Key Stats for Lam Research Stock

- Past-Week Performance: %

- 52-Week Range: $56.3 to $256.7

- Current Price: $211.6

What Happened?

Lam Research (LRCX), the semiconductor equipment maker whose etch and deposition tools sit inside virtually every advanced chip factory on earth, crossed $20.6 billion in full-year 2025 revenue for the first time, up 27% year-over-year, even as its shares trade at $211.62 following a 9.4% single-day drop on March 26.

On January 28, CFO Doug Bettinger guided March 2026 quarter revenue to $5.7 billion, above the $5.34 billion December 2025 record, while projecting 2026 industry wafer fabrication equipment, the total annual spend on chip-making tools, to reach $135 billion, up 23% from $110 billion in 2025, the most aggressive forecast among peers.

Foundry and logic, the segment covering chips that serve as the brains of AI systems, contributed 59% of systems revenue in 2025, up from 35% just one year prior, a reversal that redefines Lam from a memory-centric company into a balanced platform play spanning AI logic, high-bandwidth memory, and advanced packaging.

On February 3, Lam announced leadership transitions described as increasing company velocity for the AI era, and on February 17, opened a new 9,200 sq. ft. Boise, Idaho office supporting approximately 150 personnel focused on advanced memory manufacturing for Micron.

Timothy Archer, President and Chief Executive Officer, stated on the Q2 2026 earnings call that “the growth we envisioned for Lam at our investor event 1 year ago is materializing faster than we anticipated,” tying the statement directly to the company’s advanced packaging business growing more than 40% in 2026 and its NAND upgrade cycle accelerating beyond the original $40 billion multi-year forecast.

Lam’s installed base of 102,000 chambers, the fleet of tools generating recurring spare parts, service, and upgrade revenue that the company calls CSBG, already producing $7.2 billion in 2025, combined with a $5.1 billion buyback authorization, an 85% free cash flow return commitment, and a SAM expanding toward the high-30s percent of global WFE, positions the company to more than double revenue and profit within five years per its own investor day framework.

Wall Street’s Take on LRCX Stock

Lam’s record $20.6 billion 2025 revenue, combined with a 27% growth rate already running ahead of its own investor day model, sets the stage for a forward earnings ramp that the current $211.62 share price does not fully price in.

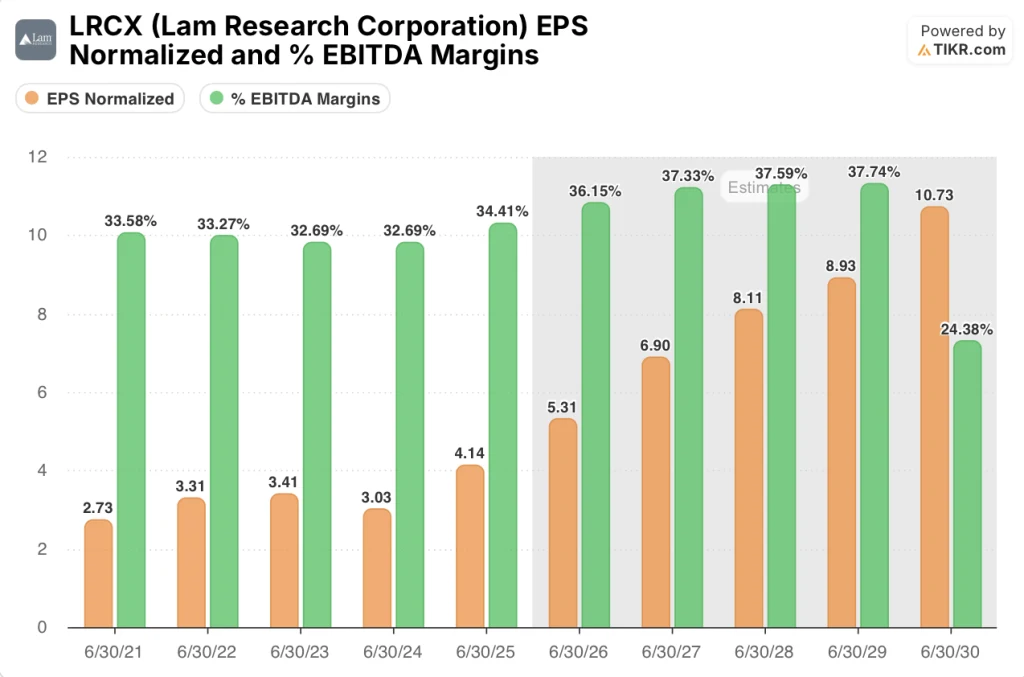

The TIKR model projects normalized EPS accelerating from $4.14 in FY2025 to $5.31 in FY2026 and $6.90 in FY2027, compound annual growth of roughly 29%, anchored by the 23% WFE industry expansion Lam itself forecast on the January 28 earnings call and the foundry/logic segment that already flipped to 59% of systems revenue.

EBITDA margins are also expected to widen from 34.4% in FY2025 to 36.2% in FY2026 and 37.3% in FY2027, a trajectory supported by the close-to-customer Malaysia manufacturing strategy CFO Doug Bettinger confirmed is already flowing through the P&L, and by CSBG, the installed-base service and spare parts business, now sitting at 102,000 chambers and growing every year.

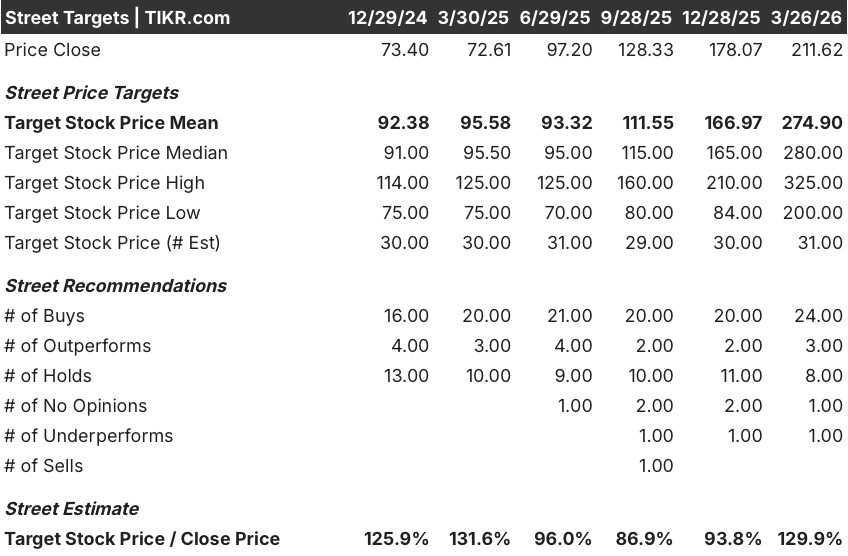

The 24 buy ratings, 3 outperforms, 8 holds, and 1 underperform among 36 analysts covering LRCX reflect near-consensus conviction in the AI-driven WFE upcycle, with a mean price target of $274.9 implying 29.9% upside from the March 26 close, as analysts specifically anticipate sustained DRAM and advanced packaging spending through the second half of 2026.

The analyst target range runs from $200.00 on the low end to $325.00 on the high end, a $125 spread that captures the primary binary: either clean room space constraints ease faster than expected, accelerating the $135 billion 2026 WFE figure toward the unconstrained demand level management described as meaningfully higher, or those constraints persist longer and compress the near-term revenue ramp.

What Does the Valuation Model Say?

The TIKR mid-case model prices LRCX at $256.18 by June 2030, implying a 21.1% total return and a 4.6% annualized IRR over 4.3 years, assuming 13.6% revenue CAGR and net income margins expanding to 29.1%, inputs grounded in the $40 billion NAND upgrade cycle accelerating ahead of schedule and the advanced packaging business growing more than 40% in 2026.

The market appears to be discounting the durable, compounding nature of CSBG, which generated $7.2 billion in 2025 and grows regardless of whether customers buy new tools, and which alone covers Lam’s annual dividend commitments while the equipment cycle does the heavy lifting.

The advanced packaging revenue line, anchored by the Syndion and SABRE 3D tools that Bettinger confirmed carry near-total market ownership in through-silicon-via processing, directly validates the model’s margin expansion assumption, since higher-intensity applications command better economics.

The key signal is that management’s own $135 billion WFE forecast, the most aggressive in the peer group, arrived alongside disclosed customer conversations extending visibility into 2027, a level of forward transparency Bettinger described as the best he has ever seen.

China revenue declining from 35% in the December quarter toward the low 30s as a percentage of total breaks the model if geopolitical escalation beyond existing U.S. end-user restrictions cuts deeper into the non-restricted Chinese customer base, where Lam currently maintains strong share via the Reliant mature product line.

The March 2026 quarter revenue print against the $5.7 billion midpoint guidance is the nearest confirmation point: meeting or exceeding that number while holding gross margin at or above 49% would validate that customer mix headwinds are manageable and that the second-half 2026 acceleration is on track.

Should You Invest in Lam Research Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LRCX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Lam Research Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze LRCX stock on TIKR for Free →