Key Takeaways:

- UnitedHealth is under pressure because investors are resetting expectations for Medicare Advantage, margins, and 2026 revenue growth after a weak outlook.

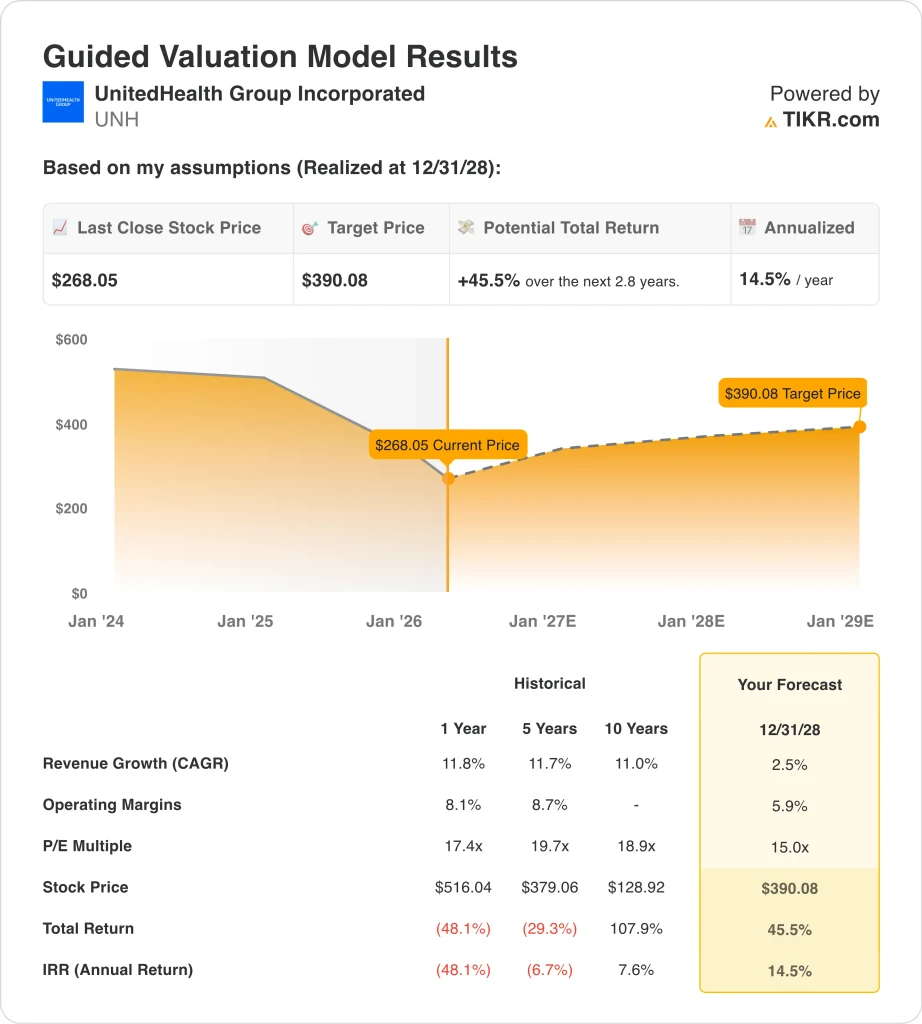

- UnitedHealth stock could reasonably reach $390 per share by December 2028, based on our valuation assumptions.

- This implies a total return of 45.5% from today’s price of $268, with an annualized return of 14.5% over the next 2.8 years.

What Happened?

UnitedHealth Group Incorporated (UNH)’s biggest stock-moving event was its January earnings release. The company reported 2025 revenue of $447.6 billion and said 2026 revenue should exceed $439.0 billion, with adjusted earnings above $17.75 per share. Reuters said that the outlook came in below Wall Street expectations, and the stock fell sharply as investors reset their assumptions for growth and profitability.

The policy backdrop made that reaction worse. Reuters reported that health insurers sold off after the Trump administration proposed a smaller-than-expected increase to 2027 Medicare Advantage payment rates. Medicare Advantage is the privately administered version of Medicare, so lower reimbursement growth can pressure revenue and margins for insurers like UnitedHealth if medical costs keep rising faster than payments.

Management tried to frame 2025 as a reset year rather than a broken model. CEO Stephen Hemsley said, “We confronted challenges directly and finished 2025 as a much stronger company,” while the company also pointed to $19.7 billion of operating cash flow and a dividend of $2.21 per share paid in March.

Since then, the company has stayed active ahead of the next earnings report. UnitedHealth announced that first-quarter 2026 results will be released on April 21, and March business updates focused on AI tools at Optum Rx, plus broader maternal care support through UnitedHealthcare. Those items help the strategic story, but investors still seem more focused on whether reimbursement, utilization, and margin trends improve in the next quarter.

Here’s why UnitedHealth stock could deliver stronger returns through 2028 if Medicare Advantage pressure eases and margins recover, but the stock likely needs better policy visibility and cleaner earnings execution first.

What the Model Says for UNH Stock

We analyzed the upside potential for UnitedHealth stock using valuation assumptions based on modest revenue growth, some margin recovery, and a lower earnings multiple than the stock carried in prior years.

Based on estimates of 2.5% annual revenue growth, 5.9% operating margins, and a normalized P/E multiple of 15.0x, the model projects UnitedHealth stock could rise from $268 to $390 per share.

That would be a 45.5% total return, or a 14.5% annualized return over the next 2.8 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for UNH stock:

1. Revenue Growth: 2.5%

UnitedHealth’s revenue base is enormous, so even low-single-digit growth still represents a very large dollar increase. Revenue rose from $400.3 billion in 2024 to $447.6 billion in 2025, which was 11.8% growth. The model’s 2.5% growth assumption is much lower, which shows how much caution is now embedded in the valuation.

The reason for that caution is straightforward. UnitedHealth’s January outlook called for more than $439.0 billion in 2026 revenue, and Reuters said that implied a decline from 2025 and missed analysts’ expectations. That weaker guide followed previously announced business cuts and a softer reimbursement backdrop in Medicare Advantage.

So the 2.5% assumption looks restrained, but still realistic over a multi-year horizon. It gives UnitedHealth credit for retaining scale across insurance, pharmacy services, and care delivery, while also acknowledging that near-term growth has slowed materially.

2. Operating Margins: 5.9%

Operating margin is the key valuation debate because that is where the pressure showed up most clearly in 2025. UnitedHealth’s operating margin fell from 8.1% in 2024 to 4.2% in 2025, while operating income dropped from $32.3 billion to $19.0 billion. That kind of compression matters because a large insurer can still grow revenue while disappointing investors if medical costs and utilization rise too quickly.

The model uses a 5.9% operating margin, which implies recovery from 2025 levels but not a full return to older profitability. That looks reasonable because management’s 2026 outlook called for more than $24.0 billion of earnings from operations, which would improve from 2025 even though revenue guidance remained soft.

This assumption matters because UnitedHealth is no longer being judged only on growth. Investors want proof that Optum and UnitedHealthcare can restore earnings quality while still absorbing cost pressure in Medicare, care delivery, and pharmacy. If margins do not recover, the stock may stay cheap even with solid cash flow.

3. Exit P/E Multiple: 15x

UnitedHealth historically traded at a higher earnings multiple than many traditional insurers because of its scale, service mix, and consistent growth. The model uses a 15.0x exit P/E, which is below the recent LTM P/E of 20.3x. That lower multiple reflects the market’s current skepticism after the 2026 guidance reset and the Medicare Advantage rate shock.

A 15.0x multiple still gives the company some credit for quality. UnitedHealth remains highly cash generative, produced $16.1 billion of free cash flow in 2025, and continues to pay a dividend that the company raised to $2.21 per quarter. But it no longer makes sense to assume the market will pay the same premium multiple it once did while earnings visibility is weaker.

Based on analysts’ consensus estimates, we maintain a 15.0x exit multiple. That assumption fits a business that still has scale advantages and broad health care exposure, but now faces more policy and cost uncertainty than before.

If the stock does better than this model, it will likely be because earnings recover faster, not because the market suddenly rewards it with a richer multiple.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for UNH stock through 2030 show varied outcomes based on reimbursement trends, margin recovery, and valuation discipline (these are estimates, not guaranteed returns):

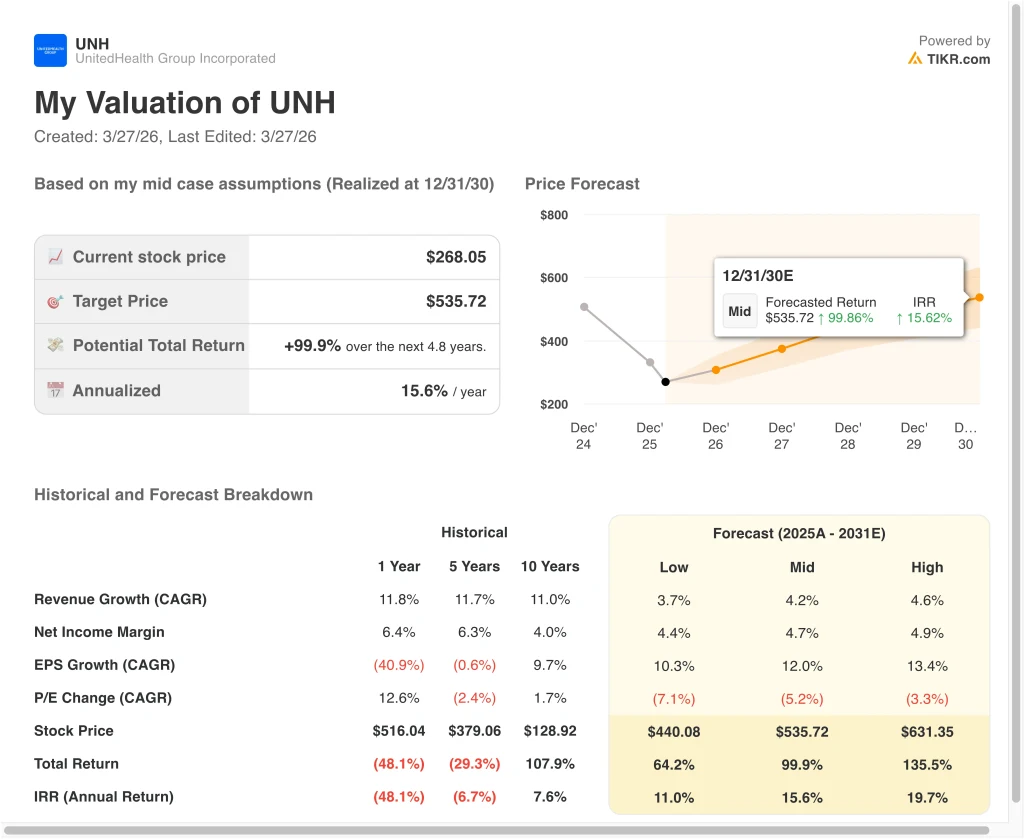

- Low Case: Medicare Advantage pressure stays elevated, and margin recovery remains slow → 11.0% annual returns

- Mid Case: UnitedHealth stabilizes utilization trends and rebuilds earnings across Optum and UnitedHealthcare → 15.6% annual returns

- High Case: Medical costs normalize faster, and the market regains confidence in long-term growth → 19.7% annual returns

Even in the low case, the model still points to positive returns because UnitedHealth remains profitable, highly scaled, and cash generative. The mid case produces a $536 target by 2030, with 99.9% total returns, which reflects 4.2% revenue growth, a 4.7% net income margin, and 12.0% EPS growth. The high case reaches $631, with 135.5% total returns, and it assumes stronger revenue growth of 4.6% plus slower annual multiple compression of 3.3%.

Going forward, UnitedHealth stock will likely trade on policy updates, medical utilization, and margin recovery more than anything else. The April 21 earnings report is the next major checkpoint because it should show whether the January reset was the bottom or just an early warning. If earnings and operating margins stabilize, the stock could start trading more like a recovery story than a policy casualty.

See what analysts think about UNH stock right now (Free with TIKR) >>>

Should You Invest in UnitedHealth Group Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up UNH, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track UNH alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze UnitedHealth stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!