Key Takeaways:

- Arista Networks is benefiting from accelerating AI-driven data center demand, with revenue reaching $9.0 billion and growing 28.6% year-over-year.

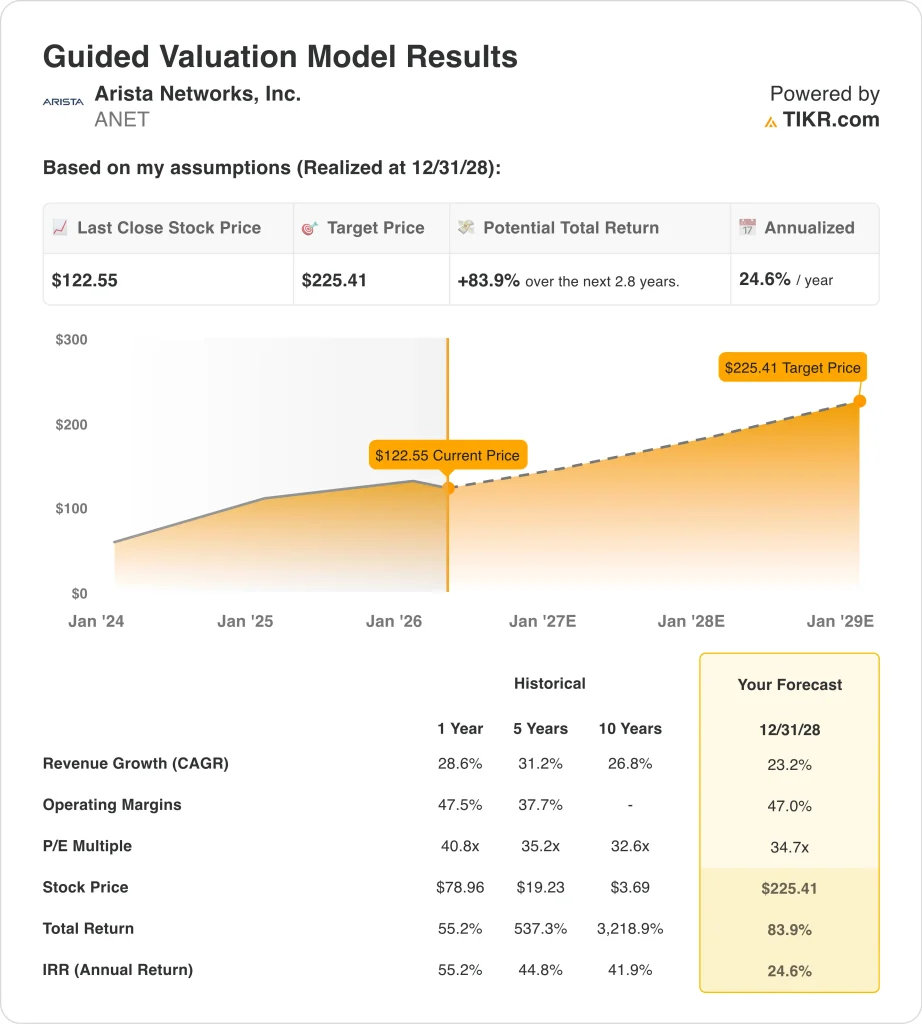

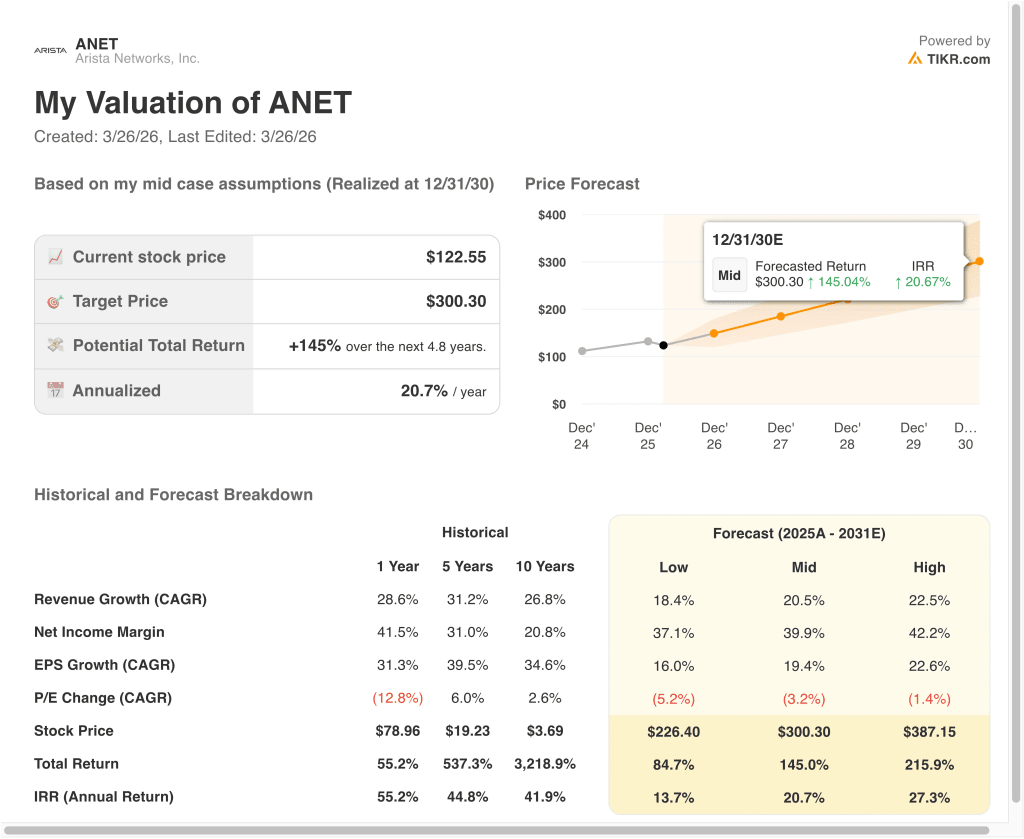

- ANET stock could reasonably reach $300 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 145.0% from today’s price of $122, with an annualized return of 20.7% over the next 4.8 years.

What Happened?

Arista Networks (ANET) has been in focus following strong Q4 2025 results, where the company reported adjusted EPS of $0.82, beating estimates of $0.76. Revenue reached $2.49 billion, up 28.9% year-over-year, driven by demand from AI infrastructure and cloud networking. Investors initially reacted positively because AI-related spending continues to expand across hyperscalers.

However, the stock has recently pulled back, declining about 9.2% on March 26, 2026, reflecting broader volatility in technology stocks. Even though inflation data cooled and markets stabilized, investors rotated away from high-multiple tech names. This suggests that valuation concerns, rather than fundamentals, are influencing near-term price action.

At the same time, Arista continues to position itself at the center of AI networking innovation. The company announced its XPO optics MSA initiative, targeting high-speed 12.8 Tbps networking solutions with liquid cooling. This matters because AI workloads require faster, more efficient data movement, and Arista is building products specifically for that shift.

There has also been notable insider selling activity in March 2026, including share disposals by executives and directors. While these transactions can raise caution, they are relatively common in high-performing tech companies and do not necessarily signal deteriorating fundamentals. Instead, investors appear to be balancing strong growth with elevated valuation multiples.

What the Model Says for ANET Stock

We analyzed the upside potential for Arista Networks stock using valuation assumptions based on its leadership in AI networking, strong operating margins, and consistent revenue growth.

Based on estimates of 20.5% annual revenue growth, 47.0% operating margins, and a normalized P/E multiple of 34.7x, the model projects ANET stock could rise from $122 to $300 per share.

That would represent a 145.0% total return, or a 20.7% annualized return over the next 4.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ANET stock:

1. Revenue Growth: 20.5%

Arista Networks has delivered consistent revenue expansion, growing from $2.9 billion in 2021 to $9.0 billion in 2025. This reflects strong adoption of cloud networking solutions and increasing enterprise demand for high-performance infrastructure.

Growth is being driven by AI-related workloads, which require faster data transfer and scalable networking architectures. Hyperscalers and cloud providers are expanding their infrastructure, and Arista is a key supplier in this ecosystem.

The 20.5% assumption reflects continued AI-driven demand but also acknowledges potential moderation as the company scales. It aligns closely with forward estimates while recognizing the cyclical nature of enterprise spending.

2. Operating Margins: 47%

Arista has steadily improved profitability, with operating margins expanding from 31.4% in 2021 to 42.8% in 2025. This reflects strong pricing power, efficient operations, and a high-margin software-driven model.

The company benefits from its Extensible Operating System (EOS), which creates recurring value and reduces reliance on hardware margins alone. This software layer enhances customer stickiness and supports premium pricing.

The 47.0% assumption reflects continued efficiency gains and scale advantages, especially as AI networking products command higher margins. However, it also accounts for ongoing investment in R&D and innovation.

3. Exit P/E Multiple: 34.7x

Arista currently trades at a forward P/E in the mid-30s range, reflecting strong growth expectations and leadership in AI networking infrastructure. Its valuation is higher than traditional networking peers but justified by superior growth and margins.

Compared to historical levels, the multiple remains elevated but consistent with high-quality growth companies. Investors are willing to pay a premium for businesses benefiting from structural trends like AI and cloud computing.

The 34.7x multiple assumes that Arista maintains its competitive position and continues delivering strong financial performance. It balances growth potential with the risk of multiple compressions.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for ANET stock through 2030 show varied outcomes based on AI adoption and enterprise spending trends (these are estimates, not guaranteed returns):

- Low Case: Growth slows, and valuation compresses → 13.7% annual returns

- Mid Case: AI demand sustains strong growth → 20.7% annual returns

- High Case: Accelerated AI adoption and margin expansion → 27.3% annual returns

Even in the conservative case, Arista Networks’ stock offers positive returns supported by strong revenue growth, high margins, and a net cash position of -$10,652.5 million. The company’s balance sheet strength and free cash flow generation provide flexibility for continued investment and shareholder returns.

Going forward, ANET stock will likely remain tied to how investors weigh Arista’s AI-driven revenue growth against its still-premium valuation. If the company continues to execute on hyperscaler demand, margin expansion, and new AI networking products, the stock could keep tracking higher over time even if volatility stays elevated.

But if AI spending slows, customer concentration becomes a bigger concern, or the market keeps compressing tech multiples, the shares could remain choppy despite strong underlying fundamentals.

See what analysts think about ANET stock right now (Free with TIKR) >>>

Should You Invest in Arista Networks?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ANET, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ANET alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Arista Networks stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!