Key Stats for Fifth Third Stock

- Past-Week Performance: +0.8%

- 52-Week Range: $32.3 to $55.4

- Current Price: $44.7

What Happened?

Fifth Third Bancorp (FITB), a Cincinnati-based regional bank now ranked 9th largest in the U.S. after closing its $12.7 billion all-stock Comerica acquisition on February 1, posted record full-year net interest income of $6.0 billion in 2025 while trading at $44.68, well below its 52-week high of $55.44, as investors weigh near-term integration noise against a platform that targets 19% return on tangible common equity and a sub-53% efficiency ratio by Q4 2026.

On March 13, Truist Securities cut its price target on FITB to $53 from $60, flagging Q1 2026 net interest income guidance of $1.93 billion as softer than expected for a stock Wall Street had positioned as a “beat and raise” story, though 16 of 22 analysts still rate the shares “strong buy” or “buy” against a median target of $57 per LSEG data.

Beneath the Q1 noise, the combined franchise is already tracking ahead of its original integration plan, with Fifth Third now guiding to at least $400 million in expense synergies in 2026 versus an initial target of $320 million, while the Southeast de novo branch program, which opens branches in high-growth markets to gather low-cost retail deposits, hit a 2025 vintage performance of 213% of its deposit goal and continues to accelerate ahead of any regional peer benchmark.

On February 11 at the Bank of America Financial Services Conference, COO James Leonard stated that “each vintage, we are tweaking things, we’re getting better partners, we’re focused on opening these branches where people live, work or shop,” anchoring confidence in the same playbook Fifth Third now deploys across 43 secured Texas locations targeting the Dallas, Houston, and Austin markets.

Fifth Third’s embedded payments platform Newline, which lets financial technology companies build payments infrastructure directly on Fifth Third’s balance sheet for fee and deposit revenue without credit extension, more than doubled its revenue year-over-year in Q4 2025 and reached $4.3 billion in linked deposits, adding a capital-light growth engine alongside the $500 million in identified five-year revenue synergies, 150 planned Texas branches by 2029, and an expected resumption of $300 to $500 million in quarterly share repurchases once integration charges clear in the second half of 2026.

Wall Street’s Take on FITB Stock

The Comerica close on February 1 is the direct mechanism behind TIKR’s estimate of 42.7% revenue growth in 2026, as Fifth Third’s combined platform, now at roughly $290 billion in assets, absorbs $850 million in annualized expense synergies and at least $400 million in 2026 alone.

FITB’s Normalized EPS is estimated to jump from $3.64 in 2025 to $4.07 in 2026 and $4.91 in 2027, as TIKR estimates, driven by $8.6 to $8.8 billion in net interest income from a combined loan book targeting the mid-$170 billion range.

Twelve buys and five outperforms among 21 analysts push the street mean price target to $56.62, implying 26.7% upside from the March 30 close of $44.68, as analysts price in successful integration execution and the 19% ROTCE target Fifth Third now targets for Q4 2026.

The analyst price target range spans $49 on the low end to $67 on the high end, where the low anchors to persistent integration disruption and Q1’s softer $1.93 billion NII print, while the high reflects full realization of $850 million in synergies and 150 Texas branches ramping by 2029.

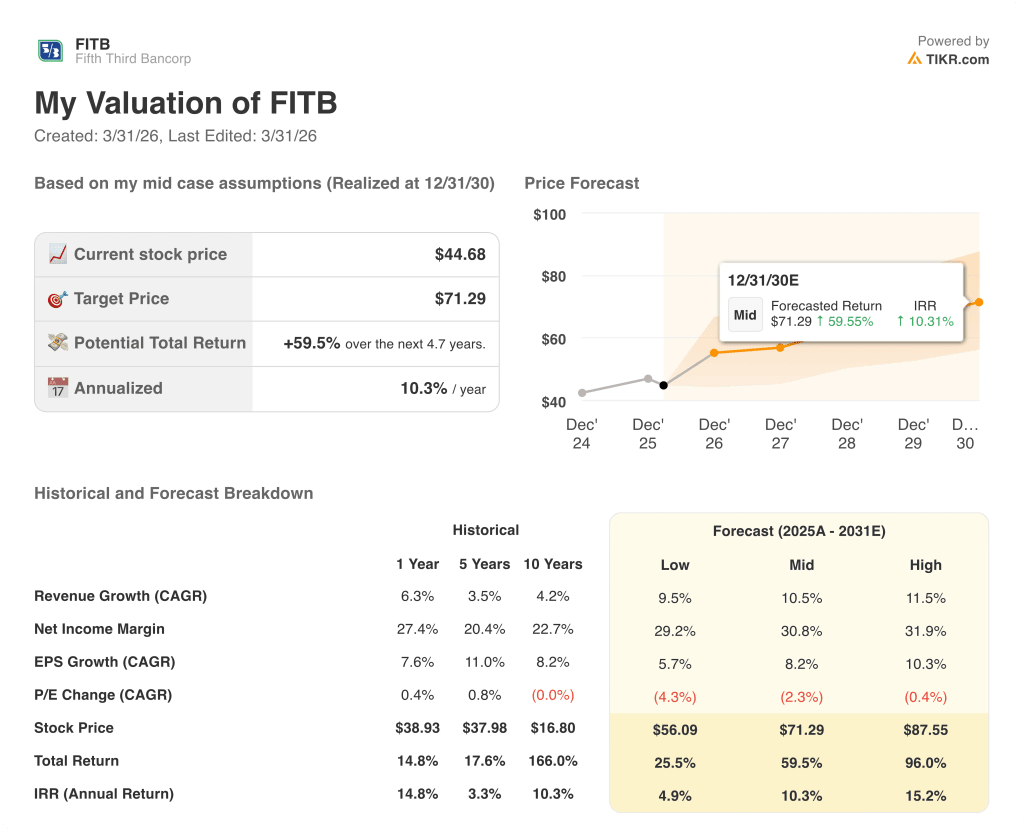

What Does the Valuation Model Say?

As TIKR estimates, the mid-case price target of $71.29 by December 2030 implies a 59.5% total return and 10.3% IRR, grounded in a 10.5% revenue CAGR and net income margin expansion to 30.8%, supported by the Newline embedded payments platform’s capital-light deposit and fee growth already showing $4.3 billion in linked deposits.

FITB trades at roughly 11x 2026 normalized EPS of $4.07 and 9.1x 2027 normalized EPS of $4.91, well below the 13x to 15x forward P/E regional bank compounders typically command at equivalent or better growth; undervalued, with 20.5% EPS growth arriving in 2027.

The TIKR model’s $71.29 mid-case target is supported by the Southeast de novo program already running at 213% of deposit goals and Texas site acquisition underway, establishing the organic growth runway that underwrites the 10.5% revenue CAGR assumption.

Management’s own Q4 2026 efficiency ratio target of below 53% and 19% ROTCE, accelerated from the original 2027 timeline, signals the investment thesis is ahead of schedule, not behind it.

The model breaks if Tricolor-linked litigation materially escalates or if commercial line utilization, which dipped to 35% in Q4 2025, fails to normalize, compressing 2026 NII below the $8.6 billion floor.

Q1 2026 earnings in early April are the first real-time read on whether the $1.93 billion NII print holds and whether Comerica integration attrition in commercial relationships remains as limited as management indicated through February.

Should You Invest in Fifth Third Bancorp?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FITB stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Fifth Third Bancorp alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze FITB stock on TIKR for Free →