Key Stats for Zeta Stock

- Past-Week Performance: -21.8%

- 52-Week Range: $10.7 to $24.9

- Current Price: $14.6

What Happened?

Zeta Global (ZETA) delivered its 18th consecutive beat-and-raise quarter in Q4 2025, with the AI-powered marketing cloud platform posting $395 million in revenue, up 28% organically, while net revenue retention hit a record 120%, signaling that existing enterprise clients are accelerating spending even before Athena, the company’s conversational AI marketing agent, reaches general availability.

On February 24, CEO David Steinberg raised the FY 2026 revenue guidance midpoint by $25 million to $1.755 billion, representing 35% growth, after Q4 revenue beat the LSEG consensus of $379.2 million by $15.8 million and adjusted EBITDA of $95.1 million cleared guidance by $4 million.

The operational case rests on a customer flywheel that is visibly compounding: super-scaled customers, those spending over $1 million annually, grew 24% year-over-year to 184, multi-use case adoption among scaled customers surged 80% year-over-year in Q4, and clients on the platform five or more years now average $3.9 million in annual spend, up 39%, a cohort expansion pace that dwarfs the roughly 10% industry growth rate cited by management.

Moreover, Steinberg stated on the Q4 2025 earnings call that “net revenue retention hit a record high of 120% and in 2025, up from 114% in 2024,” then added that RFP volume more than doubled year-over-year to a new record, underscoring that both existing clients and new prospects are accelerating engagement simultaneously.

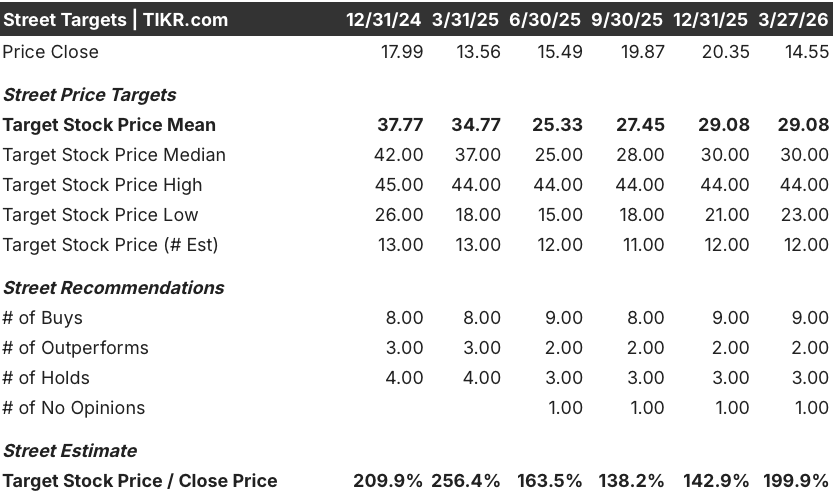

Zeta’s updated 2028 targets, lifted after the Marigold enterprise acquisition closed, now call for at least $2.3 billion in revenue, $573 million in adjusted EBITDA at a 25% margin, and $371 million in free cash flow, while an active buyback program with roughly $139 million remaining and Athena’s general availability targeted for the end of March 2026 together position the company to close the gap between its $14.55 current share price and the $30.00 median analyst price target as platform monetization scales.

Wall Street’s Take on ZETA Stock

The record 120% net revenue retention rate, the clearest measure of whether existing enterprise clients are expanding or retreating on the Zeta Marketing Platform, confirms the 18th consecutive beat-and-raise quarter was structural, not seasonal, and strengthens the forward revenue trajectory already embedded in the raise.

TIKR models FY 2026 revenue at $1.76 billion (+34.7% YoY), expanding to $2.04 billion in FY 2027, both supported by the 80% YoY surge in multi-use case adoption that historically drives 5x greater spend per customer versus single-use case relationships.

FCF also expanded from a 9.2% margin in FY 2024 to 12.6% in FY 2025, and TIKR projects that margin reaching 13.1% in FY 2026 and 14.2% in FY 2027, driven by Marigold operating leverage and continued EBITDA-to-FCF conversion improvement.

Eleven of 14 analysts currently rate ZETA a buy or strong buy, with a mean price target of $29.08 and a median of $30.00, implying roughly 100% upside from the March 27 close of $14.55, a consensus anchored to the 35% revenue growth guide and the first-ever positive GAAP net income year ahead.

The spread between the analyst low of $23.00 and high of $44.00 maps directly to two competing outcomes already in the story: the bear case rests on Athena adoption disappointing and Marigold failing to scale beyond its $190 million conservative revenue floor, while the bull case reflects Athena-driven ARPU expansion and further One Zeta multi-use case penetration above the current 25% of the scaled customer base.

What Does the Valuation Model Say?

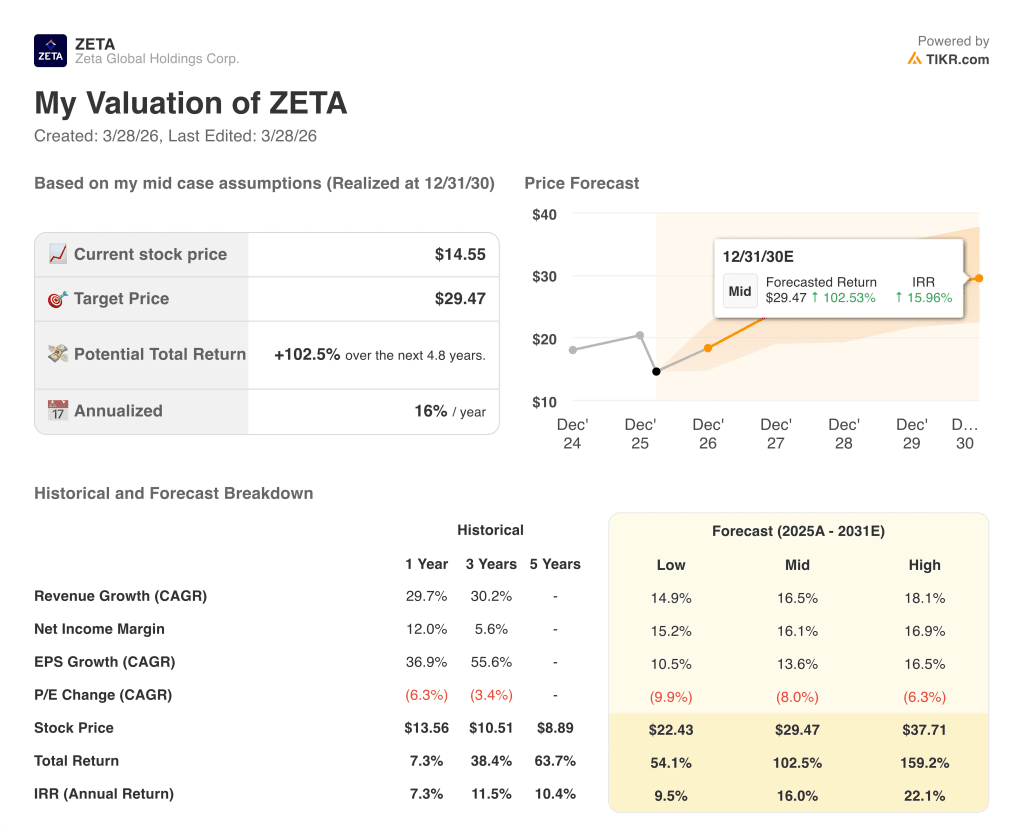

The TIKR mid-case target of $29.47, implying a 102.5% total return and a 16% annualized IRR through December 2030, assumes a 16.5% revenue CAGR and a 16.1% net income margin, both grounded in the demonstrated cohort behavior where five-plus-year customers already average $3.9 million in annual spend, up 39% year-over-year.

The market appears to be pricing ZETA as if growth is decelerating, yet the company just delivered its third consecutive year of 30%-plus revenue expansion and a 40% adjusted EBITDA increase, with FCF up 78%.

Super-scaled customer ARPU of $1.8 million per quarter, growing at a mid-teens rate when normalized for political revenue, directly supports TIKR’s $29.47 mid-case price target by anchoring the revenue base to sticky, expanding enterprise relationships rather than transactional volume.

CEO David Steinberg confirmed on the Q4 earnings call that Athena early users are “spending materially more” on the platform, a signal that TIKR’s conservative de minimis Athena revenue assumption for 2026 likely understates the true consumption upside.

The key risk is that Marigold’s $190 million revenue contribution, assumed conservatively, stalls below that floor if enterprise cross-sell timelines extend beyond year one, which would compress the EBITDA margin trajectory and delay the 22.3% margin target that underpins the 2026 model.

Athena’s general availability, targeted by end of March 2026, is the single nearest-term confirmation event; watch for Q1 2026 super-scaled ARPU and multi-use case adoption figures to determine whether Athena is accelerating the One Zeta flywheel on schedule.

Should You Invest in Zeta Global Holdings Corp.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ZETA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Zeta Global Holdings Corp. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ZETA stock on TIKR for Free →