Key Stats for Travelers Stock

- Past-Week Performance: -3.8%

- 52-Week Range: $230.4 to $313.1

- Current Price: $192.8

What Happened?

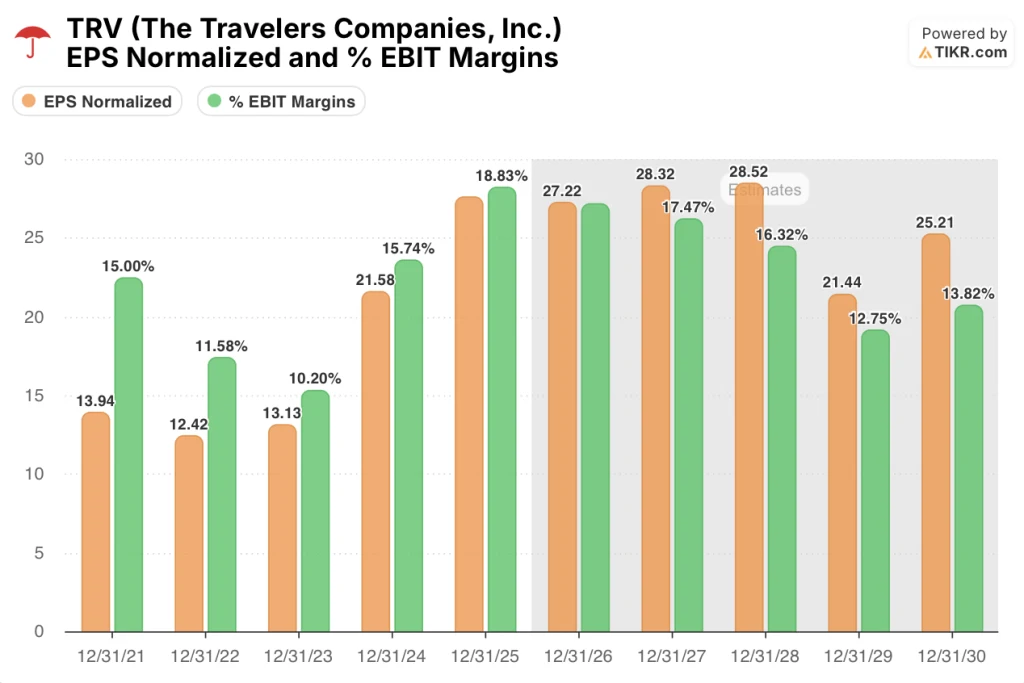

The Travelers Companies (TRV), a property and casualty insurer that sells commercial, specialty, and personal coverage across the U.S., posted full-year 2025 core income of $6.3 billion, up 26% year over year, while after-tax underlying underwriting income, the profit insurers generate before investment returns, grew to $5.5 billion, nearly tripling from $2.1 billion in 2022, with shares trading at $291.82.

On January 21, Travelers reported Q4 2025 core income of $2.5 billion or $11.13 per diluted share, with an underlying combined ratio, the metric measuring underwriting profitability where lower is better, of 82.2%, marking its fifth consecutive quarter below 85% and a roughly 2-point improvement from the prior year quarter.

Operating cash flow reached $10.6 billion in 2025, more than doubling the prior decade’s average of roughly $4 billion, as the company grew its investment portfolio, a key income source for insurers, by $7.5 billion to $106 billion at year-end.

Chairman and CEO Alan Schnitzer stated on the Q4 2025 earnings call that “over the past decade, we’ve grown our top line at a compound annual rate of 7% while improving our underlying profitability by almost 8 points,” underscoring the durability of margin gains that have persisted through elevated catastrophe years.

Travelers enters 2026 with Q1 share repurchases of approximately $1.8 billion already guided, fixed income net investment income projected at $3.3 billion after tax for the full year, and an AI partnership with Anthropic empowering 10,000 technical employees, positioning the insurer to compound underwriting discipline with structural cost efficiency gains across its $43.9 billion premium base.

Wall Street’s Take on TRV Stock

The $5.5 billion in after-tax underlying underwriting income Travelers posted for 2025, up from $2.1 billion in 2022, signals a structural reset in the profitability of writing insurance, not a cyclical windfall, and that reset now anchors the forward earnings outlook.

As TIKR estimates, normalized EPS holds at $27.2 in 2026 before climbing to $28.3 in 2027, supported by an EBIT margin of 18.1% in 2026, a level that would have been unthinkable at the 10.2% trough recorded in 2023.

TRV’s EBIT margin recovery from 10.2% in 2023 to 18.8% in 2025 also represents a structural repricing of the book, driven by disciplined renewal premium change across all three segments, Business Insurance, Bond and Specialty, and Personal Insurance, and not by a single favorable loss year.

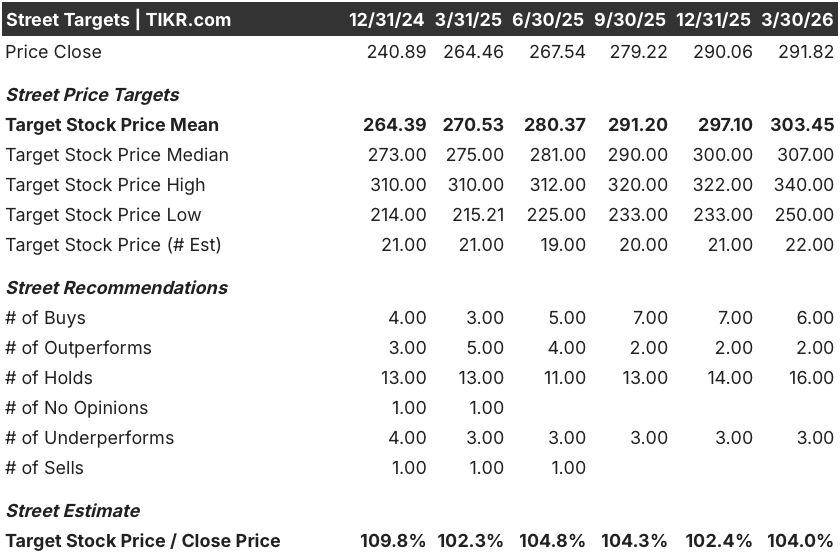

Fourteen analysts currently rate TRV as a Buy or Outperform, while 16 hold and 3 Underperform, with the mean price target of $303.5 implying roughly 4% upside from current levels, a consensus that reflects respect for execution but not yet conviction in the AI-driven efficiency cycle now embedded in the business.

The spread between the low analyst target of $250 and the high of $340 reflects a genuine fork: the bear case hinges on catastrophe losses overwhelming the 7.8% cat load built into the 2026 plan, while the bull case rests on AI-driven claim and underwriting efficiencies compressing the loss adjustment expense ratio faster than the Street models.

What Does the Valuation Model Say?

TIKR’s mid-case price target of $361.9 by December 2030, implying 24% total return and a 4.6% IRR, assumes a net income margin of 12.5% and a revenue CAGR of 3.0%, inputs directly supported by the $10.6 billion operating cash flow base and the Anthropic partnership accelerating software and underwriting delivery across the company.

The market prices TRV as a slow-growth insurer, yet the EBIT margin expanded 8.6 points in two years, a pace that the 1.9% revenue growth estimate for 2026 structurally obscures.

The claim organization’s straight-through processing rate, now covering more than half of all claims with customers adopting it two-thirds of the time, is compressing loss adjustment expense and showing up directly in the loss ratio, the core assumption behind TIKR’s $361.9 target.

Management’s guidance of $1.8 billion in Q1 2026 share repurchases alone, funded partly by the $700 million Canadian operations sale, signals a balance sheet with excess capital that the company is actively returning rather than hoarding.

A deterioration in casualty loss trends, specifically the long-tail commercial lines where management acknowledged ongoing uncertainty and retained an explicit IBNR provision for 2026, would directly pressure the 18.1% EBIT margin estimate and invalidate the mid-case model.

The April 16 Q1 2026 earnings call is the first test of whether the $800 million after-tax fixed income net investment income target and the 82.2% underlying combined ratio are tracking, and those two numbers together will confirm or challenge the TIKR mid-case thesis.

Should You Invest in The Travelers Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TRV stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track The Travelers Companies, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TRV stock on TIKR for Free →