Key Stats for Raymond James Stock

- Past-Week Performance: -1.7%

- 52-Week Range: $117.6 to $177.7

- Current Price: $140.9

What Happened?

Raymond James Financial (RJF), a diversified wealth management and investment banking firm, posted its fifth consecutive year of record revenues and earnings while its adviser recruiting engine pulled in $69 billion in total client assets over the trailing 12 months, yet the stock trades at $140.89, well below its 52-week high of $177.66.

On January 28, RJF reported Q1 FY2026 record net revenues of $3.7 billion, up 6% year-over-year, with adjusted earnings per diluted share of $2.86 and an adjusted pretax margin of 20%, hitting the firm’s own publicly stated margin target despite a 125-basis-point rate cut headwind since November 2024.

Securities-based lending, a product that lets wealth clients borrow against their investment portfolios at floating rates, grew 28% annually and 10% in Q1 alone, lifting bank segment pretax income to a record $173 million and total loans to a record $53.4 billion, outpacing the broader industry’s loan growth trend.

In March, RJF closed its acquisition of GreensLedge Holdings, a structured credit boutique, while completing the announced acquisition of Clark Capital Management, an asset manager with over $46 billion in combined assets, broadening the firm’s Capital Markets and Asset Management segments simultaneously.

CEO Paul Shoukry stated on the Q1 FY2026 earnings call that “our sustained growth over time is a testament to the deep personal relationships our advisers, bankers and associates have with their clients, which is a foundation to providing tailored and trusted financial advice,” a posture now backed by $1 billion in annual technology investment and a newly launched AI operations agent named Rai built to automate adviser service workflows.

Raymond James’ competitive position over the next 3 to 5 years rests on a convergence of three structural drivers: a $2.4 billion excess capital base available for deployment, $400 million in targeted quarterly share repurchases sustaining EPS momentum, and a recruiting pipeline that added advisers carrying $460 million in trailing production at prior firms, up 21% from the prior year record.

Wall Street’s Take on RJF Stock

RJF’s record $3.7 billion Q1 revenue and simultaneous 20% adjusted pretax margin, achieved despite 125 basis points of rate cuts since November 2024, confirm the firm’s earnings engine is structurally more resilient than the current $140.89 stock price implies.

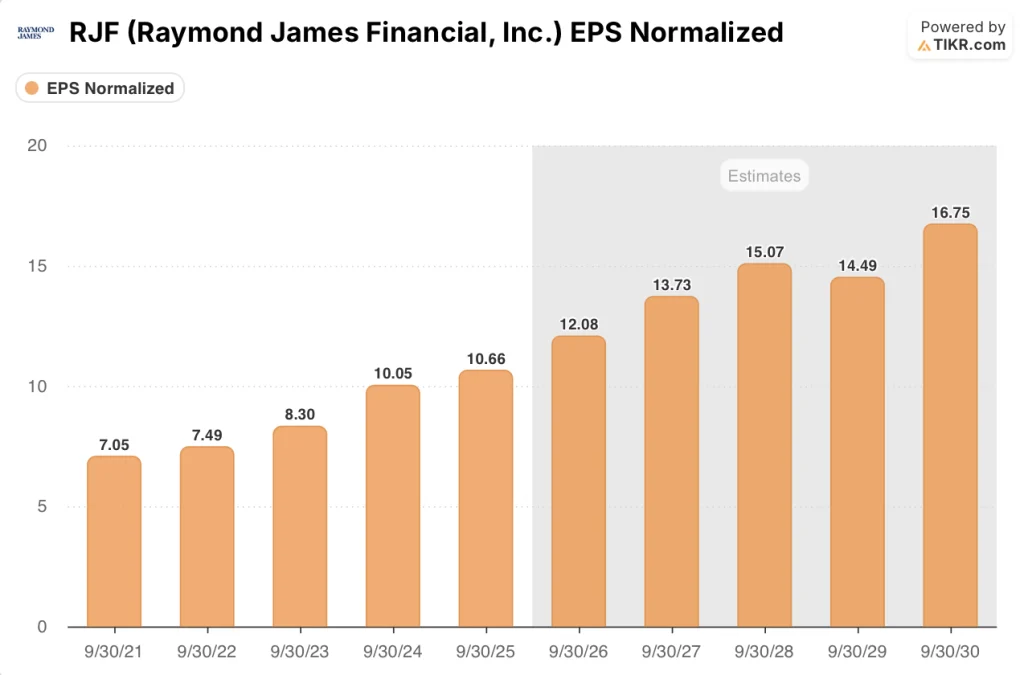

As TIKR estimates, normalized EPS grows from $10.66 in FY2025 to $12.08 in FY2026 and $13.73 in FY2027, a 13.3% two-year CAGR, supported by record securities-based lending growth of 28% and a $69 billion trailing recruiting haul that expands the fee-based asset base.

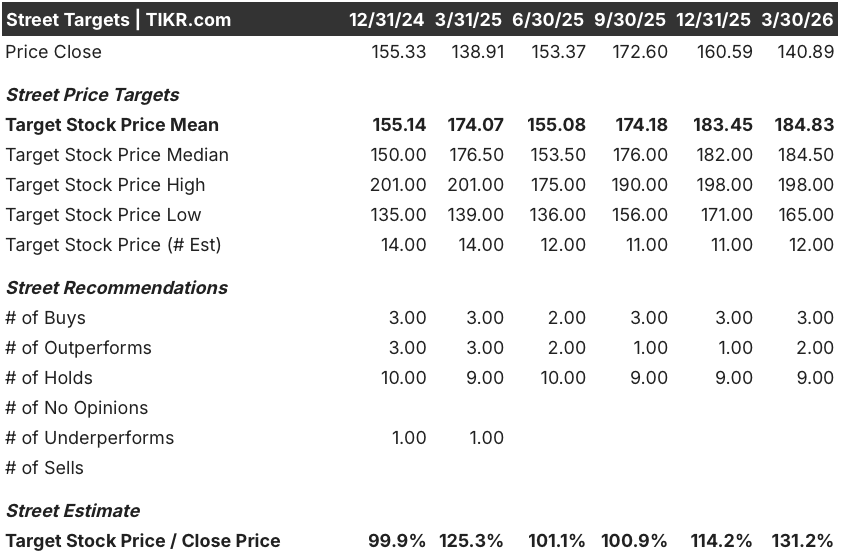

The consensus of 12 analysts carries a mean price target of $184.83, implying 31.2% upside from the March 30 close, with 3 buys, 2 outperforms, and 9 holds reflecting a Street that acknowledges the quality but waits for capital markets revenue to inflect from the Q1 trough of $380 million.

The analyst price target range spans $165 on the low end to $198 on the high, where the floor reflects sustained rate compression and soft M&A pull-through, and the ceiling prices in the investment banking pipeline recovery management described as “robust” entering Q2.

What Does the Valuation Model Say?

TIKR’s mid-case target of $199.42, built on a 5.8% revenue CAGR and a 15.4% net income margin, is directly supported by $69 billion in recruited client assets and a record $53.4 billion loan book that expands fee-based and interest-earning revenue simultaneously.

At 11.7x forward normalized EPS of $12.08, RJF trades at a steep discount to its own historical earnings growth rate of 21.2%, making it materially undervalued against the fundamentals already in motion.

A $69 billion trailing recruiting haul and record bank pretax income of $173 million underpin TIKR’s $199.42 price target, which assumes earnings compound steadily as fee-based assets and securities-based lending continue scaling.

Management committed to $400 million in quarterly repurchases while normalized EPS tracks 13.3% two-year growth, a capital return posture that signals the firm itself views the stock as undervalued at current levels.

A sharp deceleration in securities-based lending, which drove 28% annual loan growth and record bank segment income, would directly compress the net interest income assumption holding TIKR’s margin trajectory together.

The May or June Investor Day is the event to watch; updated margin guidance and capital deployment targets will confirm whether the 20% adjusted pretax margin holds as capital markets revenue recovers from $380 million.

Should You Invest in Raymond James Financial, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up RJF stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Raymond James Financial, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze RJF stock on TIKR for Free →