Key Stats for Ford Stock

- Past-Week Performance: -1.3%

- 52-Week Range: $8.4 to $14.8

- Current Price: $11.2

What Happened?

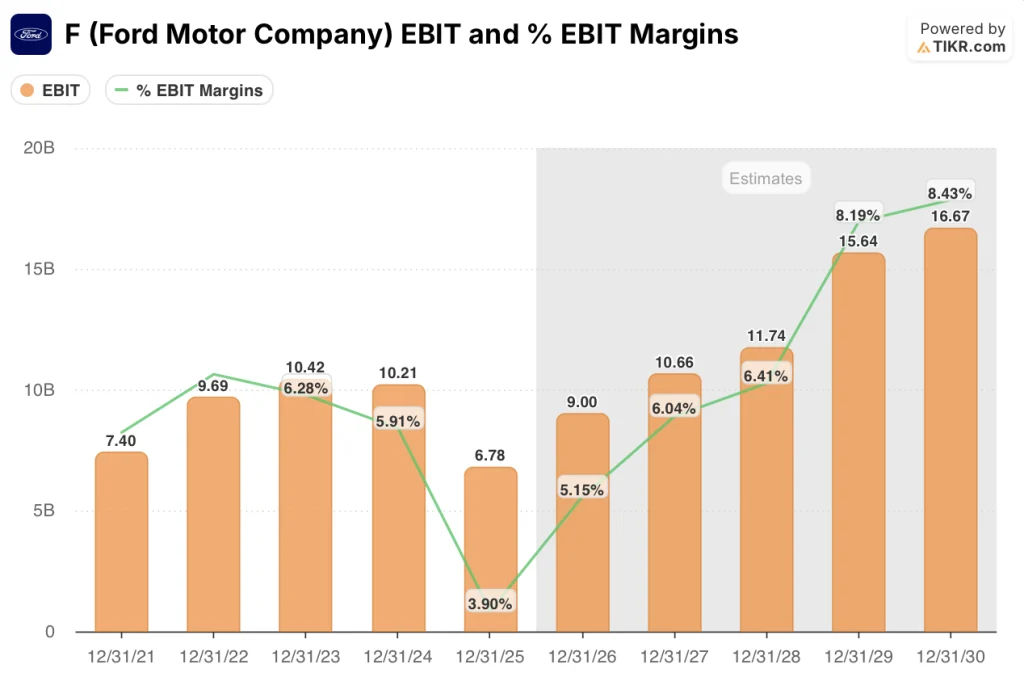

Ford Motor Company (F), the Dearborn automaker whose commercial vehicle and truck lineup generates the bulk of its earnings, enters 2026 trading at $11.21 against a 52-week high of $14.80 after posting $6.8 billion in adjusted earnings before interest and taxes for FY2025, a result distorted by $4 billion in combined headwinds from a Novelis aluminum mill fire and a late-year tariff credit timing change that alone cost Ford $1.9 billion and will not recur.

Ford’s Q4 2025 earnings report, released last February 10, revealed that stripping out the one-time tariff credit hit, full-year adjusted EBIT would have reached $7.7 billion, materially above the $6.0 billion to $6.5 billion range Ford guided at its Q3 update, with $1.5 billion in industrial cost reductions, primarily from material and warranty savings, driving the outperformance.

Ford Pro, the company’s commercial vehicle arm serving fleets, small businesses, and government customers, delivered $6.8 billion in EBIT on more than $66 billion in revenue at a double-digit margin, with U.S. Super Duty heavy-truck sales at their best level in over 20 years and paid software subscriptions, the recurring digital revenue layer Ford is building atop its vehicle sales, growing 30%.

Chief Executive Jim Farley stated on the Q4 2025 earnings call that “the earnings power of our business is accelerating, and our Ford+ strategy distinguishes us from the competition in clear ways,” a claim anchored by Ford’s 13.2% U.S. market share, its strongest showing in six years, and a 42% total shareholder return for the year.

Ford’s 2026 guidance of $8 billion to $10 billion in adjusted EBIT, underpinned by another $1 billion in targeted cost reductions, the Novelis hot mill restart expected between May and September, and the 2027 launch of its Universal EV Platform targeting the high-volume $30,000 to $35,000 segment, frames a business that is closing a structural cost gap while positioning its next product cycle to lift margins toward its stated 8% EBIT target by 2029.

Wall Street’s Take on F Stock

The $1.9 billion tariff credit timing hit that compressed Ford’s FY2025 EBIT to $6.8 billion is confirmed non-recurring, meaning the underlying business already ran closer to $7.7 billion and the 2026 guide of $8 billion to $10 billion reflects genuine operational momentum, not an easy base effect.

As TIKR estimates, Ford’s EBIT margin expands from 3.9% in FY2025 to 5.2% in FY2026 and 8.2% by FY2029, driven by $1 billion in annual cost reductions, Novelis volume recovery of 50,000 to 60,000 units, and sunset of low-margin nameplates including Escape.

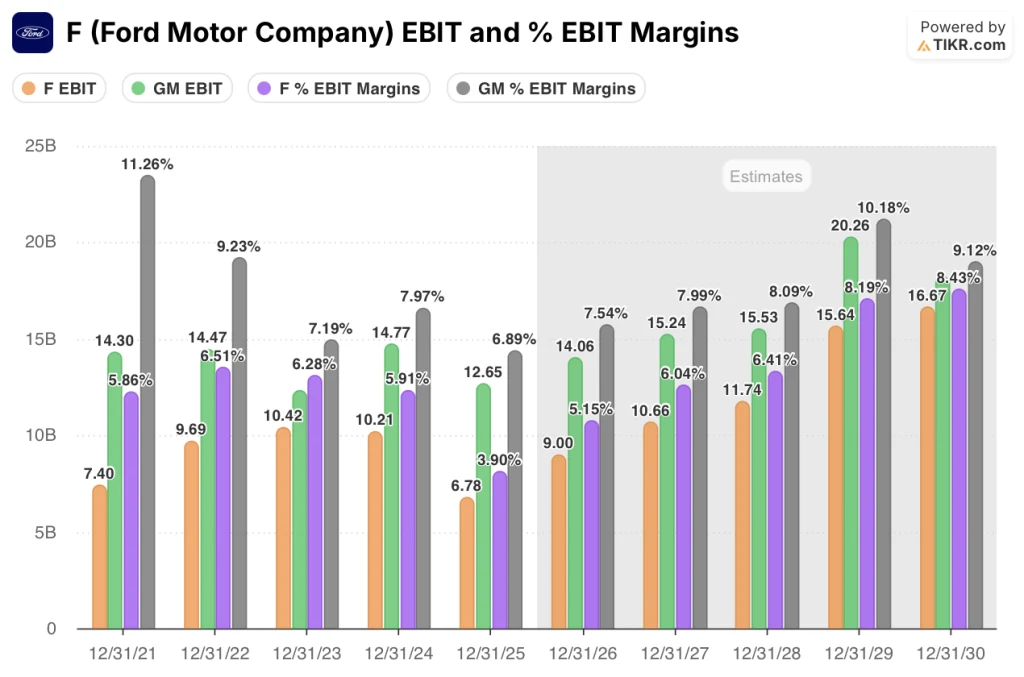

General Motors, Ford’s most direct rival in U.S. full-size trucks and commercial vehicles, posted a 6.9% EBIT margin on $185 billion in FY2025 revenue and itself appears undervalued at current levels, with TIKR’s model estimating a target price of roughly $85 implying approximately 16% upside, while Ford’s own EBIT margin trajectory, moving from 3.9% in FY2025 to a projected 6.0% by FY2027 and 8.2% by FY2029, is on a path to match and ultimately surpass that benchmark as cost reductions and mix improvement compound.

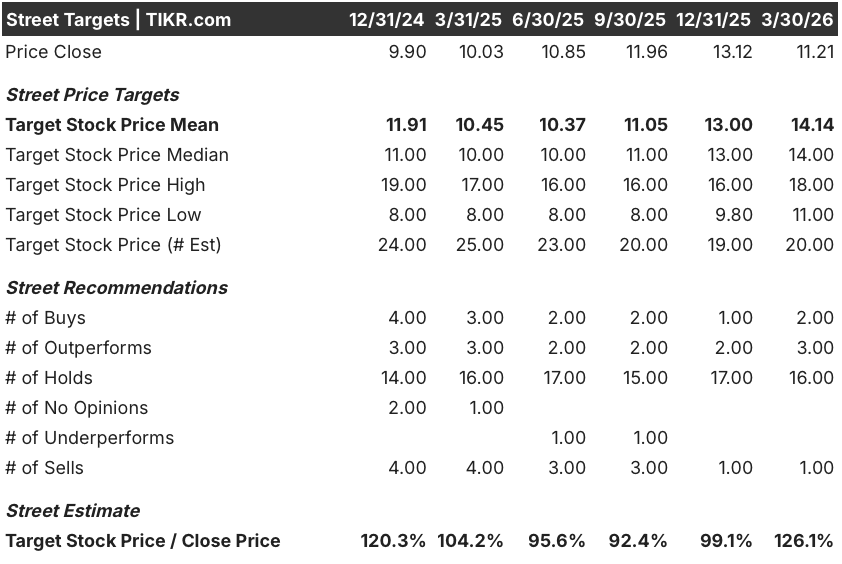

Wall Street’s conviction is building but remains cautious: with 2 buys, 3 outperforms, 16 holds, and 1 sell across 20 analysts, the mean price target of $14.14 implies 26.1% upside from $11.21, suggesting the Street acknowledges the recovery but has not yet fully priced the margin trajectory.

The spread between the $11.00 low target and $18.00 high target reflects a binary read on Novelis: bears anchoring near current levels assume extended aluminum supply disruptions and tariff pressure persist, while bulls pricing toward $18.00 assume the hot mill restarts by September and $1 billion in temporary costs drop off entirely in 2027.

What Does the Valuation Model Say?

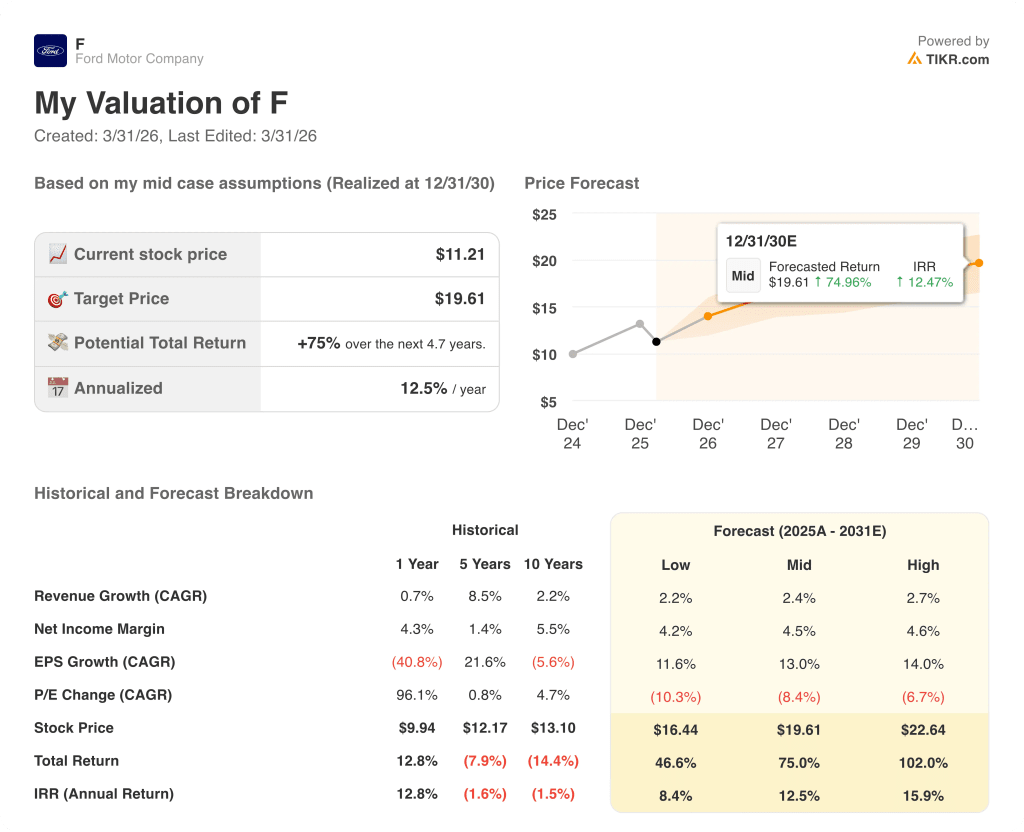

As TIKR estimates, Ford’s mid-case price target of $19.61 by December 2030 implies a 75% total return and 12.5% annualized IRR, supported by a 13% EPS compound annual growth rate from FY2025 to FY2030 as cost reductions, Pro segment software scaling, and UEV platform economics layer into the income statement.

The market is pricing Ford as though its 3.9% FY2025 EBIT margin is structural when $4 billion of that compression was explicitly non-recurring.

Ford’s $1.5 billion in FY2025 cost reductions, exceeding its own $1 billion target, confirms the cost trajectory is real and not yet reflected in the $11.21 share price.

Moreover, Ford COO Kumar Galhotra confirmed on March 18 that Novelis restart timing is actively monitored with contingency supply secured, signaling management confidence that the $1 billion year-over-year improvement in 2026 is not schedule-dependent.

A Novelis restart delay beyond September, or a second wave of aluminum tariff costs, would extend the $1.5 billion to $2 billion temporary cost burden into 2027 and push the 8% EBIT margin target further out.

Should You Invest in Ford Motor Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up F stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Ford Motor Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze F stock on TIKR for Free →