Key Takeaways:

- Super Micro continues scaling revenue rapidly, reaching $28.1 billion LTM as AI server demand accelerates.

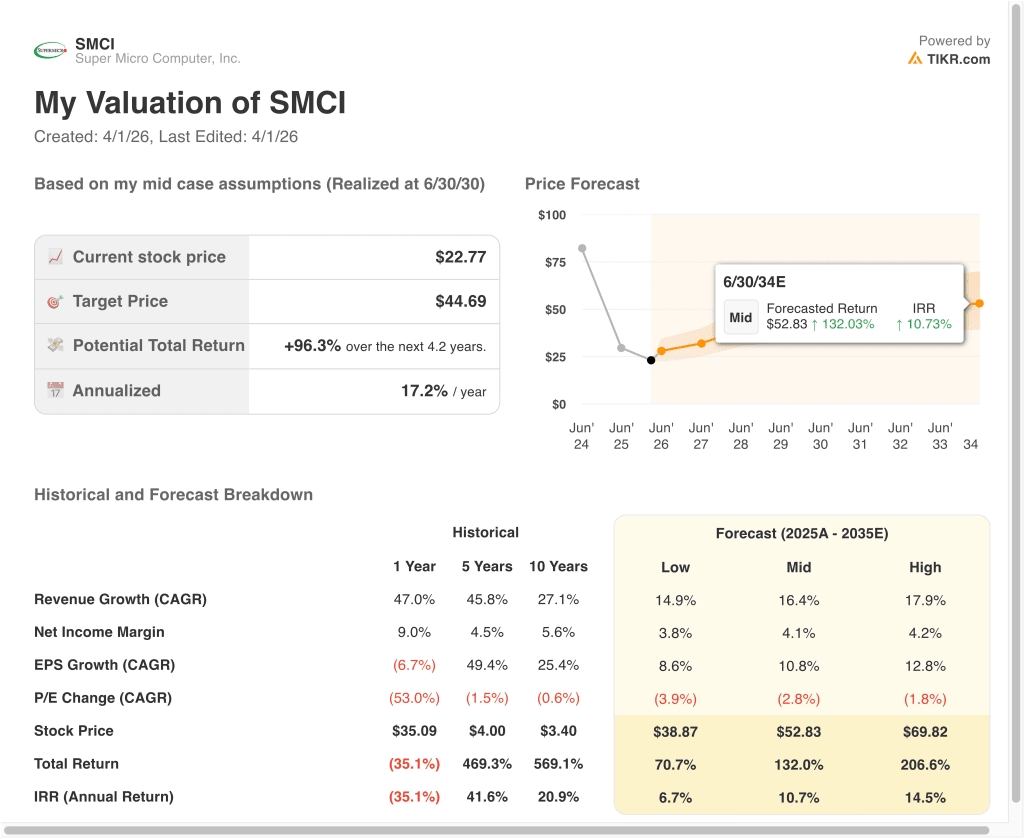

- SMCI stock could reasonably reach $34 per share by June 2028, based on our valuation assumptions.

- This implies a total return of 52.6% from today’s price of $22.77, with an annualized return of 20.6% over the next 2.2 years.

What Happened?

Super Micro Computer, Inc. (SMCI) has been under pressure following a series of regulatory and governance-related developments that shifted investor sentiment in March 2026. The stock dropped sharply after U.S. authorities charged individuals tied to the company in a case involving the alleged smuggling of AI chips to China. While the company stated it was not named in the indictment, the headlines triggered a selloff and raised concerns about compliance risk.

At the same time, corporate governance changes added to uncertainty. A co-founder stepped down from the board, and the company appointed a new acting chief compliance officer. These moves suggest management is responding to regulatory scrutiny, but they also reinforce investor caution in the near term.

Despite these issues, demand for Super Micro’s products remains strong. The company continues to benefit from AI infrastructure growth, including partnerships tied to NVIDIA’s latest AI platforms and liquid-cooled data center solutions. Super Micro’s presence at major events like NVIDIA’s GTC AI Conference highlights its role in enabling next-generation AI workloads.

However, the stock has declined significantly, down over 50% in recent months. Investors appear to be balancing strong revenue growth with concerns about margins, governance, and execution risk.

Here’s why Super Micro stock could re-rate if growth remains strong and operational risks stabilize.

What the Model Says for SMCI Stock

We analyzed the upside potential for Super Micro stock using valuation assumptions based on its leadership in AI server infrastructure, strong revenue growth driven by hyperscaler demand, and expanding role in liquid-cooled data center deployments.

Based on estimates of 37.0% annual revenue growth, 5.1% operating margins, and a normalized P/E multiple of 7.0x, the model projects Super Micro stock could rise from $22.77 to $34.75 per share.

That would be a 52.6% total return, or a 20.6% annualized return over the next 2.2 years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for SMCI stock:

1. Revenue Growth: 37%

Super Micro has delivered exceptional revenue growth, with total revenue reaching $28.1 billion LTM. Revenue more than doubled in 2024 and continued growing 46.6% in 2025, driven by strong demand for AI servers and data center infrastructure. This reflects the company’s positioning within one of the fastest-growing segments in technology.

The company benefits from close alignment with AI chip providers and hyperscale customers. Its modular server architecture allows faster deployment and customization, which is critical for AI workloads. This has enabled Super Micro to scale faster than many traditional hardware peers.

Based on analysts’ consensus estimates, we use a 37.0% forecast, reflecting continued AI infrastructure demand, strong backlog visibility, and expansion into liquid-cooled solutions, balanced against potential normalization in growth rates.

2. Operating Margins: 5.1%

While revenue growth has been strong, margins have compressed over time. Gross margins declined to 8.0% LTM, while operating margins fell to 3.7%, reflecting higher component costs and competitive pricing pressures. This highlights the capital-intensive nature of the hardware business.

Operating income still reached over $1.0 billion LTM, but growth has slowed compared to revenue expansion. This indicates that scaling revenue does not fully translate into higher profitability due to cost pressures and investment needs.

Based on analysts’ consensus estimates, we use 5.1% operating margins, reflecting modest improvement from current levels as supply chains stabilize and efficiency improves, balanced against continued pricing pressure in AI infrastructure markets.

3. Exit P/E Multiple: 7x

Super Micro currently trades at a relatively low forward multiple compared to high-growth AI peers. The lower multiple reflects uncertainty around margins, governance risks, and earnings volatility. Investors appear to be discounting these risks despite strong top-line growth.

Compared to software or AI chip companies, hardware providers typically trade at lower multiples due to cyclicality and lower margins. This is consistent with Super Micro’s current valuation profile.

Based on analysts’ consensus estimates, we maintain a 7.0x exit multiple given the company’s hardware exposure, margin variability, and current market sentiment, balanced against strong revenue growth and AI positioning.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Different scenarios for Super Micro stock through 2028 show varied outcomes based on revenue growth, margin execution, and valuation discipline (these are estimates, not guaranteed returns):

- Low Case: AI demand slows, and margins remain compressed → 6.7% annual returns

- Mid Case: Super Micro continues scaling AI infrastructure with stable margins → 10.7% annual returns

- High Case: Strong demand and margin expansion drive higher earnings growth → 14.5% annual returns

Super Micro’s future will depend on how it balances rapid growth with profitability and compliance execution. The company is positioned in a structurally growing market, but near-term risks remain elevated due to recent developments.

If management stabilizes governance concerns and improves margins, valuation could gradually normalize alongside earnings growth.

See what analysts think about SMCI stock right now (Free with TIKR) >>>

Should You Invest in Super Micro Computer, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SMCI, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SMCI alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Super Micro stock on TIKR Free→

Looking for New Opportunities?

- See what stock billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!