Key Stats for Elastic Stock

- Past-Week Performance: +3.5%

- 52-Week Range: $48.7 to $98.3

- Current Price: $49.9

What Happened?

Elastic (ESTC) built its investment case on a single structural claim: enterprises cannot move petabytes of sensitive data to an AI model, so the model must come to the data, and ESTC crossed $1 billion in current remaining performance obligations for the first time in Q3, confirming that claim is now showing up in committed revenue, even as the stock sits 49% below its 52-week high of $98.25.

Elastic reported Q3 FY2026 results on February 26, with total revenue of $450 million beating the IBES consensus of $438.5 million, sales-led subscription revenue (contracts sold directly by the field sales team, the truest measure of commercial demand) accelerating to 21% growth, and adjusted EPS of $0.73 clearing the $0.65 consensus by 12%.

Driving that beat was CRPO of $1.055 billion, up 19%, alongside RPO growth of 22%, the strongest backlog expansion in two years, while over 470 customers in the company’s $100,000-plus annual contract value cohort now use Elastic for AI workloads, representing roughly 25% penetration of that high-value tier, a cohort the CFO confirmed consumes approximately 6% more compute than non-AI customers.

On March 2 at the Morgan Stanley Technology, Media and Telecom Conference, CEO Ashutosh Kulkarni stated that “the number of commitments for over $1 million in annual commitment value signed this quarter grew over 30% compared to the same period last year, driven by new logos and customer expansion,” directly tied to a 7-figure new logo win at a Fortune 100 insurance institution replacing a legacy SIEM (security information and event management, the software that centralizes and analyzes security alerts across an organization) with Elastic’s AI-powered cyber data lake.

Elastic’s elimination of per-endpoint pricing for Elastic Security XDR on March 23, combined with a $500 million buyback program already 60% deployed and a midterm FY2029 target of 20%-plus sales-led subscription revenue growth, positions the company to convert its AI infrastructure moat into durable compounding returns as the roughly 75% of its $100,000 ACV customer base that has not yet adopted AI workloads begins that journey.

Wall Street’s Take on ESTC Stock

The first CRPO print above $1 billion, combined with 21% sales-led subscription revenue growth, validates the AI context-engine thesis Elastic has been building toward, and the stock’s trajectory from here hinges on whether that backlog converts to accelerating consumption revenue.

Per TIKR estimates, Elastic’s revenue is set to sit at $1.73 billion in FY2026 and $1.97 billion in FY2027, supported by the 30%-plus growth in $1 million-plus annual commitment deals that directly feeds future consumption billings as enterprise workloads scale.

Elastic’s FCF margin stood at 17.7% in FY2025 and the TIKR model projects expansion to 19.3% in FY2027 and 20.8% in FY2028, driven by operating leverage already visible in Q3’s 18.6% non-GAAP operating margin.

Thirteen analysts rate ESTC a buy or strong buy, six rate it outperform, and nine hold, with zero sells; the mean price target of $82.13 implies 64.4% upside from the March 25 close of $49.94, a gap anchored in expectations of sustained sales-led subscription revenue compounding above 20%.

The analyst target range of $60.00 to $116.00 frames the binary precisely: the low end assumes AI penetration stalls near the current 25% of the $100,000 ACV cohort, while the high end prices full realization of the 75% of that cohort yet to adopt AI workloads.

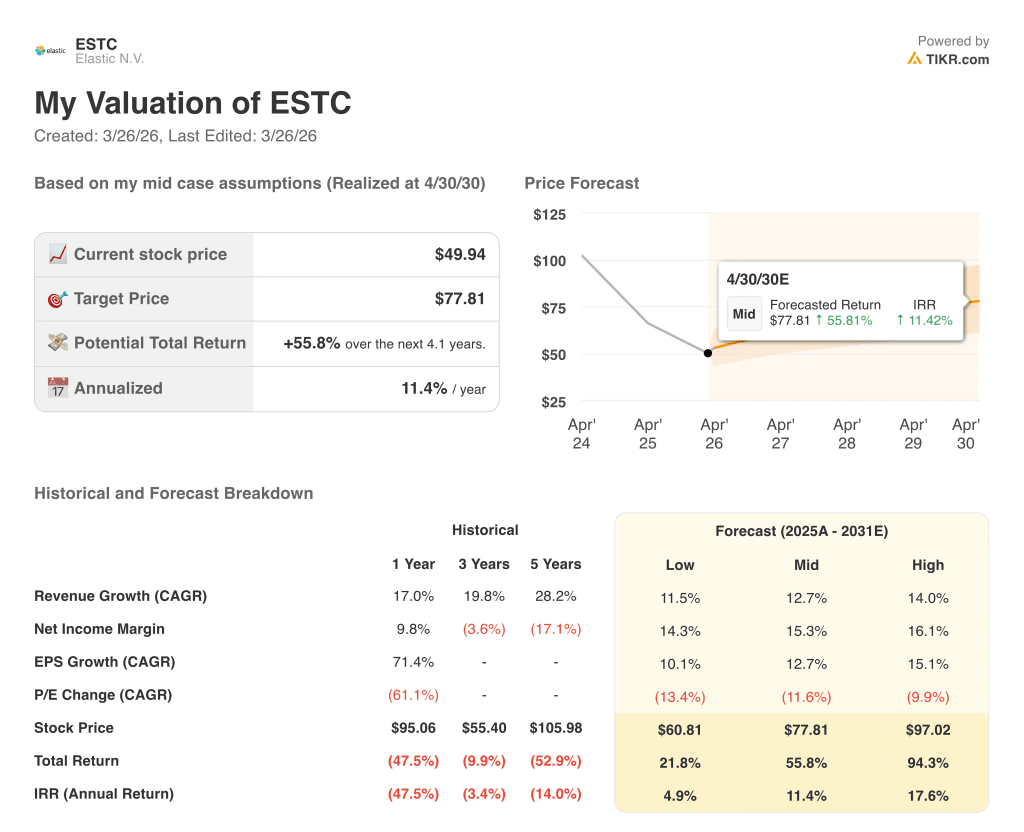

What Does the Valuation Model Say?

The TIKR mid-case price target of $77.81, reached by FY2030 on a 12.7% revenue CAGR and 15.3% net income margin, is grounded in the AI consumption uplift of approximately 6% that management quantified at the October Financial Analyst Day, a figure now tracking above that baseline per CFO commentary.

The market is pricing ESTC as though the 49% stock decline reflects business deterioration, yet CRPO and RPO just posted their fastest growth in two years.

The 60% completion of the $500 million buyback program, paired with FY2026 normalized EPS estimates of $2.53 rising to $2.83 in FY2027, confirms the capital return story is already executing, not aspirational.

The signal: AI customers inside the $100,000 ACV cohort already consume approximately 6% more compute on average, and that cohort is still roughly 75% unpenetrated, meaning the revenue uplift is structural, not a one-cycle event.

The risk: if Q4 sales-led subscription revenue misses the guided 18% midpoint growth, the TIKR model’s 12.7% revenue CAGR assumption breaks, and the $77.81 mid-case target loses its primary support.

The catalyst: Q4 FY2026 earnings in May, where the number to watch is sales-led subscription revenue against the $371–$373 million guidance range and whether AI penetration of the $100,000 ACV cohort crosses 30%.

Should You Invest in Elastic N.V.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ESTC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Elastic N.V. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ESTC stock on TIKR for Free →