Key Takeaways:

- Circle is trading as both a crypto infrastructure company and a regulation-sensitive payments platform, so the stock is moving with both USDC adoption and Washington policy headlines.

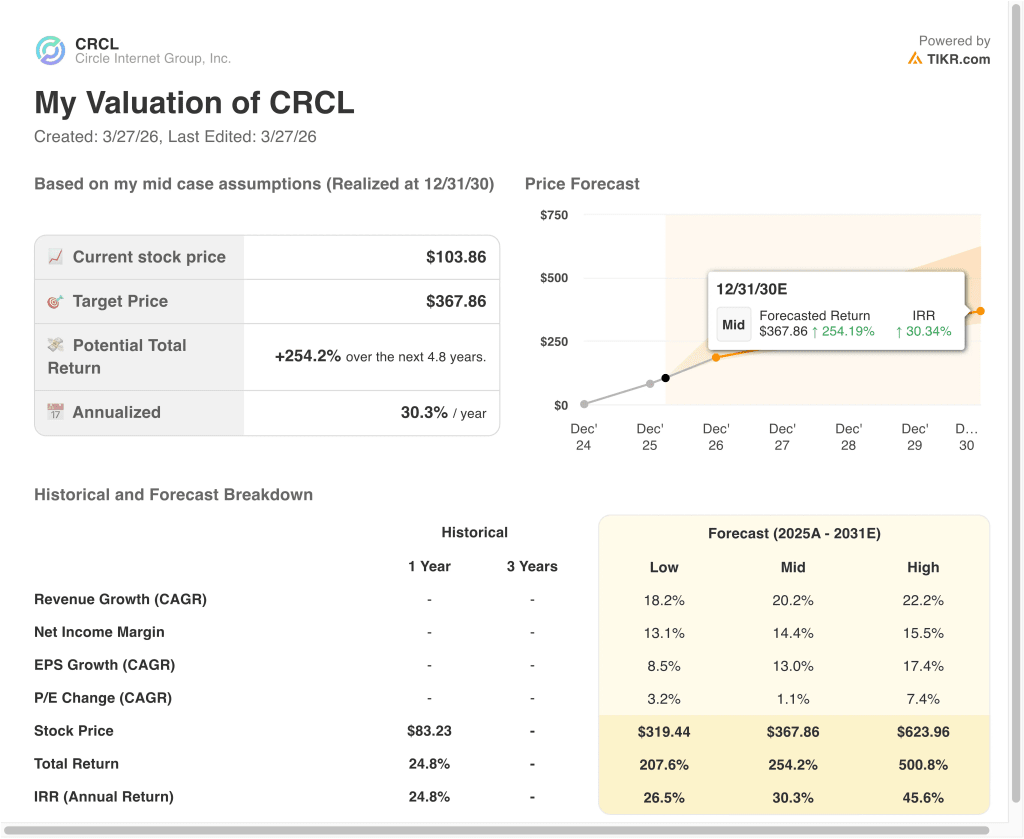

- CRCL stock could reasonably reach $368 per share by December 2030, based on our valuation assumptions.

- This implies a total return of 254.2% from the model’s reference price of $104, with an annualized return of 30.3% over the next 4.8 years.

What Happened?

Circle Internet Group (CRCL) has been relevant this week because investors are trying to separate strong operating momentum from fresh regulatory risk. On March 25, Reuters reported that Circle and Coinbase slid after a report that a new draft of the CLARITY Act would prohibit stablecoin yield payments. For a company tied so closely to USDC adoption, any sign that lawmakers may narrow the economics of stablecoin rewards can change sentiment quickly.

That policy concern arrived only weeks after a much more bullish stretch. Reuters reported on February 25 that Circle topped fourth-quarter revenue expectations, with total revenue and reserve income of $770 million, and the stock jumped nearly 30% in afternoon trading. The same report said USDC circulation rose 72% to $75.3 billion, which reinforced the idea that Circle was gaining scale even as interest rates moved lower.

The company has kept adding commercial proof points as well. Circle announced a collaboration with Sasai Fintech on March 24 to expand USDC access across Africa, and Triple-A said on March 25 that it had integrated with Circle Payments Network to support stablecoin-to-local-currency settlement across major corridors.

Those moves are important because they push Circle deeper into remittances, treasury flows, and cross-border payments rather than leaving it dependent on crypto trading activity alone.

What the Model Says for CRCL Stock

We analyzed the upside potential for Circle stock using valuation assumptions based on expanding USDC circulation, growth in payment and settlement infrastructure, and a business model that still appears early in its public-market life.

The key question is not whether Circle has growth, because it clearly does. The harder question is whether that growth can outpace the regulatory and multiple risk that comes with being a stablecoin platform.

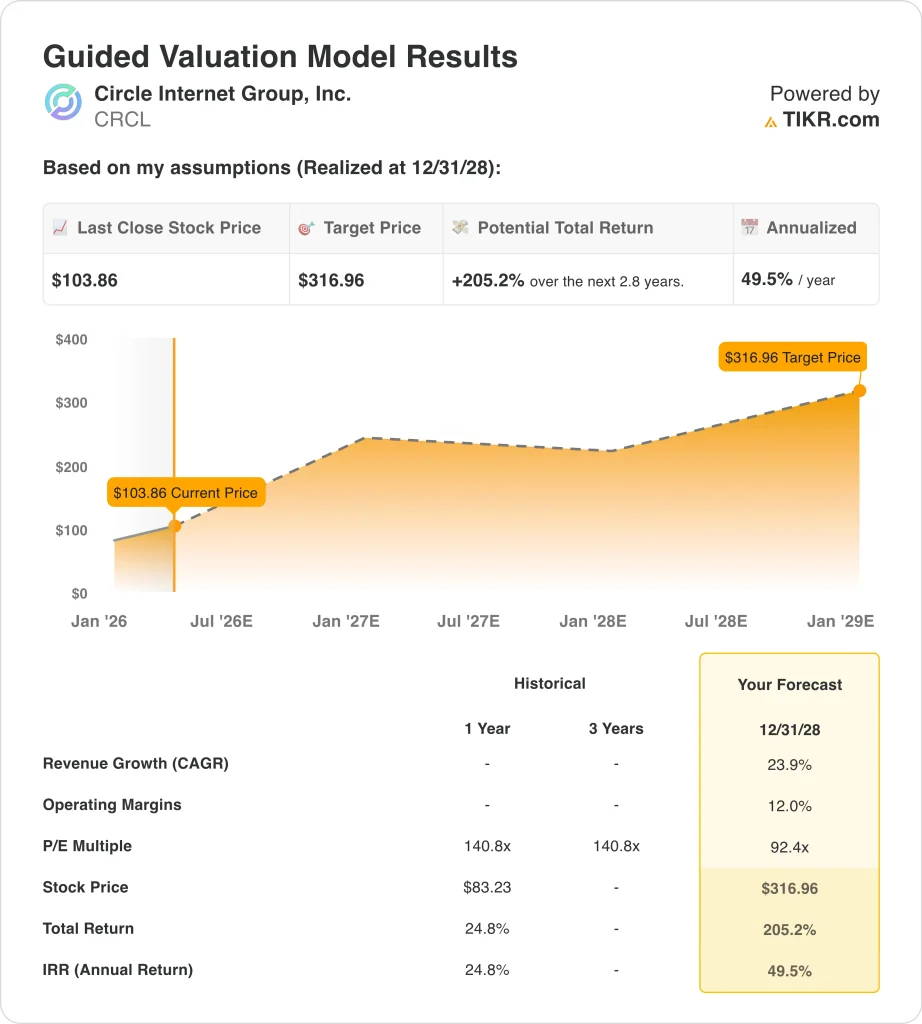

Based on our valuation framework, Circle could reach $368 per share by December 2030 from the model’s reference price of $104. That would imply a 254.2% total return and a 30.3% annualized return over the next 4.8 years. A shorter-dated case is also strong, with a target price of $317 by December 2028 and a 49.5% annualized return from the same reference price.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRCL stock:

1. Revenue Growth: 23.9%

Circle’s recent operating data support a strong top-line growth discussion, even though the historical figures in the financial table are uneven. In the fourth quarter of 2025, Circle reported total revenue and reserve income of $770 million, up 77% year over year, and full-year revenue and reserve income of $2.7 billion, up 64%. That acceleration was driven largely by reserve income as USDC circulation expanded sharply.

The main business driver is stablecoin scale. Circle said USDC in circulation reached $75.3 billion at year-end 2025, while USDC on-chain transaction volume in the quarter was $11.9 trillion, up 247% year over year. That matters because more circulation can lift reserve income, and more transaction activity can support payments, treasury, and infrastructure use cases around the network.

A 23.9% revenue growth assumption is demanding, but it reflects the fact that Circle is still expanding across new corridors and products. Recent announcements with Sasai Fintech in Africa and Triple-A in cross-border settlement show that Circle is trying to add real-world utility on top of USDC. If that network keeps broadening, strong revenue growth can remain part of the valuation debate even if regulation stays noisy.

2. Operating Margins: 12%

The margin story is more mixed, and that is one reason the stock trades with such sharp swings. The financial table you provided shows that the operating margin moved from 17.9% in 2021 to 12.4% in the latest period, while the LTM EBIT margin on the overview is also 12.4%. So Circle is growing, but not all of that growth is falling cleanly to the bottom line.

Part of the pressure came from public-company costs and one-time items. Circle said fourth-quarter 2025 operating expenses rose 95% year over year, including a $48 million increase in stock-based compensation after the IPO and a $23 million charge related to the Circle Foundation. Even so, adjusted EBITDA rose 412% to $167 million, which shows the underlying operating model still has leverage when volume grows fast enough.

Using a 12.0% operating margin assumption is therefore not especially aggressive. It is close to the recent reported margin and leaves room for the business to keep investing in distribution, regulation, and infrastructure buildout. For Circle, the valuation case depends more on durable growth and network expansion than on immediate margin expansion alone.

3. Exit P/E Multiple: 92.4x

The exit multiple is high, but Circle is not being valued like a mature payments company or a traditional software stock. The attached overview shows an NTM P/E of 92.35x, and the shorter-dated valuation framework uses a 92.4x exit P/E. That tells you the market still sees Circle as an early-stage platform tied to a large and still-forming category.

There is also a reason investors are willing to pay such a large multiple. Circle sits in the middle of stablecoins, tokenized payments, and crypto-linked financial infrastructure, and each of those markets is still developing. The business also benefits when investors believe regulation will legitimize the space, which is why policy headlines can move the stock so quickly in either direction.

That said, a high multiple also raises the risk of compression. The same regulatory backdrop that can expand Circle’s addressable market can also narrow key economics, as the March CLARITY Act headlines showed. So the valuation case works best if Circle keeps compounding network usage and commercial partnerships fast enough to justify a premium multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for CRCL stock through 2030 show varied outcomes based on USDC adoption, payments network expansion, and regulation (these are estimates, not guaranteed returns):

- Low Case: Stablecoin regulation gets tighter and commercial monetization takes longer → 26.5% annual returns

- Mid Case: USDC circulation and Circle Payments Network keep scaling across new corridors → 30.3% annual returns

- High Case: Circle captures broader payment, treasury, and blockchain infrastructure demand → 45.6% annual returns

Even in the conservative case, Circle stock still offers positive returns because the company is generating real cash and building multiple infrastructure layers around USDC.

The financial data you provided shows a 2025 free cash flow of $518.5 million, and Circle’s latest results showed continued growth in CPN activity, EURC circulation, and Arc development. That gives the company more than one product lever if the stablecoin market keeps broadening.

The risk is that Circle’s stock will probably keep trading more like a policy-sensitive platform than a steady compounder. Reuters said progress on U.S. crypto market-structure legislation had stalled in March, and separate reporting showed investors reacted sharply to a draft that could restrict stablecoin yield payments. For a company with a premium multiple, that kind of headline can move the shares even when operating performance remains solid.

Going forward, the stock will likely move with three things at once: USDC circulation, new network partnerships, and the direction of U.S. stablecoin regulation. If Circle keeps extending USDC into payments and treasury use cases, investors may keep valuing the company as critical internet-financial infrastructure. But if regulation limits economics or slows adoption, the stock could stay volatile even as the underlying platform keeps expanding.

See what analysts think about CRCL stock right now (Free with TIKR) >>>

Should You Invest in Circle Internet Group, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up CRCL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track CRCL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Circle Internet Group stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!