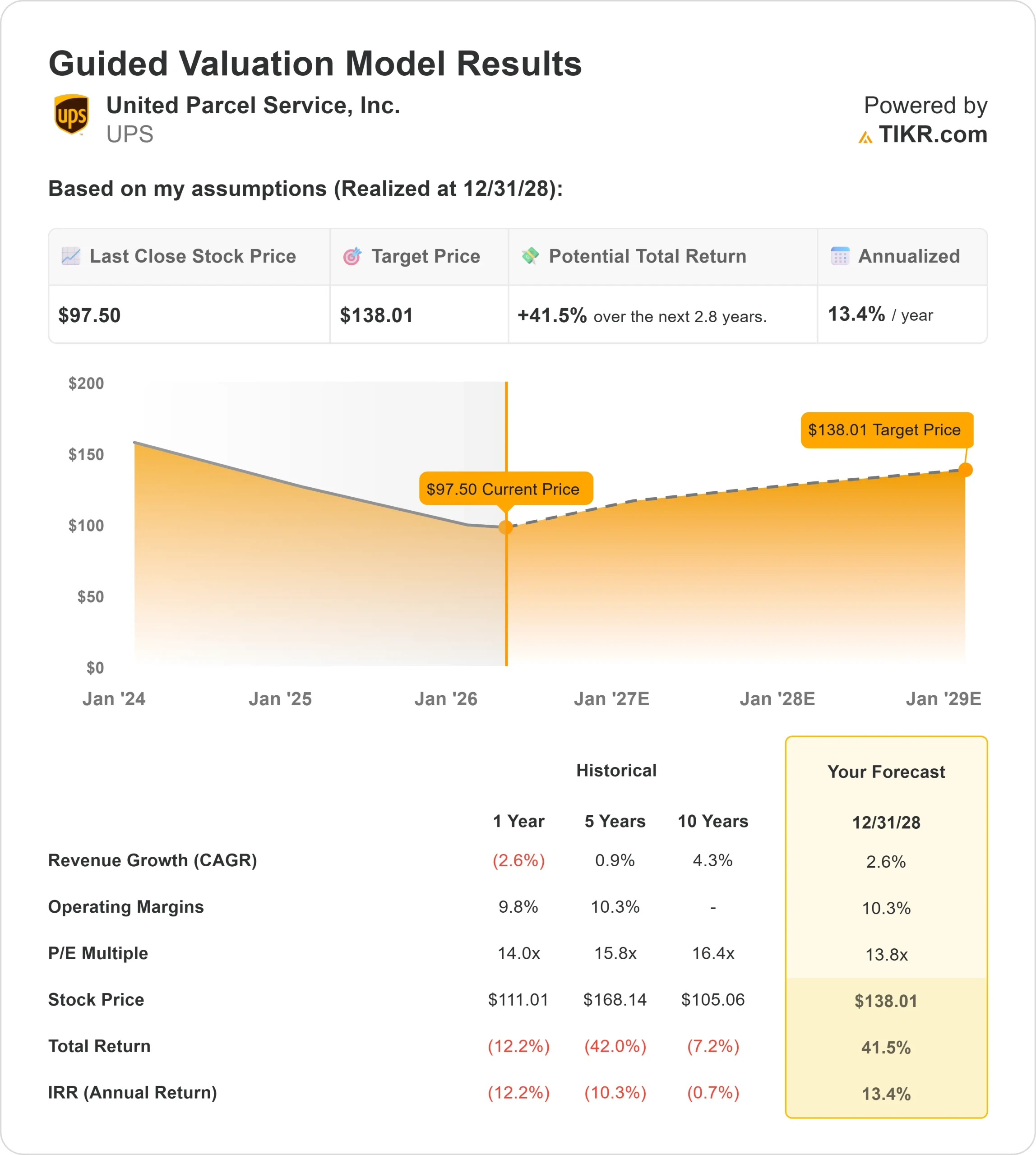

Key Stats for UPS Stock

- Past-30-Day Performance: -16%

- 52-Week Range: $82 to $122

- Valuation Model Target Price: $138

- Implied Upside: 42%

Analyze your favorite stocks like United Parcel Service with TIKR (It’s free) >>>

What Happened?

United Parcel Service stock fell about 16% over the past 30 days, finishing near $98 per share, as investors reacted to a major strategic reset in which the company is moving away from lower-margin Amazon-related volume and reshaping its network toward higher-quality, more profitable shipments, while peers like FedEx are also focusing on pricing discipline and network efficiency.

The stock declined primarily because investors are concerned that reducing Amazon-related volume and ongoing labor restructuring will pressure near-term revenue and margins, as UPS is intentionally removing lower-margin shipments while absorbing transition costs, creating a temporary gap between declining volumes and future margin improvement.

At a recent investor conference, UPS reiterated its 2026 outlook and highlighted the scale of its transformation, with CFO Brian Dykes stating the company will remove about 2 million Amazon-related packages per day over two years, or roughly $5 billion in revenue, while targeting $6.5 billion in free cash flow and guiding for about 1% revenue growth with flat EPS, adding that “we’ll see revenue up” as performance improves in the second half of the year.

Institutional activity showed active but mixed positioning, with Assenagon Asset Management increasing its stake by 155.9% to about 1.07 million shares worth roughly $106 million and Nordea Investment Management raising its holdings to about 4.28 million shares valued near $426 million, while other firms including Capital CS Group and Cooper Financial Group reduced exposure, reflecting a more balanced sentiment backdrop as investors weigh near-term execution risk against longer-term margin recovery potential.

Value United Parcel Service instantly (Free with TIKR) >>>

Is UPS Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 2.5%

- Operating Margins: 10.3%

- Exit P/E Multiple: 13.8x

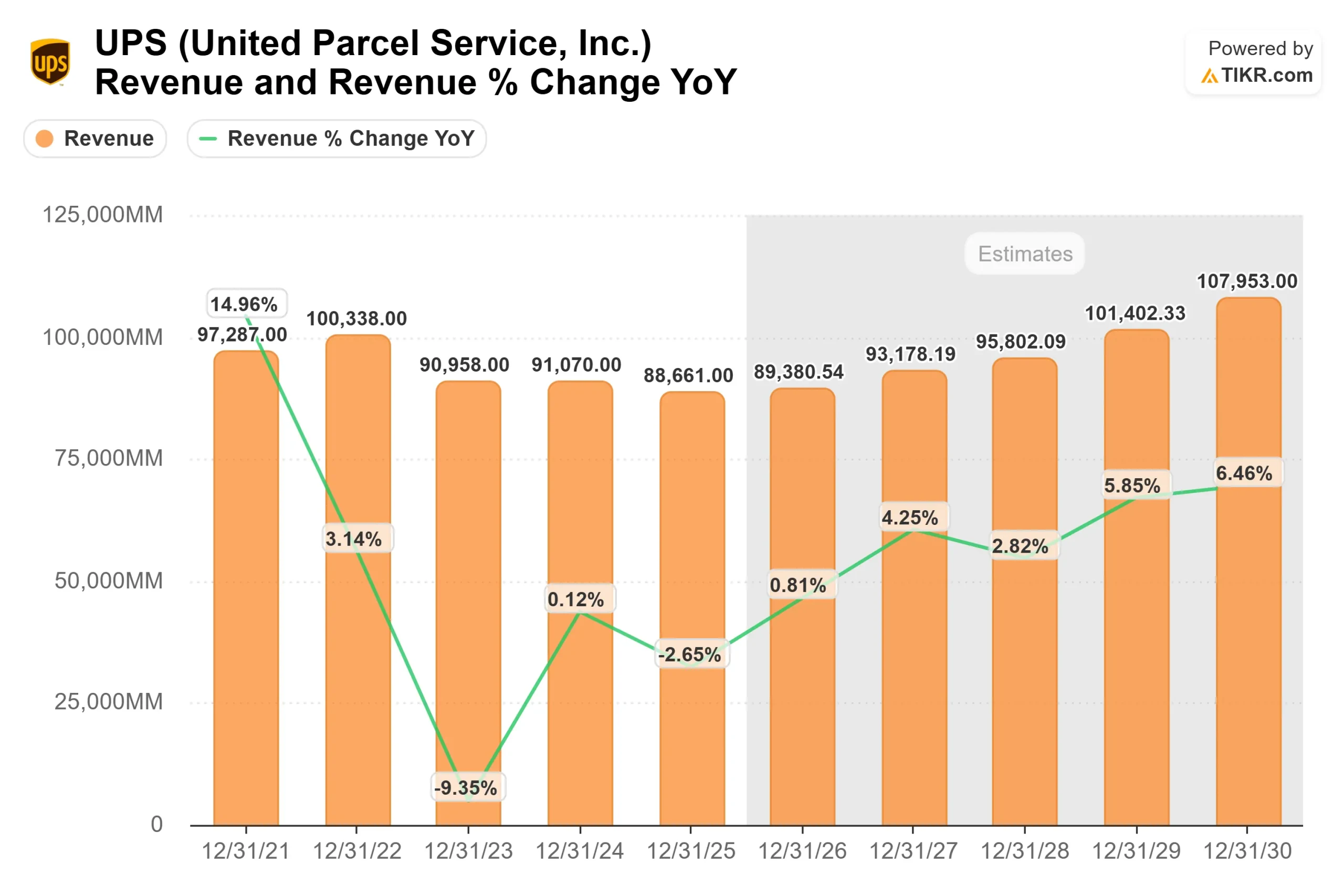

Revenue growth is expected to remain modest as UPS deliberately reduces lower-quality e-commerce shipments tied to Amazon while focusing on higher-value segments like small and medium-sized businesses, which tend to ship more frequently at better pricing, and healthcare logistics, where time-sensitive deliveries such as medical products require premium service and support higher margins.

See analysts’ growth forecasts and price targets for United Parcel Service (It’s free) >>>

Margins are likely to improve gradually as automation, network optimization, and a more favorable shipment mix offset labor cost pressures, though this depends on execution during the current restructuring period.

This shift toward higher-quality revenue rather than pure volume growth is central to the investment case, as it supports stronger pricing power and more stable long-term profitability even if near-term results remain uneven.

The competitive landscape reinforces this strategy, as peers like FedEx are also prioritizing pricing discipline, cost control, and network efficiency, suggesting a more rational industry environment over time.

Based on these inputs, the model estimates a target price of $138, implying about 42% total upside over the next 2.8 years, suggesting the stock appears undervalued if UPS can successfully execute its transition and restore margin expansion.

Performance this year will depend on how quickly volumes stabilize, how effectively UPS manages labor and restructuring costs, and whether pricing and mix improvements translate into stronger earnings in the second half of 2026.

At current levels, UPS appears undervalued, with future returns driven by margin recovery, improved shipment mix, and pricing discipline rather than a rapid rebound in shipping volumes.

How Much Upside Does UPS Stock Have From Here?

Investors can estimate United Parcel Service potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value United Parcel Service in under 60 seconds with TIKR (It’s free) >>>