Key Takeaways:

- Domino’s is being repriced around one core debate: U.S. value promotions are working, but investors still want proof that international demand and franchise growth can stay healthy.

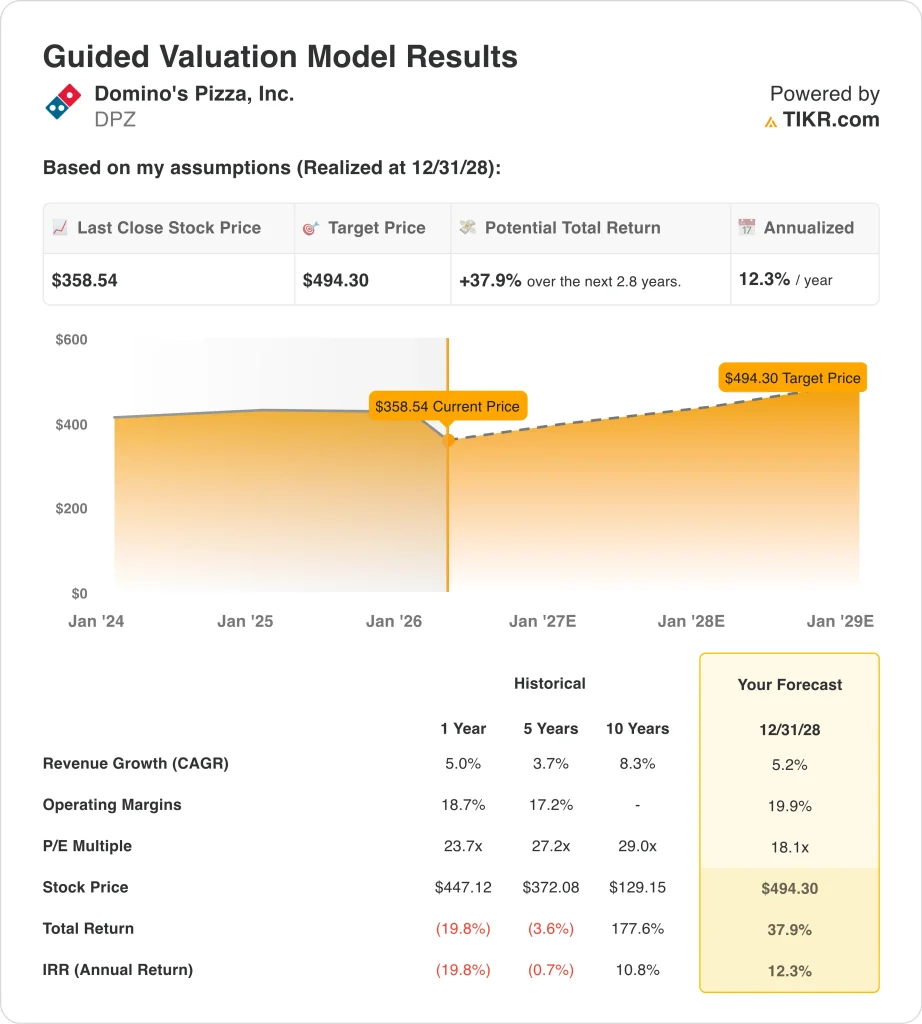

- Domino’s stock could reasonably reach $494 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 37.9% from today’s price of $359, with an annualized return of 12.3% over the next 2.8 years.

What Happened?

Domino’s Pizza (DPZ) released its fourth-quarter earnings report on February 23. Reuters reported that the company beat Wall Street estimates for U.S. same-store sales and posted revenue of $1.53 billion versus expectations of $1.52 billion. Shares rose about 5% in early trading because investors saw clear evidence that value offers were still bringing in traffic.

It also reported 3.0% U.S. same-store sales growth for the full year, 1.9% international same-store sales growth, and global net store growth of 604 locations, which shows the brand is still expanding even in a choppy consumer backdrop.

Management’s tone also helped shape sentiment. CEO Russell Weiner said in the earnings release, “Our Hungry for MORE strategy drove strong order count growth and market share gains in 2025,” and he said the company expects to “significantly grow market share in the U.S. quick-service restaurant pizza segment over the long term.”

Still, the stock has not held its post-earnings strength. Reuters-linked market coverage on February 24 highlighted a JPMorgan upgrade to overweight, but the shares remain well below the $426 year-end close in the financial data the user provided.

Investors seem to be balancing solid U.S. execution against softer international trends, heavy leverage, and a valuation that still needs steady earnings growth to look compelling.

Here’s why Domino’s stock could deliver solid returns through 2028 if U.S. same-store sales stay healthy, margins keep improving, and the market becomes more comfortable with the company’s debt-heavy but cash-generative model.

What the Model Says for DPZ Stock

We analyzed the upside potential for Domino’s stock using valuation assumptions based on steady same-store sales, continued unit growth, and strong free cash flow generation.

Based on estimates of 5.2% annual revenue growth, 19.9% operating margins, and a normalized P/E multiple of 18.1x, the model projects Domino’s stock could rise from $359 to $494 per share.

That would be a 37.9% total return, or a 12.3% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for DPZ stock:

1. Revenue Growth: 5.2%

Domino’s has posted fairly steady top-line growth. Revenue rose from $4.71 billion in 2024 to $4.94 billion in 2025, which was a 5.0% increase, and that followed a 5.1% increase in 2024. That consistency matters because Domino’s is a mature chain, so mid-single-digit growth already signals healthy execution.

The key growth drivers are same-store sales, store openings, and supply chain revenue. In 2025, U.S. same-store sales rose 3.0%, international same-store sales rose 1.9%, and the company added 604 net stores globally. Those figures show that revenue growth is still coming from both higher sales per store and a larger store base.

Based on analysts’ consensus estimates, we use a 5.2% revenue growth assumption. That figure is close to the guided valuation model and close to the company’s recent historical growth rate. It implies that Domino’s can keep gaining share and adding stores, but without assuming a major acceleration in consumer demand.

2. Operating Margins: 19.9%

Domino’s remains a high-margin restaurant operator. Operating margin improved from 18.7% in 2024 to 19.3% in 2025, while operating income rose 8.6% to $955.0 million. That is important because margin improvement gives the company room to grow earnings even if revenue growth stays moderate.

The margin story also links directly to the company’s business mix. Franchise royalties and supply chain sales tend to support strong profitability, and Domino’s generated $792.1 million of operating cash flow and $671.5 million of free cash flow in 2025. That helps explain why investors still give the company credit for quality even while the stock price has weakened this year.

Based on analysts’ consensus estimates, we use a 19.9% operating margin assumption. That is only modestly above the 19.3% margin posted in 2025, so it does not require a dramatic shift in profitability. It assumes Domino’s keeps converting sales growth into earnings through pricing, franchise economics, and supply chain efficiency.

3. Exit P/E Multiple: 18.1x

Valuation is one reason the stock is interesting now. The terminal screenshot shows Domino’s trading at an LTM P/E of 20.4x, while the guided valuation model uses an exit P/E multiple of 18.1x. That means the model already assumes some multiple compression rather than a richer future valuation.

That lower multiple makes sense because Domino’s carries substantial leverage. The balance sheet data shows total debt of about $5.05 billion and net debt of about $4.92 billion at year-end 2025, while the terminal screenshot shows LTM net debt to EBITDA of 4.45x. Investors usually accept that leverage because Domino’s has strong recurring cash flow, but it still limits how much premium the market may be willing to pay.

Based on analysts’ consensus estimates, we maintain an 18.1x exit multiple. That looks reasonable for a company with durable brand strength, healthy margins, and strong cash generation, but also with meaningful financial leverage. If the stock outperforms this model, it will likely be because earnings grow faster than expected, not because investors suddenly pay a higher multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

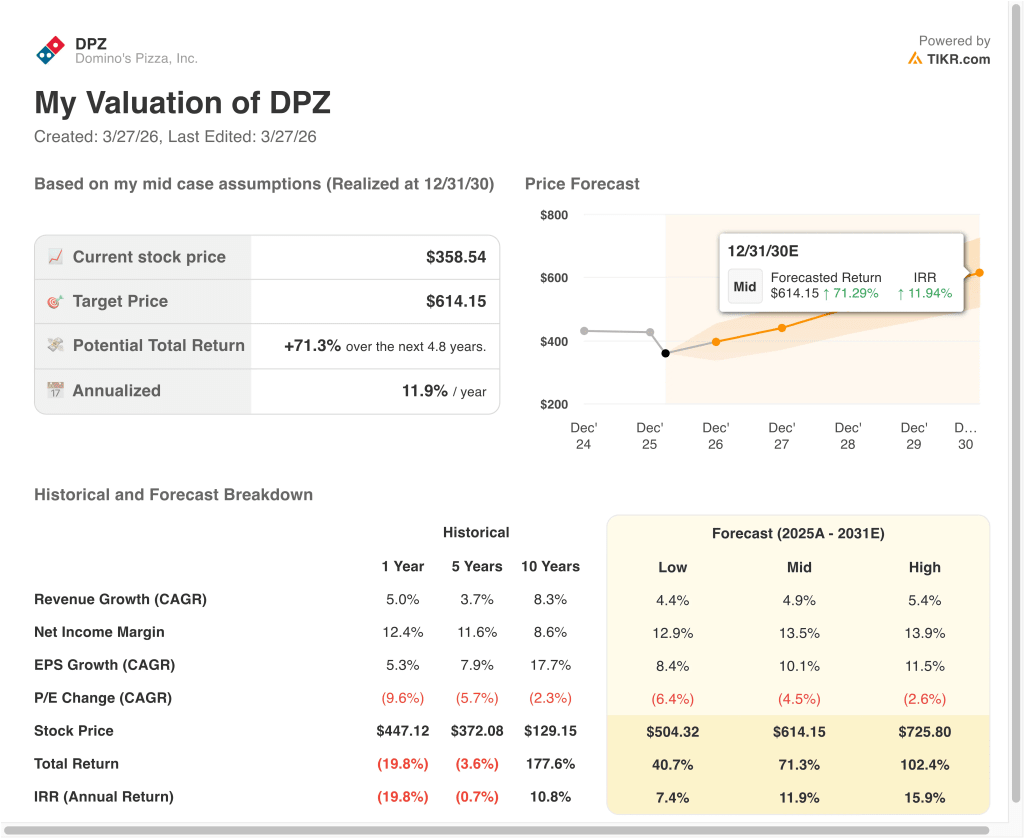

Different scenarios for DPZ stock through 2030 show varied outcomes based on same-store sales, unit growth, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: U.S. traffic softens, international growth stays sluggish, and valuation compresses faster → 7.4% annual returns

- Mid Case: Domino’s keeps gaining share, expands margins, and compounds earnings steadily → 11.9% annual returns

- High Case: Store growth re-accelerates, same-store sales stay healthy, and earnings compound faster than expected → 15.9% annual returns

Even in the low case, the model still points to positive returns because Domino’s remains highly profitable and cash generative. In the mid case, the stock reaches about $614 by 12/31/30, with 71.3% total returns, supported by 4.9% revenue growth, a 13.5% net income margin, and 10.1% EPS growth. In the high case, the stock reaches about $726, with 102.4% total returns, which shows how much stronger earnings compounding can matter even if the P/E multiple still declines modestly.

Going forward, Domino’s stock will likely trade on U.S. same-store sales, international performance, and franchise health. The April 27 earnings report is the next major checkpoint because it should show whether the strong fourth quarter carried into 2026. If comparable sales and operating income hold up, the stock could start to look more like a steady compounder again rather than a restaurant name stuck in a valuation reset.

See what analysts think about DPZ stock right now (Free with TIKR) >>>

Should You Invest in Domino’s Pizza, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up DPZ, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track DPZ alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Domino’s Pizza stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!