Key Takeaways:

- Roku is getting attention because platform revenue is still growing, profitability improved sharply in 2025, and management guided 2026 revenue above Wall Street estimates, but the stock is also reacting to a weaker 2026 tape and a still-demanding earnings multiple.

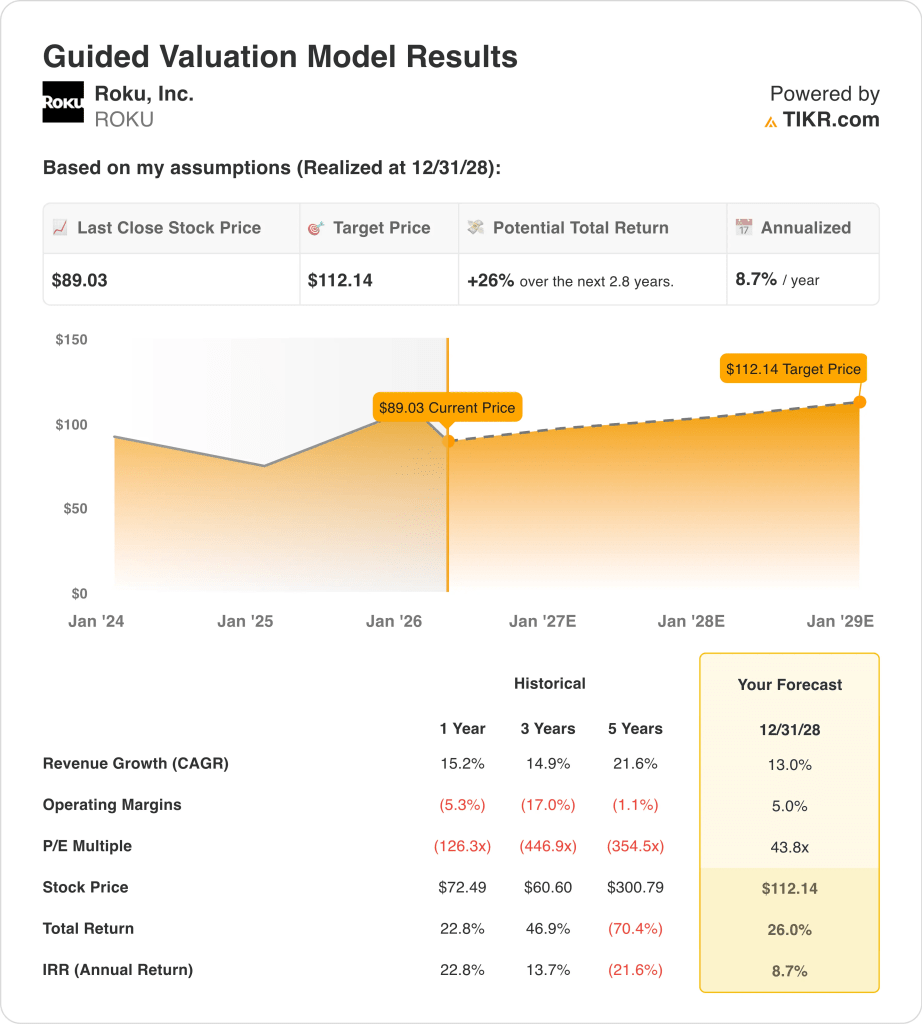

- Roku stock could reasonably reach $112 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 26.0% from today’s price of $89, with an annualized return of 8.7% over the next 2.8 years.

What Happened?

Roku, Inc. (ROKU)’s latest big stock-moving event was its February earnings report. Reuters reported the shares jumped about 12% after Roku forecast 2026 revenue of $5.5 billion, above analysts’ estimates of $5.34 billion, and said platform revenue should reach $4.89 billion. That response showed investors were encouraged by the company’s ad and platform momentum, even after a volatile stretch for growth stocks.

The quarter itself also looked solid. Reuters said fourth-quarter platform revenue came in at $1.22 billion and beat forecasts, while Roku tied that outlook to the shift toward ad-supported streaming. In plain terms, Roku is benefiting as more TV viewing moves to streaming and as advertisers follow that audience to connected TV.

Roku’s own updates reinforced that story in March. The company launched Howdy on Prime Video, and said the move expands the service beyond the Roku platform for the first time, while supporting its subscription and platform revenue strategy.

It also rolled out Roklue, a new discovery-focused game on the Roku home screen, which shows management is still investing in engagement features that can keep viewers inside the ecosystem longer.

Even so, the stock has pulled back this year. The market is likely balancing Roku’s stronger fundamentals against valuation sensitivity, insider selling disclosures, and a broader reset in higher-multiple media and software names. The next key checkpoint is Roku’s expected Q1 2026 results on April 24, which should show whether platform growth and monetization stayed strong into the new year.

Here’s why Roku stock could still deliver moderate returns through 2028 as platform revenue, advertising demand, and subscription monetization improve, but the stock likely needs steadier execution to justify a higher multiple.

What the Model Says for ROKU Stock

We analyzed the upside potential for Roku stock using valuation assumptions based on its platform-led revenue mix, improving profitability, and large connected TV reach.

Based on estimates of 13.0% annual revenue growth, 5.0% operating margins, and a normalized P/E multiple of 43.8x, the model projects Roku stock could rise from $89.03 to $112.14 per share.

That would be a 26.0% total return, or a 8.7% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ROKU stock:

1. Revenue Growth: 13%

Roku’s revenue growth has become steadier again after a harder period in 2022 and 2023. Revenue rose from $4.1 billion in 2024 to $4.7 billion in 2025, which was a 15.2% increase. That matters because it shows the platform business is still expanding at a double-digit rate even at Roku’s current scale.

The key driver is platform revenue, not hardware. Reuters said Roku’s 2026 platform revenue outlook is $4.89 billion, and management tied that to strength in advertising and content distribution as consumers keep shifting toward ad-supported streaming. That means Roku’s business is increasingly driven by monetizing viewing activity rather than by just selling devices.

Based on analysts’ consensus estimates, we used a 13.0% forecast. That is below the company’s recent 15.2% historical growth rate, so it is not assuming a dramatic acceleration.

It reflects a business that can still grow through advertising, subscriptions, and engagement, but also faces a larger revenue base and a more competitive streaming market.

2. Operating Margins: 5%

Roku’s margin story has improved, but it is still early. Operating margin moved from -12.5% in 2023 to -4.6% in 2024 and then to essentially break-even in 2025. That trend matters because a platform company like Roku can create much more earnings power if revenue keeps growing faster than operating costs.

The cash flow improvement supports that argument. Roku generated $483.7 million of operating cash flow and $478.4 million of free cash flow in 2025, both much better than the prior year. So even though the reported EBIT margin is still near zero, the business is already showing much better financial quality than the income statement alone suggests.

Based on analysts’ consensus estimates, we use 5.0% operating margins. That is a clear improvement from current levels, but it still looks measured for a scaled platform business. It assumes Roku keeps monetizing platform usage better, while also maintaining cost discipline after years of restructuring and operating resets.

3. Exit P/E Multiple: 43.8x

Roku’s multiple remains one of the most debated parts of the story. ROKU stock is trading at an LTM P/E of 150.9x, while the guided valuation model uses a much lower 43.8x exit multiple. That means the valuation case already assumes notable multiple compression from current trailing levels.

That lower exit multiple makes sense because Roku is profitable again, but not yet a high-margin earnings machine. Investors are willing to pay up for connected TV exposure, yet they still want proof that platform revenue can translate into durable operating margins. The stock’s 2026 pullback reflects that tension between real business progress and valuation discipline.

Based on analysts’ consensus estimates, we maintain a 43.8x exit multiple. That assumption gives Roku credit for platform scale, strong balance sheet liquidity, and improving profitability, but it does not assume the market values it like a peak-cycle streaming stock again. If Roku beats this model, it will probably be because earnings scale faster, not because the multiple expands.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

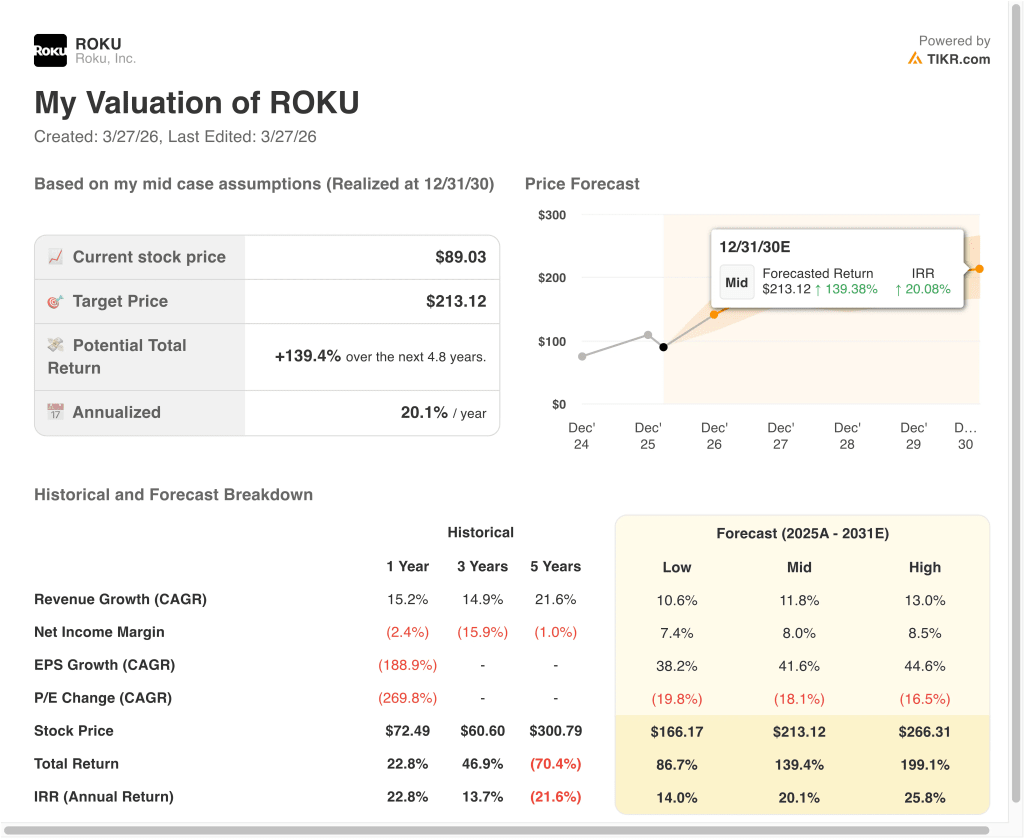

Different scenarios for ROKU stock through 2030 show varied outcomes based on platform growth, advertising demand, and margin expansion (these are estimates, not guaranteed returns):

- Low Case: Advertising demand softens, subscription momentum cools, and valuation compresses faster → 14.0% annual returns

- Mid Case: Roku keeps scaling platform revenue, improves monetization, and converts more gross profit into earnings → 20.1% annual returns

- High Case: Platform engagement, ad budgets, and subscription economics remain very strong, and earnings compound faster than expected → 25.8% annual returns

Even in the conservative case, Roku’s model still shows positive returns because the company has a large user base, improving cash flow, and a net cash balance sheet. The mid case suggests the stock can work well if connected TV advertising and platform monetization keep improving together. The high case shows how sensitive the upside becomes if Roku turns scale into stronger margins while the market stays constructive on streaming platforms.

Going forward, Roku stock will likely trade on platform revenue growth, advertising demand, and signs of sustained margin improvement. Investors will also watch new subscription products and engagement tools, because those can deepen monetization without relying on device sales. The April earnings report is the next major test of whether Roku’s stronger 2025 finish is carrying into 2026.

See what analysts think about ROKU stock right now (Free with TIKR) >>>

Should You Invest in Roku, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ROKU, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track ROKU alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Roku stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!