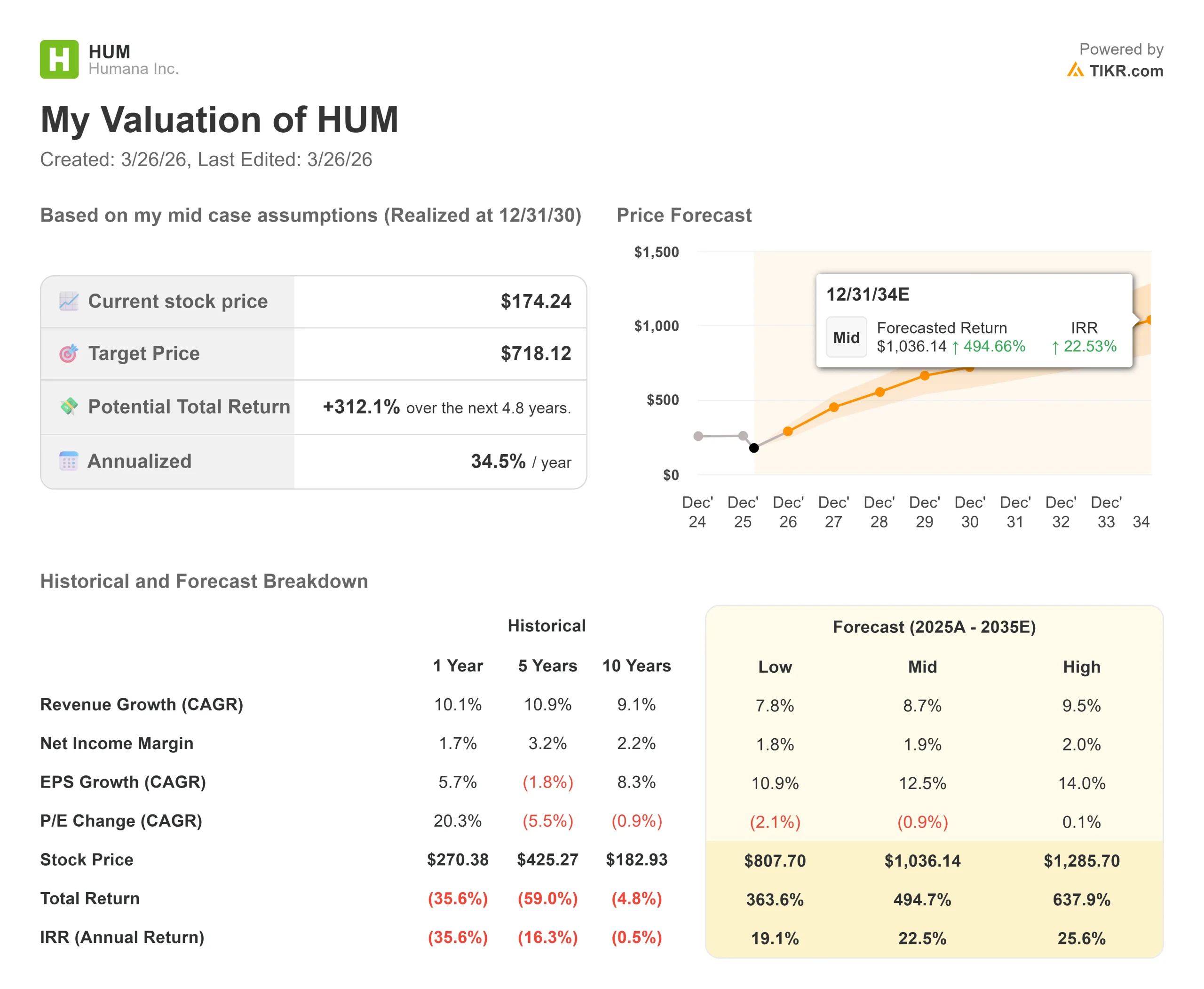

Key Stats for Humana Stock

- Current Price: $174

- Target Price: $718

- Street Target: $212.17

- Potential Total Return: +312.1%

- Annualized IRR: 34.5%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The Medicare Advantage (MA) sector is currently enduring one of its most challenging operating environments in recent memory, culminating in Humana Inc. (HUM) suffering a severe 47.54% maximum drawdown by mid-March 2026.

A brutal combination of mid- to high-single-digit medical cost trends and essentially flat government funding has forced the entire industry to rapidly adjust its benefit structures.

At the Leerink Global Healthcare Conference on March 10, 2026, Humana CEO Jim Rechtin and CFO Celeste Mellet addressed this turbulence head-on, reiterating their commitment to restoring the MA business to a compelling 3% margin and regaining full earnings power by 2028.

Instead of chasing unprofitable volume growth, Humana is fundamentally changing how it acquires and manages its members.

The new strategy is anchored on the “lifetime value” of an enrollee.

CFO Celeste Mellet bluntly explained the flawed economics of the industry’s historical churn: acquisition costs for a new member are massive, averaging over $1,000 in the first year, before dropping by half in the second year.

Furthermore, the Medical Expense Ratio (MER) naturally improves in year two and beyond as Humana’s care teams better understand and manage a member’s chronic conditions.

By cutting ties with low-performing call centers and broker partners, Humana aims to stop enriching third parties with churn commissions and start retaining profitable, long-term members.

“The economic value of [a member] in year 2 is substantially better than year 1… when we talk about lifetime value, what we’re talking about is the economic incentive to make sure that we are minimizing attrition,” Rechtin explained.

The early data from the Annual Enrollment Period (AEP) suggest the strategy is working.

Humana added over 1 million members, with an impressive 70% categorized as “switchers” from other plans rather than new-to-Medicare enrollees.

More importantly, 70% of these new members are in highly-rated 4-star or better contracts, and 75% were acquired through high-quality sales channels.

Beyond the core MA business, Humana continues to fortify its primary care footprint.

Management discussed filling geographic gaps in the Southeast by acquiring high-performing risk-bearing groups.

This was verified in reality on February 13, 2026, when Humana’s CenterWell division officially closed its acquisition of MaxHealth, bringing an additional 82 Florida clinics and 120,000 patients into its value-based care network.

See historical and forward estimates for Humana stock (It’s free!) >>>

Is Humana Undervalued Today?

The intense regulatory and funding pressures from CMS (Centers for Medicare & Medicaid Services) have created extreme pessimism around Humana, depressing the stock price to $174.24.

However, for investors willing to look past the current legislative headwinds, the valuation presents a highly asymmetric risk/reward profile.

Looking at the standalone valuation data from TIKR, Humana currently trades at a highly compressed NTM EV/EBITDA multiple of 10.90x and an NTM P/E of 18.63x.

This reflects a heavily discounted valuation for a company that typically commands a premium as a pure-play Medicare Advantage leader.

The market’s fear is currently priced around the upcoming final CMS rate notice and ongoing “unlinked chart review” policies (a CMS compliance initiative ensuring that billed conditions match actual patient encounter data).

Rechtin acknowledged the difficult math of the preliminary rule, noting, “You can’t have mid- to high single-digit cost trend and flat funding and expect benefits to remain the same.”

However, because this is an industry-wide crisis, Humana is using the moment to structurally improve its risk pool.

If the final CMS rates provide even a modest amount of relief, Humana’s disciplined pricing and upgraded membership mix could trigger a massive re-rating toward the $212.17 Street Target.

Analyze historical valuation multiples for HUM (It’s free!) >>>

The TIKR Model Analysis

The TIKR Advanced Model calculates the long-term impact of Humana successfully executing its 3% MA margin recovery plan and scaling its CenterWell clinics by 2028.

- Current Price: $174

- Target Price: $718

- Potential Total Return: +312.1%

- Annualized IRR: 34.5%

Build a 4-year Valuation Model for HUM for yourself (It’s free) >>>

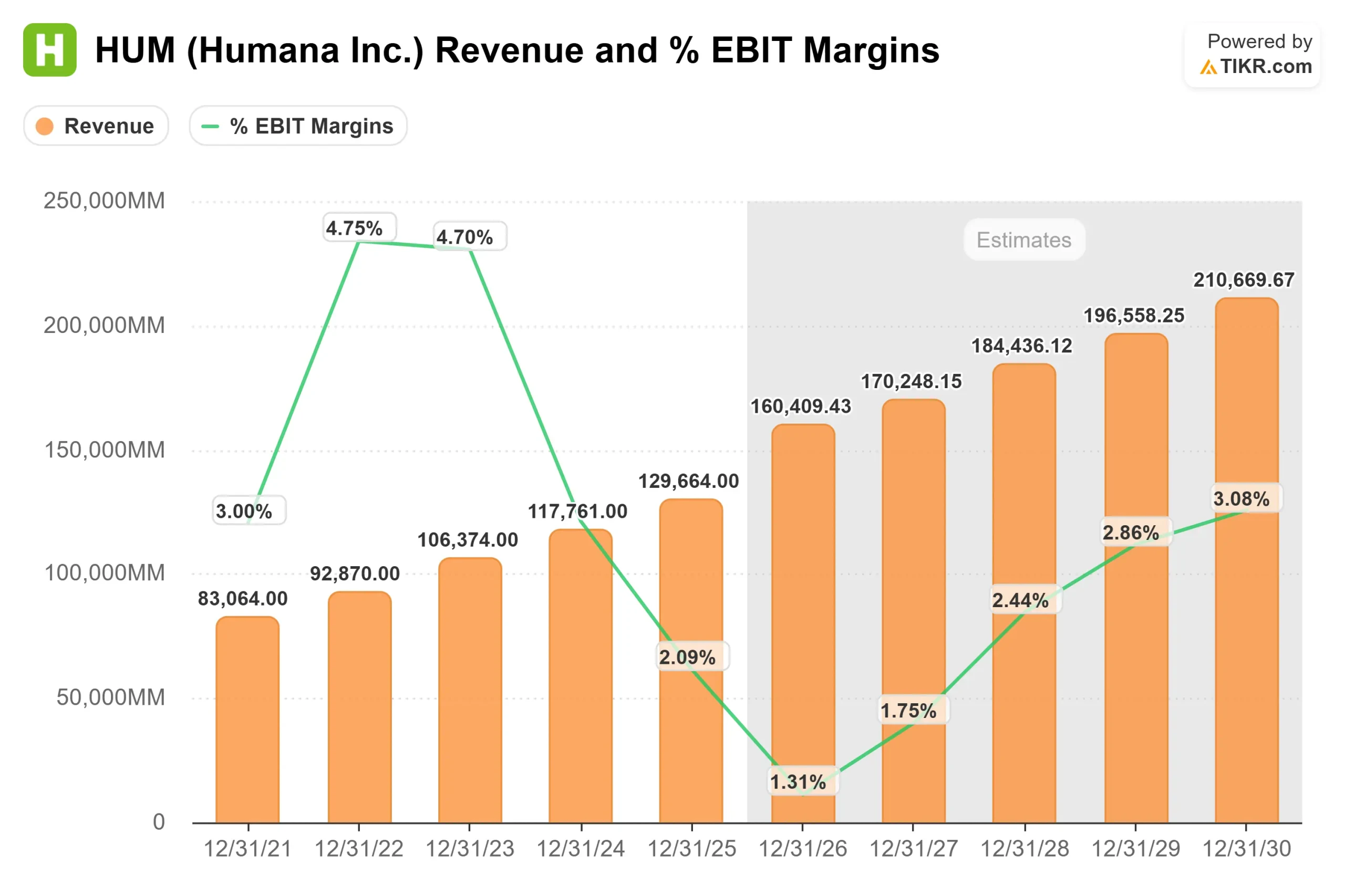

The Mid Case projection issues an incredibly bullish $718.12 target price, which requires Humana to compound at a 34.5% Annualized IRR over the next 4.8 years. The engine of this valuation is a solid 8.7% Revenue CAGR through 2035, driven by the structural aging of the U.S. population and the steady expansion of the CenterWell primary care footprint.

However, the true catalyst for this 312% upside is margin restoration. The model assumes Humana will pull its Net Income Margins back up to a normalized 1.9%. To achieve this, Humana must flawlessly execute its retention strategy. If the company can slash its $1,000+ year-one acquisition costs by keeping switchers engaged through its high-quality 4-star plans, the resulting “lifetime value” economics will drop straight to the bottom line. For investors with the patience to weather the 2026 CMS storm, Humana offers one of the most compelling turnaround opportunities in the healthcare sector.

Conclusion: Humana is operating in a deeply distressed Medicare Advantage environment, leading to a brutal 47% drawdown. Yet, beneath the grim regulatory headlines, the company is fundamentally upgrading its membership base, retaining profitable switchers, and aggressively expanding its CenterWell clinics via the MaxHealth acquisition. With the stock battered down to $174, the TIKR Mid Case model points to an extreme dislocation between current panic and future earnings power. If management can successfully stabilize MA margins at 3% by 2028, the mathematically sound path to the $718 target makes Humana a prime contrarian buy.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Humana?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Humana, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Humana alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!