays, while the bull case prices in full SDV ramp momentum and the VSMC gross margin tailwind arriving in 2028.

What Does the Valuation Model Say?

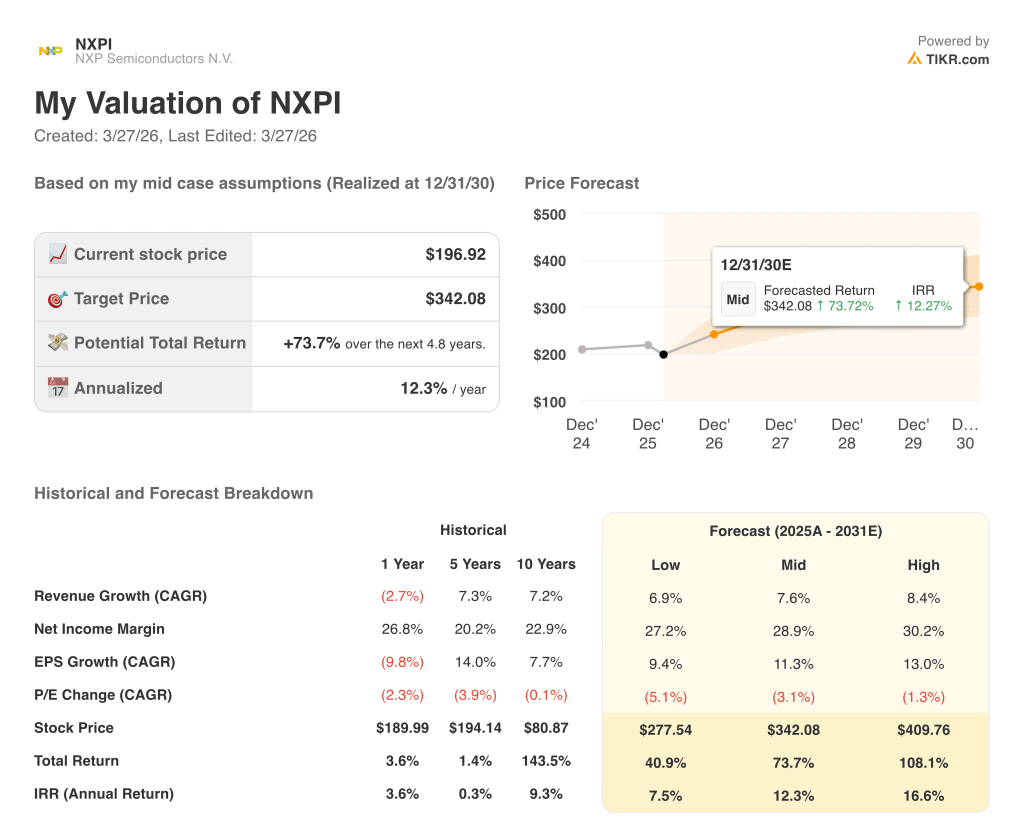

The TIKR mid-case model targets $342.08 by December 2030, implying a 12.3% annualized return, anchored to a 7.6% revenue CAGR, normalized EPS compounding at 11.3% annually, and net income margins expanding from 24.5% in 2025 to 28.9% by 2030 as VSMC wafer economics and operating leverage kick in.

The market is pricing NXP at roughly 14x 2026 normalized EPS of $13.93, a discount that ignores the 43.9% FCF inflection already baked into next year’s estimates.

Industrial and IoT physical AI revenue, the segment where on-device inference chips replace cloud-dependent processing, is doubling its revenue share in 2026 on an already-growing base, directly validating the TIKR model’s 10.3% revenue growth assumption for the year.

CEO Rafael Sotomayor stated on the Q4 2025 earnings call that NXP-specific secular drivers are now outweighing cyclical headwinds, a signal that management is guiding with visibility, not hope.

The risk is automotive content-per-vehicle growth stalling: if SDV platform program ramps slip past 2027, the TIKR model’s 10.2% 2027 revenue growth assumption breaks, and the 36.9% EBIT margin target becomes unreachable.

Q2 2026 results will be the first clean print without MEMS revenue noise, and investors should watch whether industrial and IoT sustains the low-20% year-over-year growth rate that underpins the full-year FCF expansion thesis.

Should You Invest in NXP Semiconductors N.V.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NXPI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NXP Semiconductors N.V. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NXPI stock on TIKR for Free →