Key Stats for AutoZone Stock

- Past-Week Performance: -7.9%

- 52-Week Range: $3,210.7 to $4,388.1

- Current Price: $3,396

What Happened?

AutoZone (AZO) reported Q2 earnings that exposed a widening gap between its operating strength and its reported financials, as a $59 million non-cash LIFO charge — an accounting adjustment that raises inventory costs during inflationary periods — compressed gross margin 137 basis points to 52.5% and pushed net income down 3.9% to $469 million, even as net sales climbed 8.1% to $4.3 billion and diluted EPS of $27.63 beat the IBES consensus of $27.13.

Just last March 4, Citigroup (C) raised its price target on AZO to $4,300 from $4,200, reiterating its “buy” rating and flagging that selling, general and administrative expenses — the retailer’s overhead and store-level cost base — had likely peaked, with the brokerage projecting EBIT and margin rate recovery beginning in FY2027 as the investment-heavy store expansion cycle matures.

Domestic commercial sales — parts sold to professional repair shops rather than individual car owners — also grew 9.8% to $1.2 billion and ran above 12% for ten of the quarter’s twelve weeks before severe winter storms shuttered roughly 200 to 400 stores and forced commercial accounts to close across a corridor stretching from Texas to Washington, D.C. in the final two weeks, dragging that segment’s weekly run rate down to just 1% growth during weeks ten and eleven.

CFO Jamere Jackson stated on the Q2 2026 earnings call that “excluding our noncash $59 million LIFO charge, EBIT would have grown 7.2% and EPS would have been up 7.1%,” directly quantifying how much the accounting headwind obscures underlying operating momentum.

AutoZone’s plan to reach 300 annual domestic store openings by FY2028, combined with a $1.6 billion CapEx program, 142 Mega-Hub locations (large-format stores carrying over 100,000 SKUs), and $1.4 billion remaining under its share repurchase authorization, positions the company to convert storm-disrupted commercial volume into durable share gains as the expanded store network matures and LIFO headwinds normalize.

Wall Street’s Take on AZO Stock

The LIFO distortion obscuring AZO’s operating momentum makes FY2027 the real inflection year: consensus already models EBIT recovering 12.7% to $4.13 billion as the non-cash inventory charge normalizes and 350 to 360 new stores begin maturing.

TIKR estimates project FY2026 revenue of $20.5 billion, reflecting 8.4% growth — credible given commercial sales ran above 12% for ten of Q2’s twelve weeks — while FY2027 normalized EPS of $174.7 implies 17.7% growth as SG&A deleverage reverses and the accelerated store cohort lifts per-store productivity.

Twenty-two analysts carry buy or outperform ratings against five holds and one underperform, with a mean price target of $4,225.38 implying 24.4% upside from the March 26 close of $3,395.97 — a consensus anchored on Citigroup’s thesis that SG&A has peaked and margin recovery begins in FY2027.

The spread between the $3,000 low and $4,800 high target spans 60%, with the bear case tied to LIFO charges and tariff cost pass-through stalling, while the bull case rests on commercial sales sustaining double-digit growth and the 142 Mega-Hub stores — large-format locations carrying over 100,000 parts SKUs — outperforming their pro forma models as management confirmed they are already doing.

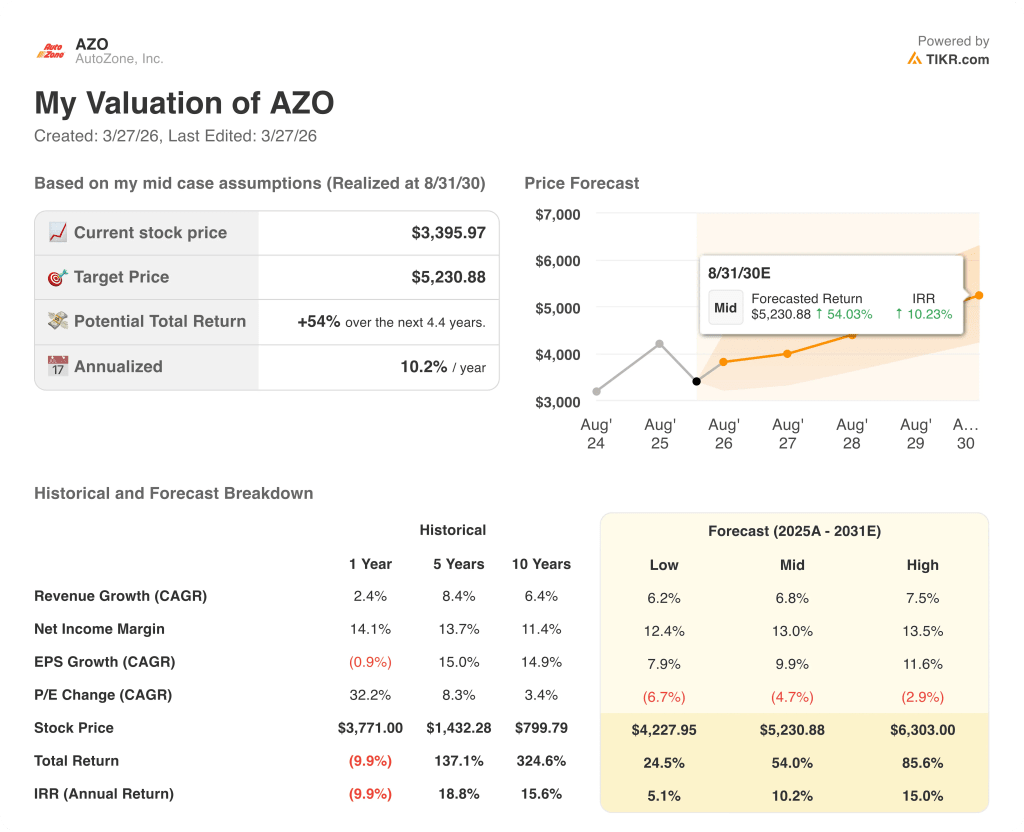

What Does the Valuation Model Say?

The TIKR mid-case target of $5,230.88 implies 54% total return over 4.4 years at a 10.2% IRR, driven by 6.8% revenue CAGR and 9.9% EPS CAGR, with multiple contraction of 4.7% annually already baked in — a deliberately conservative assumption given AZO currently trades at 24x forward earnings versus 25x three months ago.

The market is treating AZO’s 3.9% net income decline as structural deterioration, but strip the $59M non-cash LIFO charge and EBIT grew 7.2% — the operating business never contracted.

The TIKR model’s 10.2% IRR rests on FCF recovering from a $1.79 billion FY2025 trough to $2.06 billion in FY2026 and $2.22 billion in FY2027, consistent with management’s $1.6 billion CapEx cycle cresting as new distribution centers come online.

CFO Jamere Jackson’s signal that Q3 SG&A growth will moderate as prior-year store openings are lapped confirms the deleverage pressure is temporary, not a permanent reset of the cost structure.

Full-year LIFO charges of $277 million versus $64 million last year represent the single input that breaks the model if tariff costs accelerate beyond current 232-tariff assumptions and force further inventory revaluation beyond the guided $60 million per remaining quarter.

Q3 earnings — where commercial sales are already described as having “snapped back” and management guided 90 to 95 new store openings — will confirm whether EBIT ex-LIFO can sustain the 7%-plus growth rate that justifies the TIKR target; watch the SG&A per-store figure against Q2’s $3.9% reading.

Should You Invest in AutoZone, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AZO stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AutoZone, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AZO stock on TIKR for Free →