Key Stats for SNOW Stock

- Past-Week Performance: -7%

- 52-Week Range: $120 to $281

- Valuation Model Target Price: $308

- Implied Upside: 104%

Analyze your favorite stocks like Snowflake with TIKR (It’s free) >>>

What Happened?

Snowflake has become a key battleground in the AI data platform space in 2026, as investors debate whether strong demand for AI workloads can offset a clear slowdown from its earlier hypergrowth phase.

Snowflake’s platform allows companies to store, analyze, and share large amounts of data in the cloud, which becomes increasingly valuable as AI models require more data to operate. Competition is intensifying from Databricks, as well as cloud platforms like Amazon Web Services and Microsoft Azure, all of which are expanding their own data and AI capabilities.

This week, that tension weighed on sentiment, and the stock fell about 7% to around $151 per share.

The stock moved lower primarily because multiple large investors reduced positions and insiders sold shares, which directly increased selling pressure and signaled weaker near-term conviction during the week. Filings showed Norden Group cut its stake by 84.5%, Assenagon Asset Management reduced its position by 36.8%, and Nepsis Inc. lowered exposure by 16.9%, while Hudson Bay Capital also trimmed its holdings.

At the same time, former CEO Frank Slootman executed multiple large share sales in March and EVP Christian Kleinerman sold shares at about $170, reinforcing the negative momentum as more shares were supplied to the market.

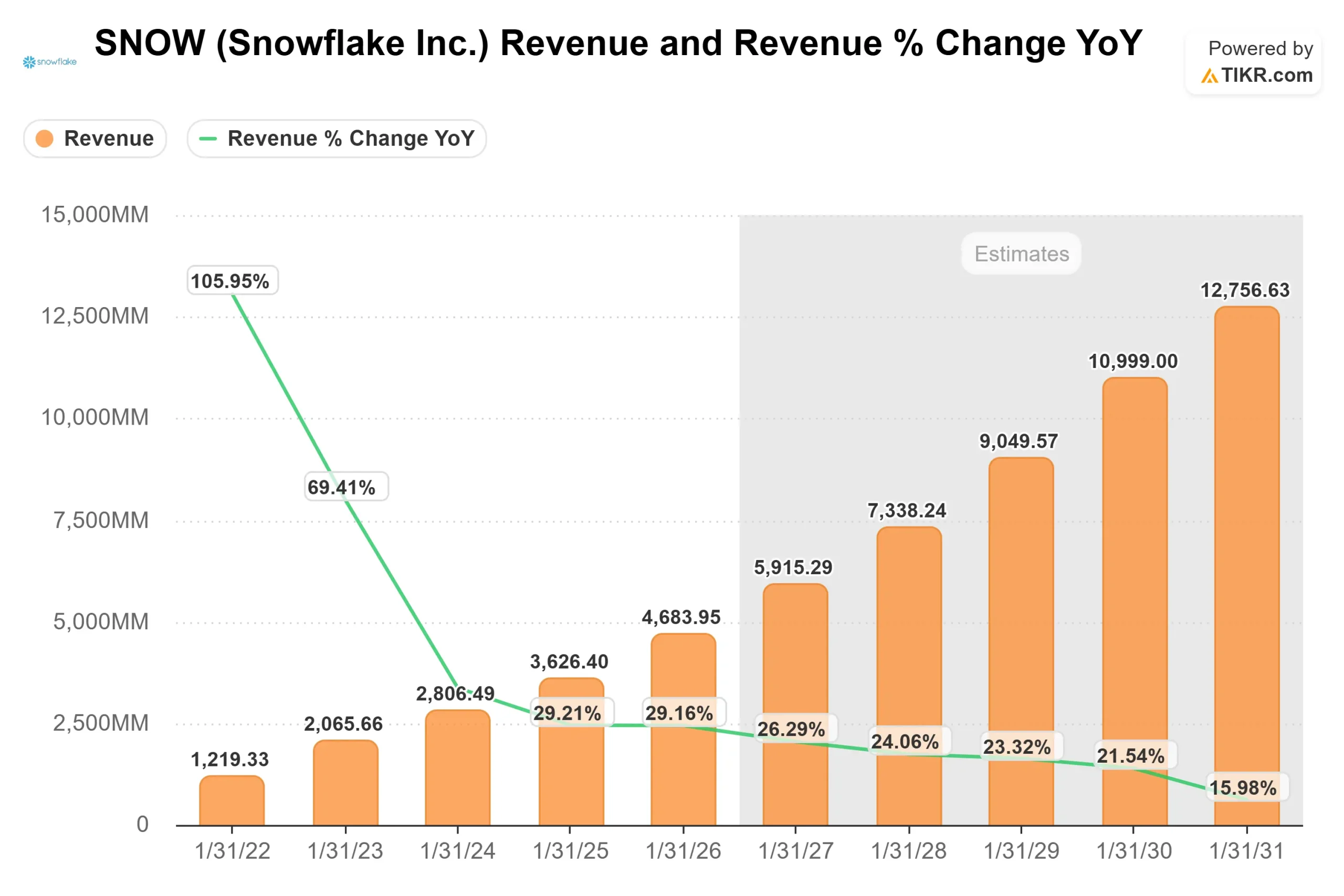

Last month, Snowflake highlighted improving business momentum at the Morgan Stanley TMT Conference, with management noting product revenue growth reaccelerated to about 30% alongside a $9.8 billion RPO balance growing 42% year over year, which points to strong forward revenue visibility.

Demand was supported by large enterprise expansions, including one deal over $400 million and seven additional nine-figure deals from existing customers increasing usage.

CEO Sridhar Ramaswamy stated that “products like Snowflake Intelligence are demonstrating how much more value you can get from data,” highlighting how AI-driven workloads are beginning to drive higher consumption across the platform.

Despite these positives, the stock remains under pressure as investors reassess Snowflake’s growth profile in 2026, especially as revenue growth has normalized into the mid-20% range after earlier hypergrowth.

Because Snowflake’s consumption-based model ties revenue directly to customer usage, even small changes in spending patterns or optimization efforts can impact near-term results, making the stock more sensitive to shifts in sentiment despite strong long-term demand.

Value Snowflake instantly (Free with TIKR) >>>

Is SNOW Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 24.5%

- Operating Margins: 14.7%

- Exit P/E Multiple: 84.2x

Snowflake’s growth is increasingly driven by expansion within its existing customer base, as enterprises centralize data and run AI and analytics workloads on its platform, where higher data usage directly increases revenue through its consumption-based pricing model.

See analysts’ growth forecasts and price targets for Snowflake (It’s free) >>>

A key driver in 2026 is the scaling of AI workloads, which require significantly more data processing and storage, increasing spending per customer as these use cases move into production and move beyond early experimentation.

At the same time, competition from Databricks and cloud-native platforms like Amazon Web Services and Microsoft Azure means Snowflake must continue improving performance, pricing efficiency, and ease of use to maintain share in the rapidly evolving data infrastructure market.

Based on these inputs, the model estimates a target price of $308, implying about 104% total upside over roughly 2.8 years, indicating the stock appears undervalued at current levels.

At current levels, Snowflake appears undervalued, with future performance driven by AI-driven consumption growth, competitive positioning, and improving operating leverage as the business scales.

How Much Upside Does SNOW Stock Have From Here?

Investors can estimate Snowflake’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Snowflake in under 60 seconds with TIKR (It’s free) >>>