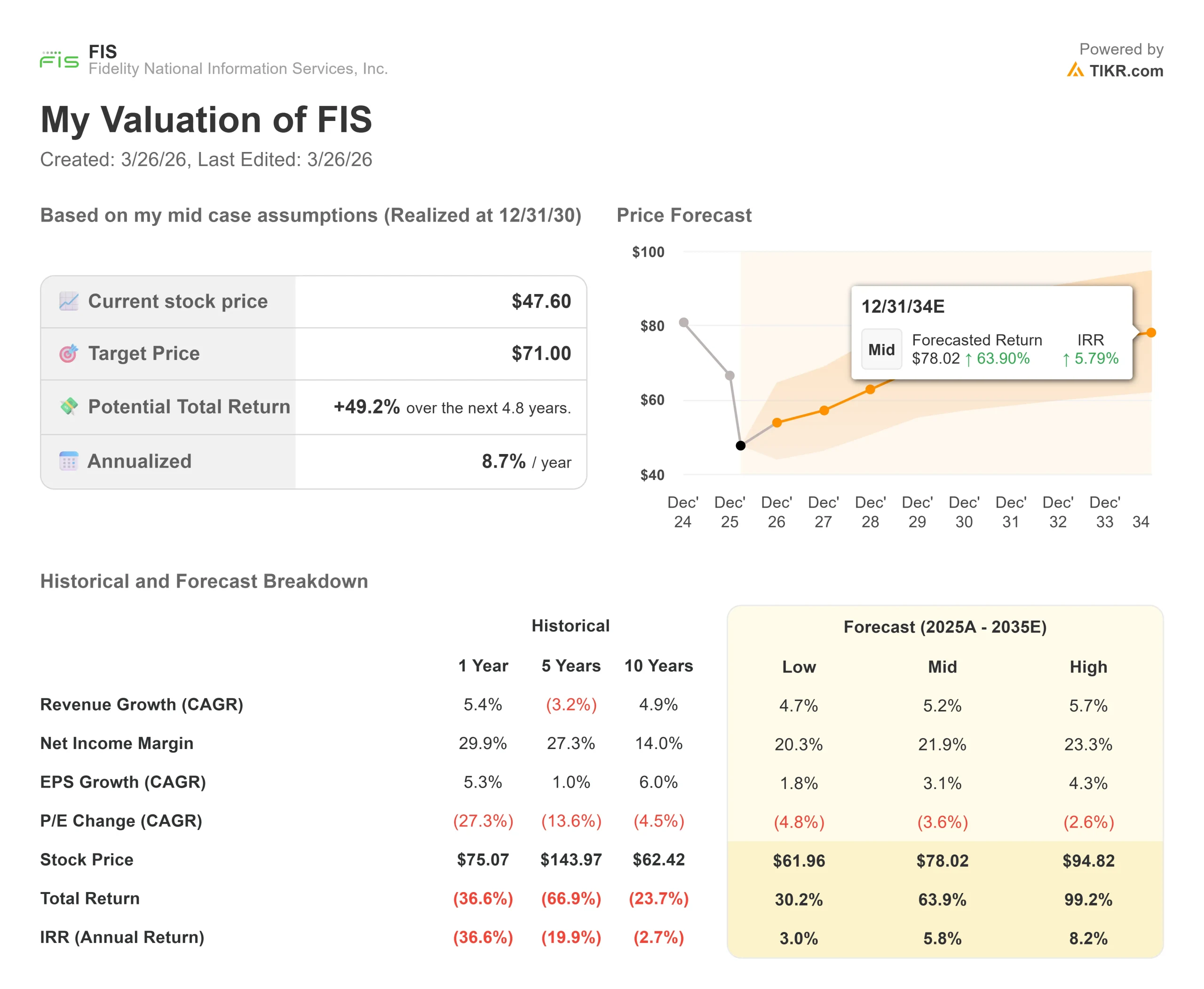

Key Stats for Fidelity National Information Services Stock

- Current Price: $47.6

- Target Price: $71

- Street Target: $66.5

- Potential Total Return: +49.2%

- Annualized IRR: 8.7%

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

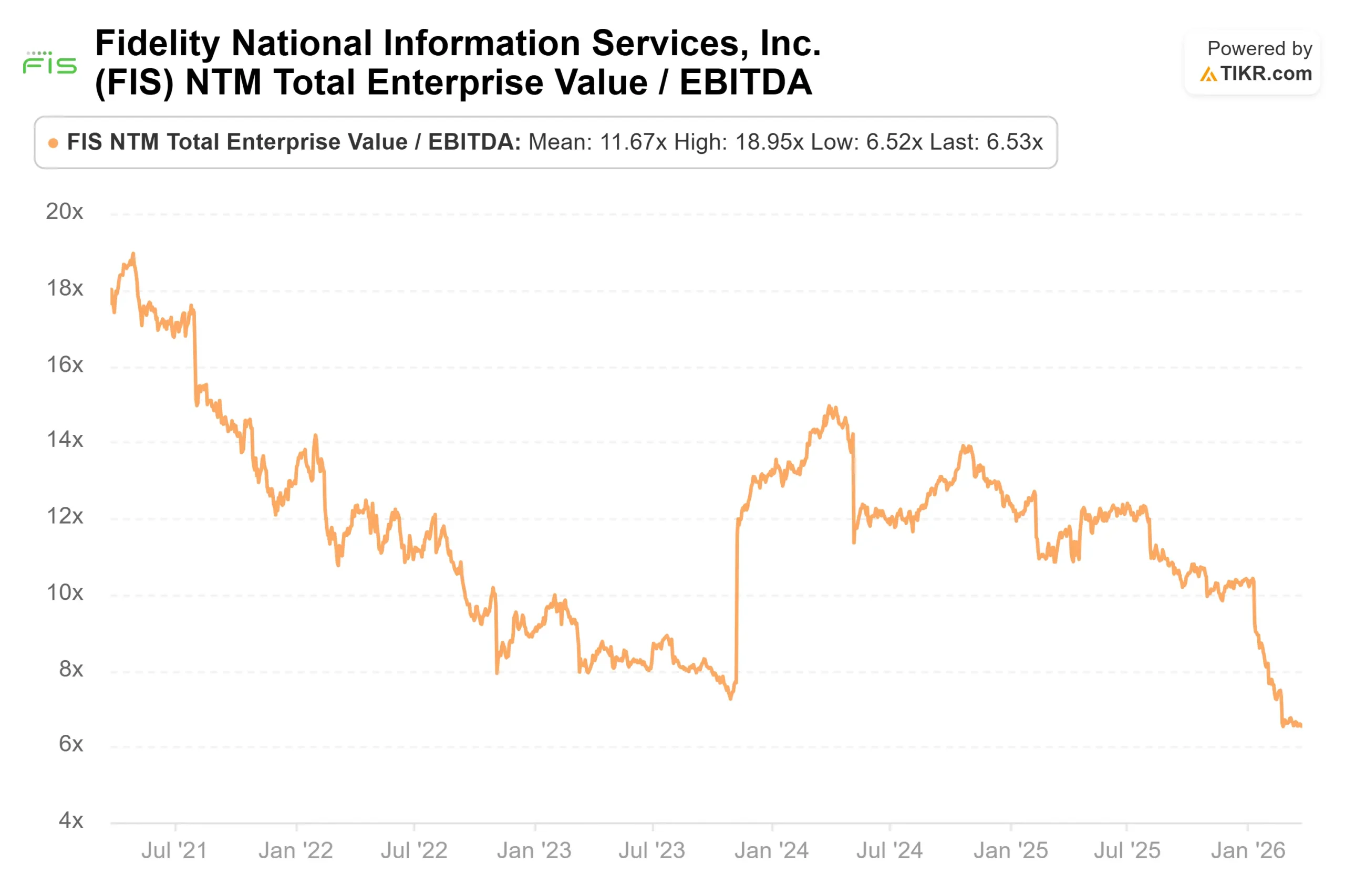

Fidelity National Information Services (FIS) stock has shed roughly 25% of its value year-to-date, suffering a bruising 43.17% maximum drawdown in early 2026 to hover near $47.

Wall Street is locked in a fierce debate over the company’s radical restructuring: bulls argue that shedding legacy merchant businesses to focus purely on high-margin banking software creates an unmatched data moat ready for AI monetization, while bears counter that near-term integration costs and margin contraction will crush earnings momentum.

The single unresolved question the market is frantically trying to price is whether management can execute its AI-driven headcount reductions fast enough to double free cash flow by 2028, or if stranded operational costs will derail the timeline.

Into this debate, CFO James Kehoe took the stage at the Wells Fargo Payments/Fintech Symposium on March 18, 2026, with a direct message: the underlying core banking business is organically accelerating, AI is already driving massive back-office savings, and the cash flow explosion is mathematically locked in.

The foundation of FIS’s transformation is a ruthless shift in how it pays its sales teams.

Management recently overhauled commercial commissions to heavily penalize low-margin service contracts while massively rewarding recurring software sales.

For example, Business Process as a Service (BPaaS) was aggressively deprioritized. By forcing the sales force to chase high-margin digital software, Annual Contract Value (ACV) surged by an impressive 20% in Q4 2025.

This momentum is heavily intertwined with FIS’s massive portfolio realignment, anchored by the reality of the company officially closing its acquisition of the Global Payments Issuer Solutions business and simultaneously completing the sale of its remaining Worldpay equity stake.

With the tax bill from the Worldpay sale now accounted for, FIS is aggressively cross-selling its newly acquired credit issuing platform.

Kehoe noted that the legacy owners of the credit business had treated international operations like a cash cow, underinvesting in sales.

FIS has immediately armed its massive global sales force with dual quotas to cross-sell the “Prime” international credit processing platform into Europe and Latin America, chasing down a stated $45 million by 2028, with an aspirational mid-term goal of $125 million in revenue synergies.

However, the true “jewel of the crown,” in Kehoe’s own words, is the payments business cross-sell. Because FIS operates true Systems of Record, the foundational, highly regulated software ledgers that hold a bank’s critical, unalterable data like account balances, they possess a structural moat that nimble AI startups cannot replicate.

“We have systems of record and systems of record are deterministic. They’re not probabilistic,” Kehoe explained, noting the impossibility of using guessing-based AI to run a bank ledger.

“The data we’ve accumulated over decades is essentially the secret sauce of the company.”

This moat was validated in the real world just days prior to the conference when Mizuho Financial Group officially selected FIS’s Balance Sheet Manager platform to navigate complex new Japanese regulatory reporting requirements.

FIS is funneling decades of this proprietary data into its new Enterprise Data and AI (EDAI) engine, a centralized platform combining consumer data across core banking, debit, credit, and wealth into a single panoramic view, allowing commercial banks to make faster lending decisions safely.

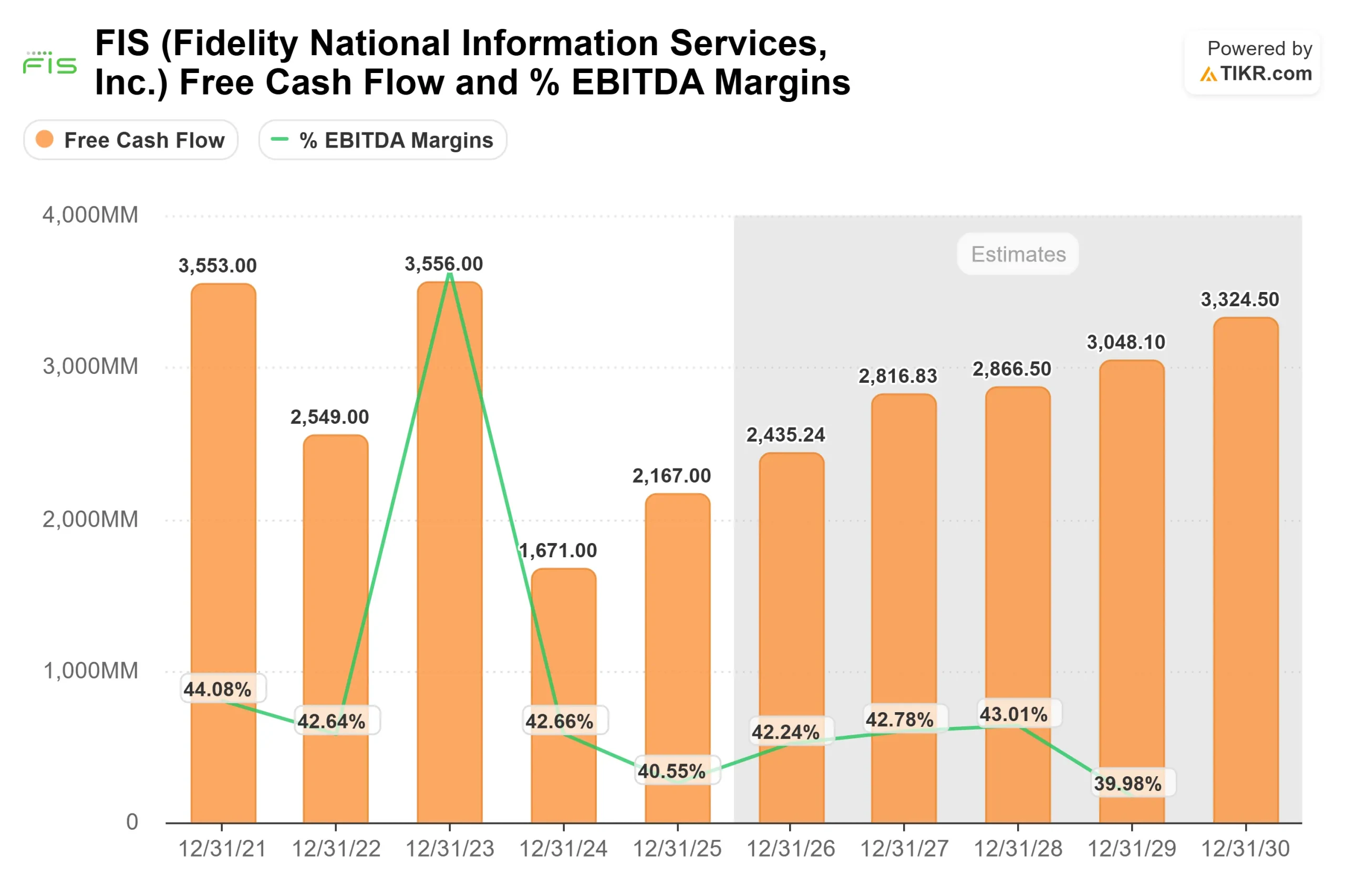

Simultaneously, FIS is using AI offensively on its own cost structure. By rolling out GitHub Copilot to its engineering teams, the company drove a massive 7,000-person headcount reduction through 2025, paving the way for a projected $1 billion expansion in free cash flow as severance and transformation costs roll off.

See historical and forward estimates for Fidelity National Information Services stock (It’s free!) >>>

Is Fidelity National Information Services Undervalued Today?

The market’s severe punishment of FIS in early 2026 suggests widespread anxiety regarding the company’s ability to cleanly digest its portfolio overhaul while fending off nimble fintech competitors. Yet, the underlying cash metrics tell a different story.

Trading heavily against the $66.52 Street consensus target, the current share price near $47 fails to reflect the reality management described: accelerating 20% growth in recurring ACV, tangible AI-driven headcount leverage, massive international banking wins like the Mizuho deal, and a structural exit from low-margin services.

While bears point out that FIS’s 2026 adjusted EPS guidance of 8% to 10% was merely in-line with expectations, management emphasized a completely different metric: cash flow per share.

Adjusted Free Cash Flow is projected to grow 30% in 2026 alone.

Because the massive $800 million in one-time transformation expenses (like severance and software integration for the new credit issuer business) are scheduled to step down by at least 50% by 2028, the underlying EBITDA growth will convert into pure cash, targeting over $3 billion by 2028, unlocking aggressive share repurchases in the back half of the decade.

Analyze historical valuation multiples for FIS (It’s free!) >>>

TIKR Advanced Model Analysis

The TIKR Advanced Model calculates the long-term impact of FIS successfully pivoting its sales mix toward high-margin digital payments and realizing its massive AI-driven operating leverage.

- Current Price: $47.6

- Target Price: $71

- Potential Total Return: +49.2%

- Annualized IRR: 8.7%

Build a 4-year Valuation Model for FIS for yourself (It’s free) >>>

The Mid Case model projects a strong $71.00 target price, driven by a 5.2% Revenue CAGR over the forecast period. This assumes that the functional shift to cross-selling debit and credit platforms directly into the highly concentrated pool of large commercial banks successfully defends the company’s market share against cheaper, down-market alternatives.

The true valuation lever, however, is the targeted expansion of its Net Income Margins, which are modeled at 21.9% in the Mid case over the forecast period, expanding from depressed recent GAAP levels as transformation costs roll off. To achieve this, FIS must flawlessly execute its EDAI monetization strategy while maintaining the strict cost discipline established by its 2025 headcount reductions. If the $800 million in transformation costs fade as promised and the high-margin recurring ACV continues to compound, the 8.7% annualized IRR provides a highly attractive entry point following the brutal Q1 drawdown.

Conclusion: FIS is no longer a sprawling, unfocused payments conglomerate. It is an optimized, high-margin cash engine built exclusively to serve the largest financial institutions in the world. While the broader market remains fixated on near-term integration noise and a 43% max drawdown, the underlying fundamentals, a 20% surge in recurring ACV, a clear path to $3 billion in 2028 free cash flow, and expanding margins, point to an extreme dislocation between perception and reality. Watch the upcoming quarters for proof of international cross-sell execution; if the pipeline converts to revenue as Kehoe predicts, the path to the $71 model target is highly secure.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Fidelity National Information Services?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Fidelity National Information Services, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fidelity National Information Services alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Fidelity National Information Services on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!