Key Stats for Adobe Stock

- Past-30-Day Performance: -7%

- 52-Week Range: $233 to $423

- Valuation Model Target Price: $317

- Implied Upside: 31%

Analyze your favorite stocks like Adobe with TIKR (It’s free) >>>

What Happened?

Adobe is increasingly being viewed as a battleground between legacy creative software and the rise of AI-native tools, as investors debate whether the company can maintain its pricing power and premium positioning in a rapidly evolving market. That uncertainty has weighed on sentiment, even as the company continues to report solid financial results.

Adobe Inc. stock is down about 7% over the past 30 days, trading near $243 per share, primarily because investors are reacting to a faster-than-expected decline in Adobe’s high-margin stock content business and uncertainty around how quickly its AI products can generate meaningful revenue to offset that pressure.

At the same time, generative AI tools are making design and content creation more accessible and integrated into everyday software workflows, raising concerns that Adobe’s premium pricing model could face pressure over time.

Competitors like Canva are gaining traction with simpler, lower-cost tools for casual users, while Microsoft is embedding AI design features into products like Office and Copilot, and OpenAI is expanding tools like ChatGPT with image and content generation capabilities, increasing pressure on Adobe’s core creative software ecosystem.

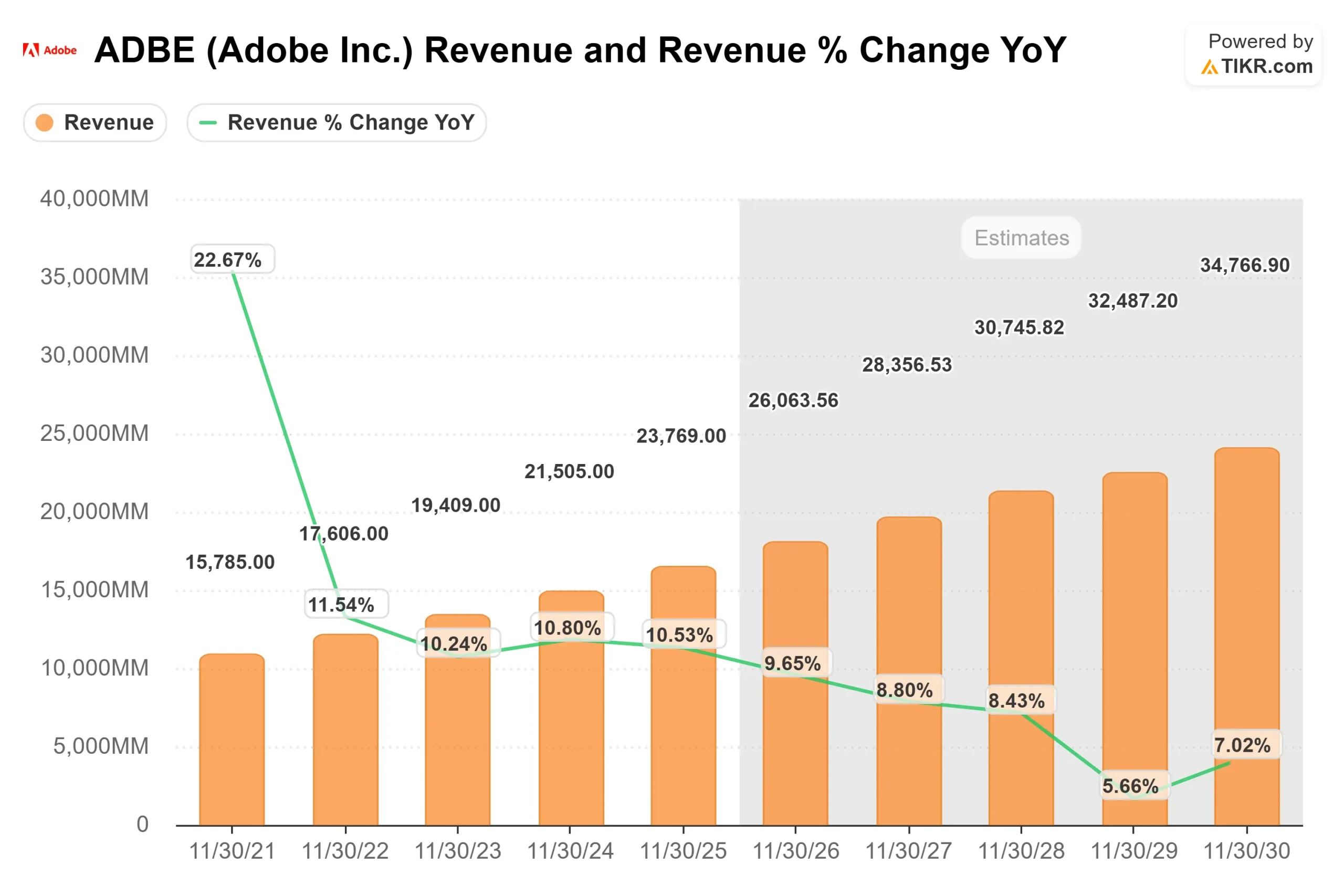

Earlier this month, Adobe reported Q1 fiscal 2026 results with revenue of $6.4 billion, up 12% year over year, while GAAP EPS reached $4.60 and non-GAAP EPS came in at $6.06. The company also surpassed 850 million monthly active users across Acrobat, Creative Cloud, Express, and Firefly, its generative AI platform that allows users to create images, video, and design content using text prompts.

CEO Shantanu Narayen said Adobe had a “strong start to the year,” although management noted that its traditional stock content business, a higher-margin segment where users pay for licensed images, declined faster than expected as customers increasingly shift toward AI-generated alternatives.

Analyst commentary remained mixed during the period, reflecting uncertainty around AI monetization and competitive positioning. Institutional activity also showed divergence, with Spire Wealth Management cutting its stake by 67%, Canoe Financial reducing its position by 61%, and Davenport & Co trimming its holdings by 32%.

At the same time, other investors added exposure, including Norden Group increasing its stake by 169% and Global X Japan raising its position by 48%, leaving institutional ownership at about 82% and highlighting a split view on Adobe’s near-term outlook.

Value Adobe instantly (Free with TIKR) >>>

Is Adobe Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 9%

- Operating Margins: 45%

- Exit P/E Multiple: 10x

Adobe’s growth outlook is supported by steady demand for Creative Cloud, which includes industry-standard tools like Photoshop and Illustrator, alongside expanding monetization of Firefly, its AI platform that allows users to generate and edit content directly within Adobe’s ecosystem.

See analysts’ growth forecasts and price targets for Adobe (It’s free) >>>

This positions Adobe differently from competitors like Canva, which focuses on simplicity and lower-cost tools for casual users, while Adobe continues to target professionals and enterprises that require advanced functionality, precision, and workflow integration, supporting stronger long-term pricing power.

AI remains the most important driver, as increased usage of generative tools and credit-based pricing could raise average revenue per user while helping Adobe defend its competitive position despite growing competition from Microsoft and OpenAI.

Enterprise demand also supports growth, particularly as large organizations adopt Adobe’s tools to automate marketing content and manage customer experiences at scale, which tends to generate more stable and higher-value recurring revenue.

Based on these inputs, the model estimates a target price of $317, implying about 31% total upside over the next 2.7 years, suggesting the stock appears undervalued at current levels.

At current levels, Adobe appears undervalued, with future performance driven by its ability to monetize AI, maintain pricing power, and sustain its competitive advantage as creative workflows evolve.

How Much Upside Does Adobe Stock Have From Here?

Investors can estimate Adobe’s potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.