Key Takeaways:

- Vertiv is one of the clearest public-market ways to play AI data center buildouts, and that theme is driving both its growth and its premium valuation.

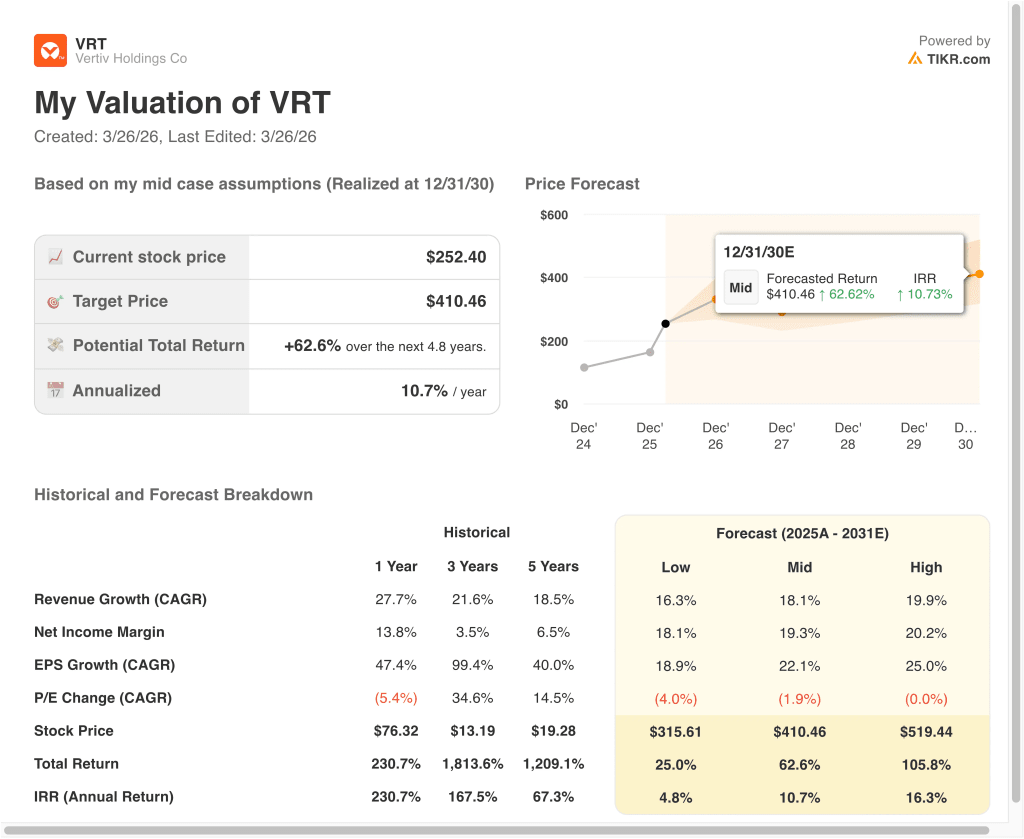

- VRT stock could reasonably reach $410 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 62.6% from today’s price of $252, with an annualized return of 10.7% over the next 4.8 years.

What Happened?

Vertiv Holdings Co (VRT) has become one of the market’s favorite AI infrastructure stocks because it sells the physical systems that keep modern data centers running. That includes power equipment, cooling systems, racks, and integrated infrastructure used in high-density AI deployments. The stock is up 57.3% year to date in 2026 based on the attached overview, so investors are clearly pricing in more AI-related demand and execution strength.

The story accelerated after S&P Dow Jones Indices said Vertiv would join the S&P 500 effective before the open on March 23, 2026. Reuters reported the shares jumped nearly 6% in extended trading after that announcement, which makes sense because index inclusion can force passive funds to buy the stock. That helped reinforce the idea that Vertiv has moved from an AI trade into a large-cap benchmark name.

Recent company news has also supported that narrative. On March 24, Vertiv said it would acquire ThermoKey to expand heat rejection and heat-exchange capabilities for AI-ready data centers, and on the same day, it announced four new or expanded manufacturing facilities in the Americas to increase capacity for infrastructure solutions, power management, and integrated cabinets.

The company has also kept building around NVIDIA’s ecosystem and around faster deployment models. Vertiv said on March 16 that it is contributing converged physical infrastructure designs for NVIDIA Vera Rubin DSX AI factories, and on March 4, it announced a collaboration with Generate Capital to offer power and cooling infrastructure in grid-constrained U.S. markets. Investors seem excited by that positioning, but the stock’s rich valuation also shows the market already expects a lot of this demand to convert into revenue and margins.

What the Model Says for VRT Stock

We analyzed the upside potential for Vertiv stock using valuation assumptions based on its exposure to AI data center power and cooling demand, improving margins, and strong order momentum.

Based on estimates of 18.1% annual revenue growth, 19.3% net income margins, and a path to $410 per share by 2030 in the mid case, the model suggests Vertiv could generate a 62.6% total return from $252. That works out to a 10.7% annualized return over the next 4.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for VRT stock:

1. Revenue Growth: 24%

Vertiv’s revenue growth has accelerated sharply over the last five years. Sales rose from $5.0 billion in 2021 to $10.2 billion in 2025, and revenue increased 27.7% in 2025 alone. That tells you the business is no longer just recovering margins, because it is now also scaling into a much larger demand environment.

The latest earnings release showed that demand is still outrunning supply in several parts of the business. Vertiv reported fourth-quarter 2025 sales of $2.88 billion, up 23% year over year, while fourth-quarter organic orders rose about 252% and backlog climbed to $15.0 billion, up 109% from a year earlier. CEO Giordano Albertazzi said, “Our record backlog provides clear visibility into what we expect to be another year of significant growth.”

A 24.0% revenue growth assumption is aggressive, but it is grounded in the company’s current order profile and in management’s 2026 outlook. Vertiv guided for 2026 net sales of $13.25 billion to $13.75 billion, with 27% to 29% organic sales growth, and it is adding manufacturing capacity to support that demand. That helps explain why the model can justify meaningful long-term appreciation even after the stock’s big run.

2. Operating Margins: 20%

Vertiv’s margin story is one of the biggest reasons the stock has rerated. Operating margin improved from 5.5% in 2021 to 18.6% in 2025, while gross margin expanded from 30.5% to 36.3% over the same span. That means the company is not just selling more equipment, because it is also doing so more profitably.

Recent results suggest there could still be room for more improvement. In fourth-quarter 2025, adjusted operating margin reached 23.2%, up 170 basis points from a year earlier, driven by higher volume, productivity, and favorable price-cost. The business is also generating much stronger cash now, with a 2025 operating cash flow of $2.11 billion and free cash flow of $1.89 billion.

A 20.0% operating margin assumption looks demanding, but it is not disconnected from the current trajectory. Vertiv is benefiting from higher-value AI deployments, and those projects often need integrated power, cooling, and service offerings rather than standalone hardware. If that mix continues shifting toward more complex solutions, margin expansion can remain part of the story even as revenue grows.

3. Exit P/E Multiple: 29.4x

The exit multiple is where the article becomes more balanced. The attached guided model uses a 29.4x P/E multiple, which is below Vertiv’s current LTM P/E of 74.0x and also below its NTM P/E of 41.1x from the overview screenshot. In other words, the model already assumes some multiple normalization as the business matures.

That lower exit multiple seems reasonable because Vertiv is still an industrial company, even if it has become one of the market’s preferred AI infrastructure names. Also, data shows a historical P/E multiple of 33.2x over one year, 24.5x over three years, and 23.1x over five years. So using 29.4x does not require the market to stay as euphoric as it is today, but it does require investors to keep paying a premium for growth and execution.

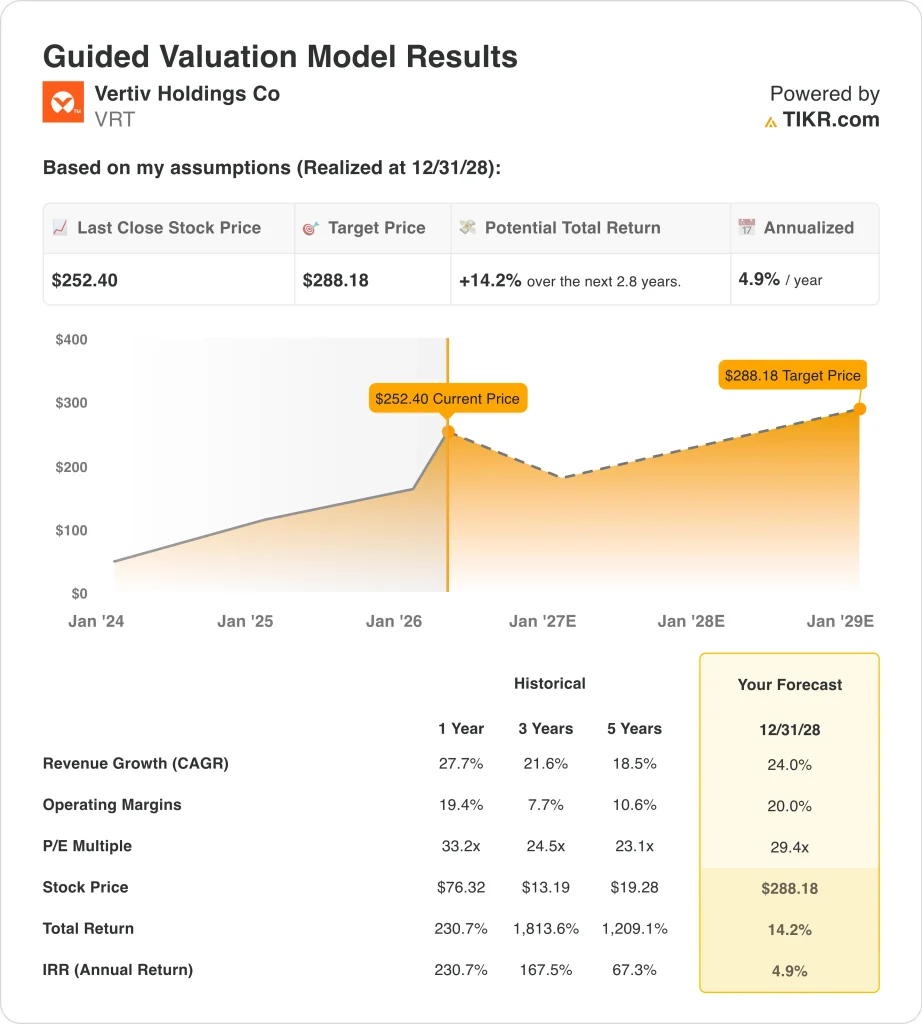

The multiple discussion also connects directly to the stock’s current behavior. Vertiv keeps winning attention because of AI demand, S&P 500 inclusion, and product announcements, but the valuation leaves less room for error if growth slows. That is why the shorter model only points to a 4.9% annualized return through 2028, even with strong operating assumptions.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for VRT stock through 2030 show varied outcomes based on AI infrastructure demand, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI data center spending cools, and valuation compresses faster → 4.8% annual returns

- Mid Case: Vertiv keeps scaling power and cooling solutions across AI deployments → 10.7% annual returns

- High Case: Orders, margins, and AI factory adoption remain exceptionally strong → 16.3% annual returns

Even in the conservative case, Vertiv stock still offers positive returns because the business is generating real cash, expanding manufacturing capacity, and carrying lower leverage than it did a few years ago.

The balance sheet has improved, with net debt down to $1.38 billion at year-end 2025, while 2025 free cash flow reached $1.89 billion. That gives the company more flexibility to invest in growth while still paying a dividend and pursuing acquisitions.

Going forward, the stock will probably keep moving with AI infrastructure sentiment, quarterly order data, and signs that Vertiv can convert backlog into profitable revenue.

If management keeps expanding capacity, integrating acquisitions, and landing large AI-related deployments, investors may stay willing to pay a premium for the shares. But if revenue growth slows or the market derates AI-exposed industrial names, the valuation could compress even if the underlying business remains healthy.

See what analysts think about VRT stock right now (Free with TIKR) >>>

Should You Invest in Vertiv Holdings Co?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VRT, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track VRT alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Vertiv stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!