Key Takeaways:

- Seagate is benefiting from stronger AI-driven data center storage demand, better pricing, and a sharp recovery in margins.

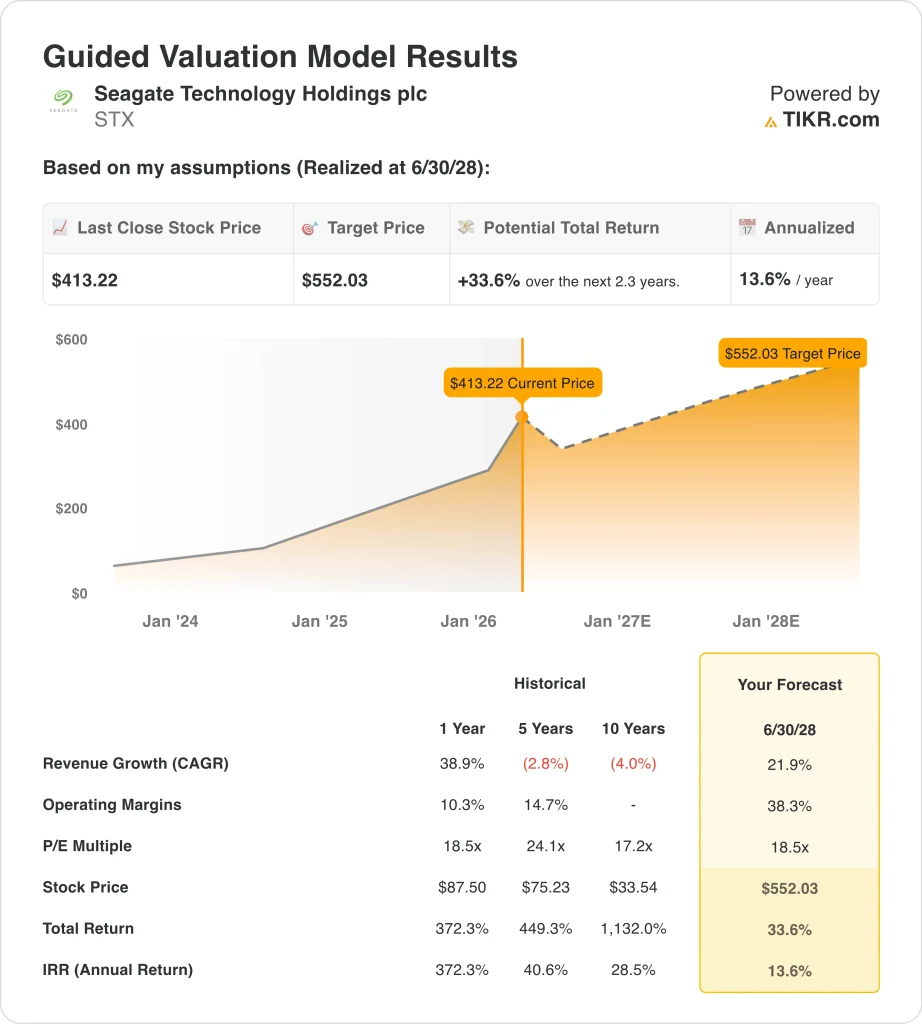

- STX stock could reasonably reach $552 per share by June 2028, based on our valuation assumptions.

- This implies a total return of 33.6% from today’s price of $413, with an annualized return of 13.6% over the next 2.3 years.

What Happened?

Seagate stock has been moving on the same broad theme that pushed storage names sharply higher in late 2025 and early 2026. Reuters reported that Seagate and Western Digital surged on AI-driven demand as cloud and hyperscale customers increased spending on storage tied to AI infrastructure. That helped explain why Seagate’s shares more than tripled over the past year before the recent pullback.

The January earnings report reinforced that story. Reuters said Seagate forecast quarterly results above estimates on strong data storage demand, while the company itself reported record exabyte shipments, record margins, and record non-GAAP EPS for the quarter.

Recent market moves show that sentiment is still volatile, though. Reuters reported on March 25 that memory-related stocks fell after Google announced a memory-saving algorithm, which reminded investors that AI infrastructure names can move sharply on any news that might affect future hardware demand. Seagate is not a memory chipmaker, but it trades in the same broader AI hardware conversation, so shifts in that narrative can still pressure the stock.

Furthermore, several insider sale disclosures during February and March, including sales by CEO Dave Mosley and other executives. Although those filings do not change the underlying business, they can affect short-term sentiment after a huge run in the stock.

Investors are now looking ahead to Seagate’s expected Q3 2026 results on April 24 to see whether data center demand, pricing, and margins remain this strong.

Here’s why Seagate stock could provide solid returns through 2030 as AI-related storage demand supports revenue growth, higher margins, and better earnings power. But after such a sharp rally, the stock is also being priced against tougher expectations and more sensitivity to any sign of demand cooling.

What the Model Says for STX Stock

We analyzed the upside potential for Seagate stock using valuation assumptions based on its recovery in mass-capacity storage demand, stronger pricing, and improving profitability.

Based on estimates of 21.9% annual revenue growth, 38.3% operating margins, and a normalized P/E multiple of 18.5x, the model projects Seagate stock could rise from $413 to $552 per share by June 2028.

That would be a 33.6% total return, or a 13.6% annualized return over the next 2.3 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for STX stock:

1. Revenue Growth: 21.9%

Seagate grew revenue 38.9% in fiscal 2025 to $9.1 billion, and LTM revenue in your TIKR data reached $10.1 billion. Fiscal Q2 2026 revenue was $2.83 billion, up from $2.33 billion a year earlier, and management guided Q3 revenue to about $2.90 billion. That supports a strong near-term growth backdrop, even if 21.9% annual growth is still a demanding assumption.

The main driver is data center demand for nearline drives, which are large-capacity hard drives used by cloud and hyperscale customers. Seagate’s management said AI applications are increasing the amount of data that must be stored economically at exabyte scale, and Reuters tied the company’s outlook beat to strong data storage demand. That gives the growth assumption a real operating basis.

At the same time, this is still a cyclical hardware business. Revenue was down 36.7% in fiscal 2023 and down 11.3% in fiscal 2024 before the rebound. So, the model assumes the current recovery continues, not that demand becomes permanently linear.

2. Operating Margins: 38.3%

Seagate’s LTM EBIT margin in your overview is 25.7%, while gross margin improved to 38.8%. In fiscal Q2 2026, non-GAAP operating margin reached 31.9%, up from 23.1% a year earlier, helped by pricing strategy, higher-capacity products, and stronger exabyte shipments. That shows margins are recovering fast as demand improves.

So the model’s 38.3% operating margin assumption is ambitious relative to the current operating margin, but it is directionally tied to a business already generating much better profitability. Fiscal 2025 operating income rose to $1.93 billion from $434 million in fiscal 2024, and LTM operating income reached $2.59 billion. The margin case depends on continued mix improvement and disciplined supply, not just unit growth.

Cash flow also supports the story. Seagate generated $723 million of operating cash flow and $607 million of free cash flow in fiscal Q2 2026, with LTM free cash flow of $1.68 billion. That matters because stronger margins are showing up in cash generation, not only in accounting earnings.

3. Exit P/E Multiple: 18.5x

Seagate is trading at about 24.8x NTM P/E and 46.6x LTM P/E, while the guided model uses an 18.5x exit multiple. That means the model is not relying on multiple expansions from the current forward valuation. Instead, it assumes the stock eventually trades at a more normalized earnings multiple as the cycle matures.

That looks reasonable because Seagate is still a hardware company with cyclical demand, leverage, and negative recent book value history, even though profitability has improved.

The balance sheet shows LTM net debt of $3.76 billion in your overview, and management also exchanged $600 million of exchangeable notes earlier this year. Those factors can limit how much valuation investors are willing to pay, even in a strong part of the cycle.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

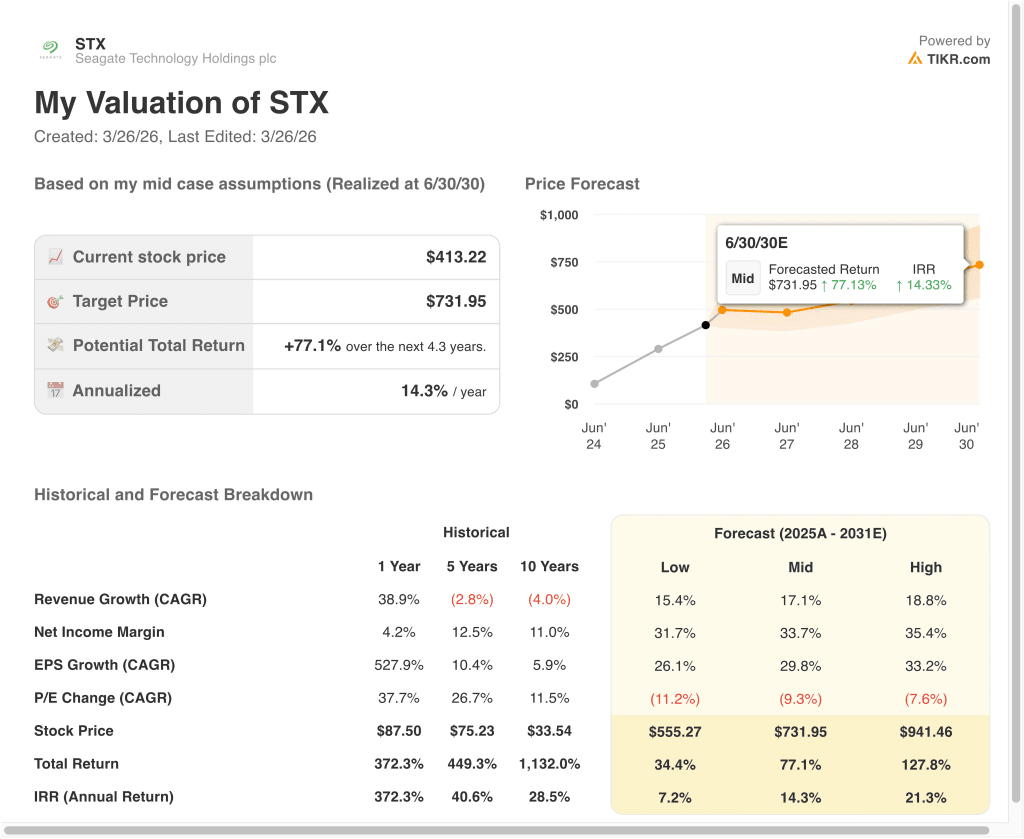

Different scenarios for STX stock through 2031 show varied outcomes based on AI storage demand, margin durability, and valuation levels (these are estimates, not guaranteed returns):

- Low Case: Data center demand cools, and margins normalize faster → 7.2% annual returns

- Mid Case: AI storage demand stays strong, and Seagate sustains better pricing and profitability → 14.3% annual returns

- High Case: Exabyte demand and HAMR adoption stay strong, and earnings compound faster → 21.3% annual returns

Even in the conservative case, STX stock offers positive returns supported by its improving margins, stronger cash flow generation, and AI-linked storage demand.

See what analysts think about STX stock right now (Free with TIKR) >>>

Should You Invest in Seagate Technology Holdings plc?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up STX, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track STX alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Seagate Technology stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!