Key Takeaways:

- CAVA is getting attention because revenue is still growing above 20%, unit expansion remains fast, and same-restaurant sales stayed positive, but investors are also weighing margin pressure and a very rich valuation.

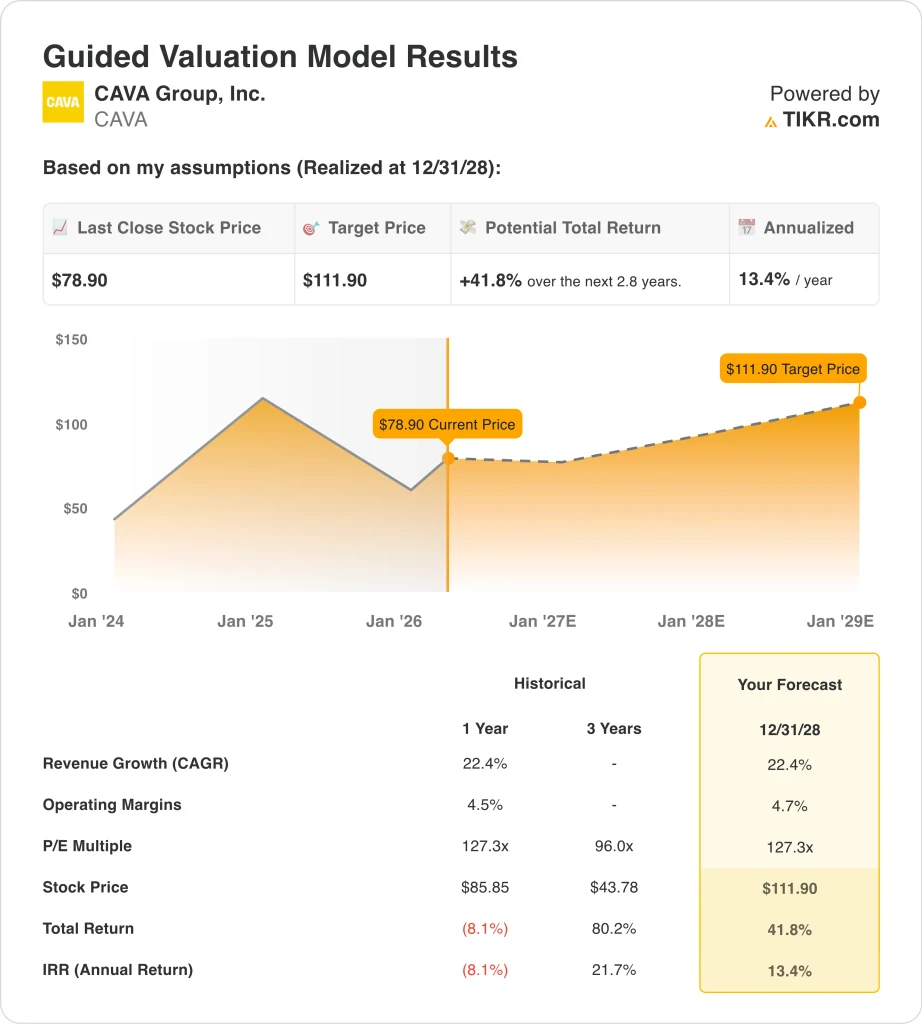

- CAVA stock could reasonably reach $112 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 41.8% from today’s price of $79, with an annualized return of 13.4% over the next 2.8 years.

What Happened?

CAVA Group, Inc. (CAVA)’s latest move was driven first by its February earnings report. Reuters reported the stock rose about 8% in extended trading after the company posted a surprise 0.5% increase in fourth-quarter same-store sales, while also forecasting 2026 same-restaurant sales growth of 3% to 5%, above consensus.

The details underneath the release help explain why sentiment stayed constructive. For fiscal 2025, CAVA crossed $1 billion in annual revenue for the first time, opened 72 net new restaurants, ended the year with 439 locations, and generated adjusted EBITDA of $152.8 million.

CEO Brett Schulman said, “For the first time in our history, revenue surpassed $1 billion for a full fiscal year in 2025,” and he added that “the power of our model and the momentum of our brand remain clear.”

The stock is also moving on expansion signals beyond the earnings release. CAVA opened its first Ohio restaurant in Cincinnati in March, and Reuters also reported that the company amended its credit agreement to extend the maturity to March 20, 2031, and increase revolving commitments to $150 million from $75 million.

Investors are still balancing that growth story against valuation and cost pressure. Reuters reported Argus downgraded the stock to hold on valuation concerns two days after earnings, even as restaurant demand remained resilient. The next key event is the company’s expected first-quarter 2026 report on May 12, which should show whether traffic, menu pricing, and new store openings are still supporting growth at the pace the market is pricing in.

Here’s why CAVA stock could continue to move sharply as investors weigh strong restaurant expansion and positive same-store sales against margin pressure and a still-demanding earnings multiple.

What the Model Says for CAVA Stock

We analyzed the upside potential for CAVA stock using valuation assumptions based on continued restaurant expansion, positive same-restaurant sales, and modest margin improvement from current levels.

Based on estimates of 22.4% annual revenue growth, 4.7% operating margins, and a normalized P/E multiple of 127.3x, the model projects CAVA stock could rise from $78.90 to $111.90 per share.

That would be a 41.8% total return, or a 13.4% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CAVA stock:

1. Revenue Growth: 22.4%

CAVA has been one of the fastest-growing public restaurant companies, and the financials show that clearly. Revenue grew from $728.7 million in 2023 to $963.7 million in 2024 and then to $1.18 billion in 2025. That matters because the company is not relying on one single lever, since both unit growth and same-restaurant sales have contributed to the top line.

The key revenue drivers are new restaurant openings, guest traffic, menu price, and digital ordering. In fiscal 2025, CAVA opened 72 net new restaurants and ended the year with 439 locations, while same-restaurant sales increased 4.0% and digital revenue mix remained high at 37.9%.

Based on analysts’ consensus estimates, we used a 22.4% forecast. That assumption matches the guided valuation model and sits close to the company’s recent growth pace, though it is a little below the 32.3% growth CAVA posted in 2024 and roughly in line with the 22.5% growth posted in 2025.

In practical terms, the model assumes CAVA can keep opening stores and growing sales briskly, but not at the unusually strong pace seen earlier in its public market story.

2. Operating Margins: 4.7%

CAVA’s margins have improved a lot from the losses it posted before becoming consistently profitable. Operating margin moved from -8.4% in 2021 and -6.0% in 2022 to 2.2% in 2023 and 5.1% in both 2024 and 2025. That progression shows the business has gained scale, but it also shows margins are still relatively thin for a stock trading at a premium multiple.

There is also a difference between restaurant-level margin and corporate operating margin, and that matters for valuation. CAVA’s fiscal 2025 restaurant-level profit margin was 24.4%, but that figure came under pressure from higher food, beverage, packaging, tariff, delivery, and wage costs. Because the company is still investing in growth, not all of that restaurant’s profitability drops to operating income for shareholders.

Based on analysts’ consensus estimates, we use 4.7% operating margins. That is slightly below the 5.1% operating margin the company posted in 2025, which makes this assumption fairly measured rather than aggressive.

The model is effectively saying CAVA can keep growing fast, but some of that benefit will still be offset by labor, commodity, and new-unit costs as the chain expands.

3. Exit P/E Multiple: 127.3x

The valuation multiple is the most debated part of the CAVA story. The terminal overview shows the stock trading at an LTM P/E of 146.1x, while the model uses a normalized P/E multiple of 127.3x. That is still very high in absolute terms, but it is below the current trailing multiple, so the model already assumes some valuation discipline rather than a further expansion in sentiment.

That premium multiple reflects what investors think they are buying. CAVA is still early in its national expansion, it has a healthier fast-casual brand position, and it has delivered strong recent revenue growth with improving profitability.

But high multiples also make the stock more sensitive to any slowdown in traffic, same-restaurant sales, or margins, which is why the shares fell after an Argus downgrade that focused on valuation, even though the underlying business update was solid.

Based on analysts’ consensus estimates, we maintain a 127.3x exit multiple. That assumption fits a stock that is still being valued more on future unit growth and earnings compounding than on present-day margin strength.

It also means the model’s return potential depends heavily on CAVA continuing to execute, because a weaker growth outlook would likely pressure the multiple first.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

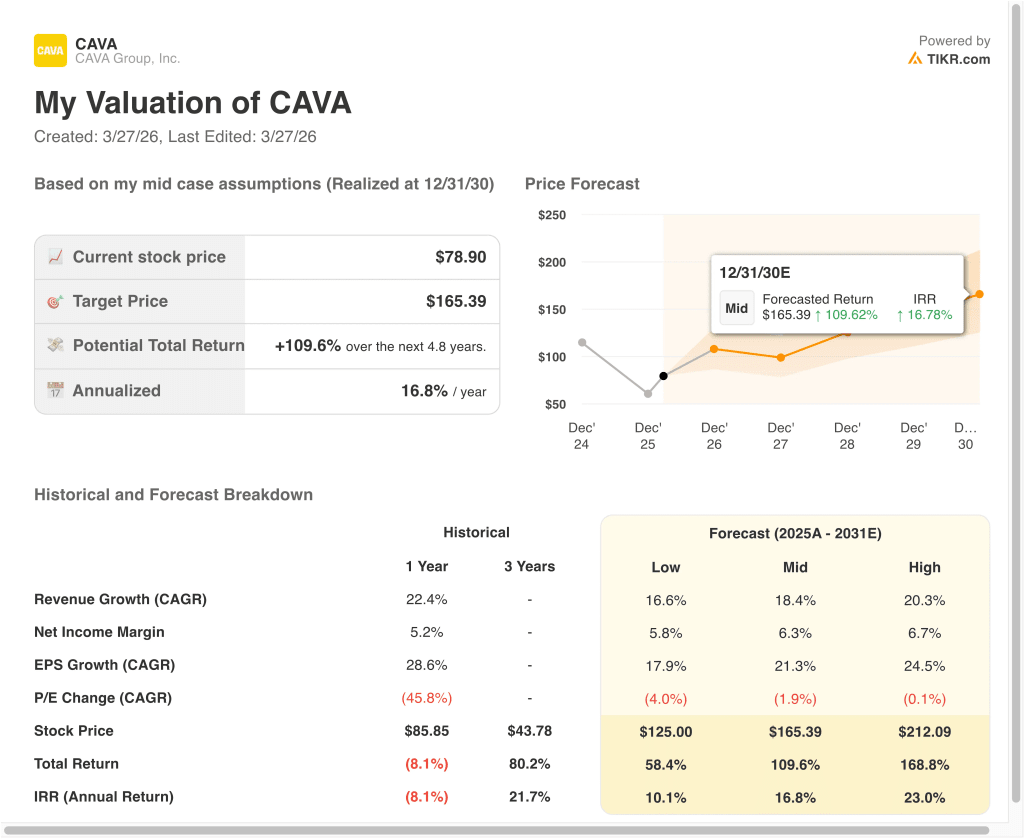

Different scenarios for CAVA stock through 2030 show varied outcomes based on restaurant expansion, same-store sales, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: Unit growth slows, same-restaurant sales moderate, and valuation compresses faster → 10.1% annual returns

- Mid Case: CAVA keeps opening restaurants efficiently and maintains solid traffic and pricing power → 16.8% annual returns

- High Case: New-unit productivity stays strong, margins improve, and the market keeps rewarding growth → 23.0% annual returns

Even in the low case, the model still shows positive returns because CAVA is already a profitable growth chain with a large runway for store openings. The mid case suggests the stock can work well if management keeps scaling the brand without giving up too much margin. The high case shows why investors stay interested, but it also highlights how much future performance is already embedded in a premium restaurant multiple.

Going forward, the stock will likely trade on traffic, same-restaurant sales, and new-unit productivity more than anything else. Investors will also watch whether commodity, wage, and tariff-related costs keep pressuring restaurant-level margins, because that is the clearest risk to a high-multiple restaurant stock. The expected May 12 report is the next major test of whether CAVA can keep pairing strong growth with enough profitability to support its valuation.

See what analysts think about CAVA stock right now (Free with TIKR) >>>

Should You Invest in CAVA Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CAVA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CAVA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze CAVA Group stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!